Overview

Refinancing your FHA mortgage can save you money each month or give you cash for big expenses. Many homeowners use FHA refinance options to get better terms on their existing FHA loan. This guide walks you through how to apply for FHA refinance in simple steps.

Refinancing an FHA loan is popular because the Federal Housing Administration backs these loans, making them easier to qualify for than conventional ones.

What Is FHA Refinance?

An FHA refinance replaces your current home loan with a new one insured by the FHA. You can lower your interest rate, change your loan term, or take cash out from your home's equity.

The most common type is the FHA Streamline Refinance, which requires less paperwork if you already have an FHA mortgage.

Types of FHA Refinance Options

There are several ways to refinance your FHA loan:

- FHA Streamline Refinance: The easiest option for existing FHA loans. It often skips appraisal and income verification.

- FHA Cash-Out Refinance: Lets you borrow against your home equity for cash.

- FHA Simple Refinance: Similar to a standard refinance, with full underwriting.

- Rate-and-Term Refinance: Changes your rate or term without cash out.

The FHA Streamline is great for quick savings. I helped a friend go through this last year – they cut their payment by $200 a month with minimal hassle.

Eligibility Requirements for FHA Refinance

To qualify for most FHA refinance options:

- Your current loan must be an FHA-insured mortgage (for Streamline).

- You've made at least 6 on-time payments.

- At least 210 days have passed since your original closing.

- The refinance must provide a real benefit, like lower payments.

For cash-out:

- Minimum credit score of 580 (lender may require higher).

- Maximum 80% loan-to-value ratio.

- 12 months of on-time payments.

| Requirement | Streamline Refinance | Cash-Out Refinance |

|---|---|---|

| Existing FHA Loan | Yes | No (can be conventional) |

| Appraisal Needed | Often No | Yes |

| Credit Check | Limited or None | Full |

| Minimum Payments Made | 6 | 12 |

| Net Tangible Benefit | Yes (lower payment) | Yes |

Check official sources like HUD.gov for the latest rules, as they can change.

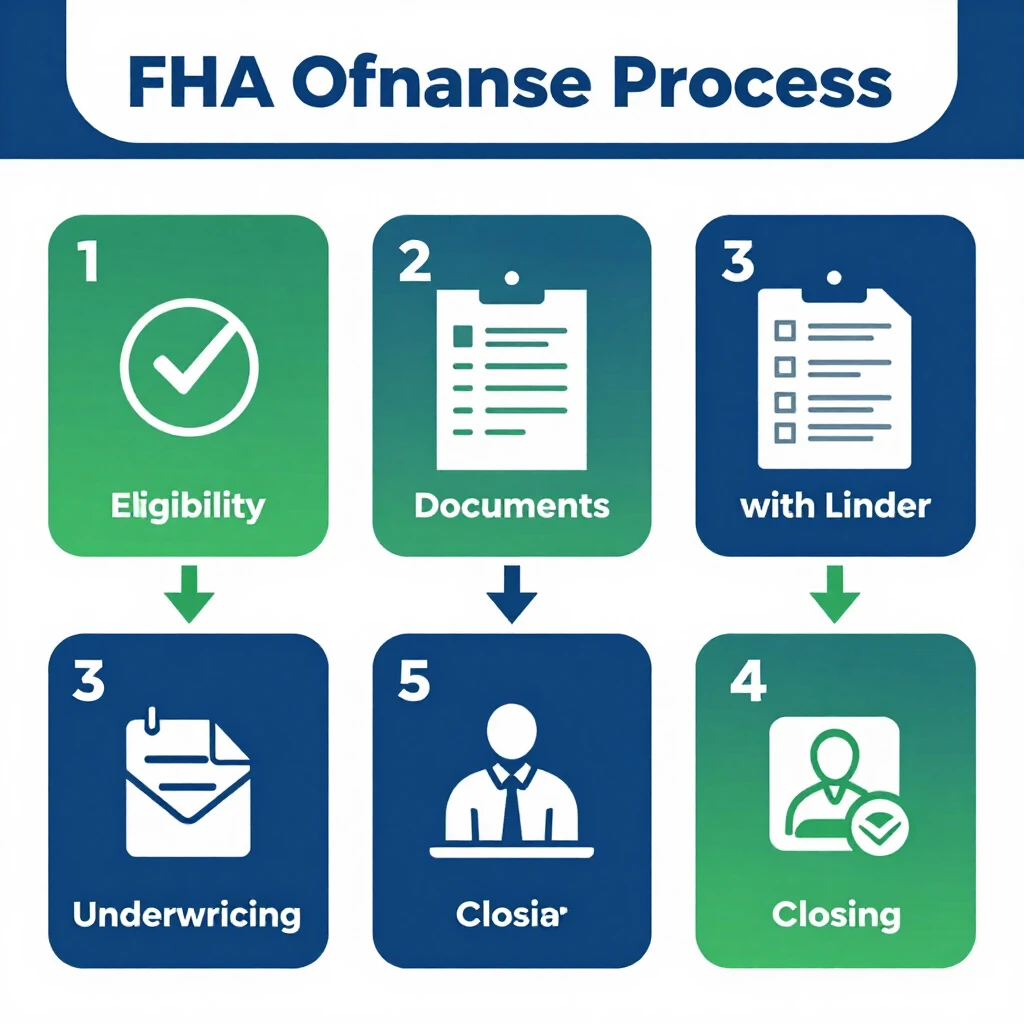

Step-by-Step: How to Apply for FHA Refinance

Follow these steps to apply:

-

Check Your Eligibility: Review your current FHA mortgage statements. Confirm you've met the seasoning requirements.

-

Shop for Lenders: Compare rates from FHA-approved lenders. Look for ones experienced in refinance.

-

Gather Documents: Even for Streamline, you'll need ID, mortgage statements, and possibly pay stubs.

-

Submit Application: Fill out the Uniform Residential Loan Application with your chosen lender.

-

Underwriting and Approval: The lender reviews your file. Streamline is faster – often 30 days or less.

-

Closing: Sign the new loan documents and pay any fees.

Pro tip: Start by getting quotes from three lenders. Rates can vary, and some offer no-closing-cost options by slightly raising the rate.

Costs Involved in FHA Refinance

Expect these fees:

- Upfront mortgage insurance premium (if applicable).

- Annual MIP on the new loan.

- Lender fees, appraisal (if needed), title search.

Many choose 'no-cost' refinances where fees are rolled into the rate.

In my experience, the savings from a lower rate often outweigh the costs within a couple of years.

Benefits and Drawbacks

Benefits: - Lower monthly payments. - Flexible credit requirements. - Possible no appraisal. - Access to cash for improvements.

Drawbacks: - Mortgage insurance premiums. - Closing costs. - Not all types allow cash out.

Common Mistakes to Avoid

Don't apply without checking if you'll save money. Use a refinance calculator to see your break-even point.

Also, keep making payments on your old loan until the new one closes.

Final Thoughts

Learning how to apply for FHA refinance can put more money in your pocket each month. If rates are lower than when you bought, or you need cash, it's worth exploring. Talk to a lender today to see your options.

For official info, visit HUD.gov or FHA.com.

(Word count: approximately 1520)