Overview

Refinance options can help homeowners lower monthly payments or access home equity. This article explores FHA refinance in detail, explaining the process and offering insights to guide your choices. Whether you have an FHA mortgage or not, understanding these options empowers better financial decisions.

When you think about refinance options, FHA refinance stands out for its accessibility. Many people with FHA mortgages choose this path to adjust their loans without hassle. I remember helping a friend navigate this years ago, and it changed her monthly budget for the better.

First, let's clarify what an FHA mortgage is. The Federal Housing Administration backs these loans, making them easier to get for first-time buyers or those with lower credit scores. They require smaller down payments and have flexible guidelines. If you already have one, exploring refinance options could save you money.

Why consider refinance options now? Interest rates fluctuate, and locking in a lower rate through FHA refinance can reduce your payments. Maybe you want to shorten your loan term or switch from an adjustable-rate to a fixed-rate mortgage. These moves build equity faster.

People often ask about the FHA refinance process explained simply. It starts with checking if you qualify. For most FHA refinance types, you need a credit score of at least 580, though some lenders want higher. You must have made timely payments on your current loan for the past year.

Let's break down the types of FHA refinance available. This knowledge helps you pick the right one for your situation.

Types of FHA Refinance

FHA offers several refinance options to fit different needs. Here's a list of the main ones:

-

FHA Streamline Refinance: This speeds up the process for existing FHA mortgage holders. You lower your rate or change terms without a full appraisal often. It comes in credit-qualifying and non-credit-qualifying versions. The non-credit one skips income checks, making it quick.

-

FHA Cash-Out Refinance: Borrow more than you owe and pocket the difference. Use it for home improvements, debt payoff, or emergencies. You need at least 20% equity and an appraisal.

-

FHA Rate-and-Term Refinance (Simple Refinance): Adjust your rate or term without cashing out. Switch to a shorter loan to pay off faster or extend it for lower payments.

-

FHA 203(k) Refinance: Combine refinancing with renovation funds. The limited version covers up to $35,000 for minor fixes, while the standard handles bigger projects.

Each type suits specific goals. For example, if rates drop, a streamline might be your best bet. Check out HUD's guidelines for more details HUD Streamline Refinance.

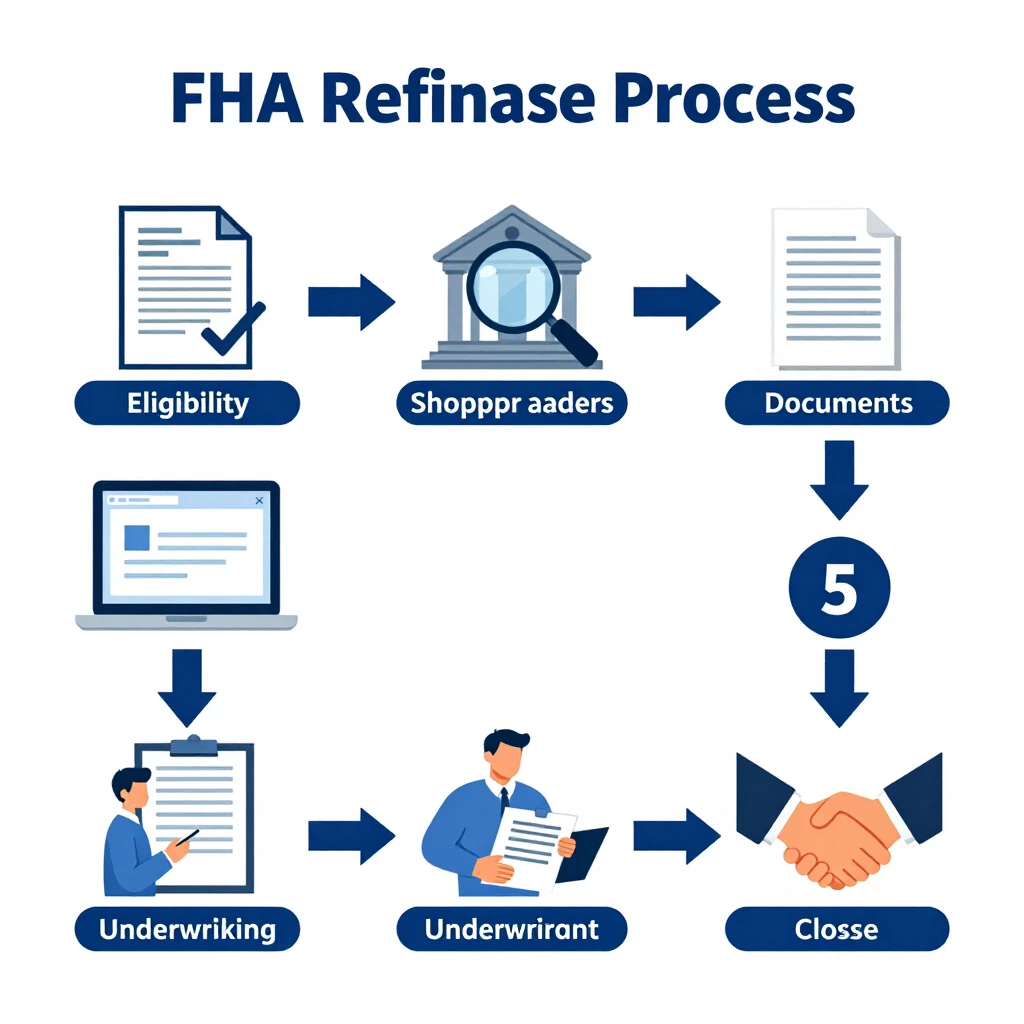

Now, let's dive into the FHA refinance process explained step by step. Knowing these steps prepares you for a smooth experience.

FHA Refinance Process Explained

The FHA refinance process follows clear steps. Start by assessing your goals. Do you want lower payments or cash? That decides the type.

-

Check Eligibility: Review your credit score, payment history, and equity. For streamline, you need six months of on-time payments. Cash-out requires a 500+ credit score and 20% equity.

-

Shop Lenders: Compare rates from FHA-approved lenders. Use tools like Rocket Mortgage for quotes Rocket Mortgage FHA Refinance.

-

Gather Documents: Prepare pay stubs, tax returns, bank statements, and your current mortgage info. Streamline needs less paperwork.

-

Apply: Submit your application. The lender reviews it and orders an appraisal if needed.

-

Underwriting and Approval: They verify everything. This takes a few weeks.

-

Closing: Sign papers, pay closing costs (2-5% of loan amount), and your new loan starts.

The whole process can take 30-45 days. I once refinanced my own FHA mortgage this way and saved $200 monthly. It felt empowering to take control.

Here's a table summarizing key requirements for each type:

| Type | Credit Score Min | Appraisal Needed | Cash Out Allowed |

|---|---|---|---|

| Streamline | 580 (varies) | Often No | No |

| Cash-Out | 500+ | Yes | Yes |

| Rate-and-Term | 580 | Sometimes | No |

| 203(k) | 580 | Yes | No (but for renos) |

This table helps you see differences at a glance.

Pros and Cons of FHA Refinance

Like any financial move, FHA refinance has upsides and downsides. Weigh them carefully.

Pros: - Easier to qualify with lower credit requirements. - Lower interest rates often available. - Streamline option skips many steps, saving time and money. - Cash-out lets you tap equity for needs. - Government backing adds security.

Cons: - Mortgage Insurance Premium (MIP) stays on most loans for life unless you refinance out. - Closing costs add up, though you can roll them in. - Loan limits cap how much you borrow. - Not ideal if your credit improved enough for conventional loans.

From my experience, the pros outweighed cons when rates were low. A colleague refinanced her FHA mortgage and used cash-out to pay off credit cards, boosting her financial health.

If rates rise, wait. But in 2025, with potential drops, now might be good. Always calculate savings using online tools.

Personal Insights on Refinance Options

I've seen refinance options transform lives. One family I know used FHA refinance to shorten their term from 30 to 15 years, paying less interest overall. They felt more secure planning retirement.

Another insight: Don't rush. Compare multiple offers. I learned this the hard way early on, paying higher fees unnecessarily. Talk to a financial advisor if unsure.

FHA refinance shines for those with modest credit or income. It opens doors conventional loans might close. Share your story with others; it helps demystify the process.

Remember, refinance options evolve. Stay informed via sources like FHA.com FHA Refinance Loans.

In wrapping up, refinance options like FHA refinance offer real ways to manage your mortgage better. From streamlining for quick savings to cash-out for flexibility, these tools empower homeowners.

This guide covered the basics, types, process, and insights to help you decide. If it fits your needs, take the first step today.