Overview

Your credit score plays a big role in getting a mortgage. It affects whether you qualify, the interest rate you get, and how much you pay over time. A higher score opens doors to better deals and saves you money.

Many people dream of owning a home, but they worry about their credit. I remember when I bought my first house. My score was around 680, and I got a decent rate, but I wished it was higher. Looking back, small changes could have saved me thousands.

How Your Credit Score Affects Your Mortgage starts with the basics. Lenders use your score to decide if you are a low-risk borrower. According to the Consumer Financial Protection Bureau (CFPB), higher scores mean lower interest rates because they show a strong history of paying bills on time.

What Is a Credit Score and Why Does It Matter?

A credit score is a number from 300 to 850 that sums up your credit history. Most lenders look at FICO scores for mortgages. They pull reports from the three big agencies: Equifax, Experian, and TransUnion. They often use the middle score.

Your score matters because it predicts how likely you are to repay the loan. The CFPB explains that consumers with higher credit scores get lower interest rates.

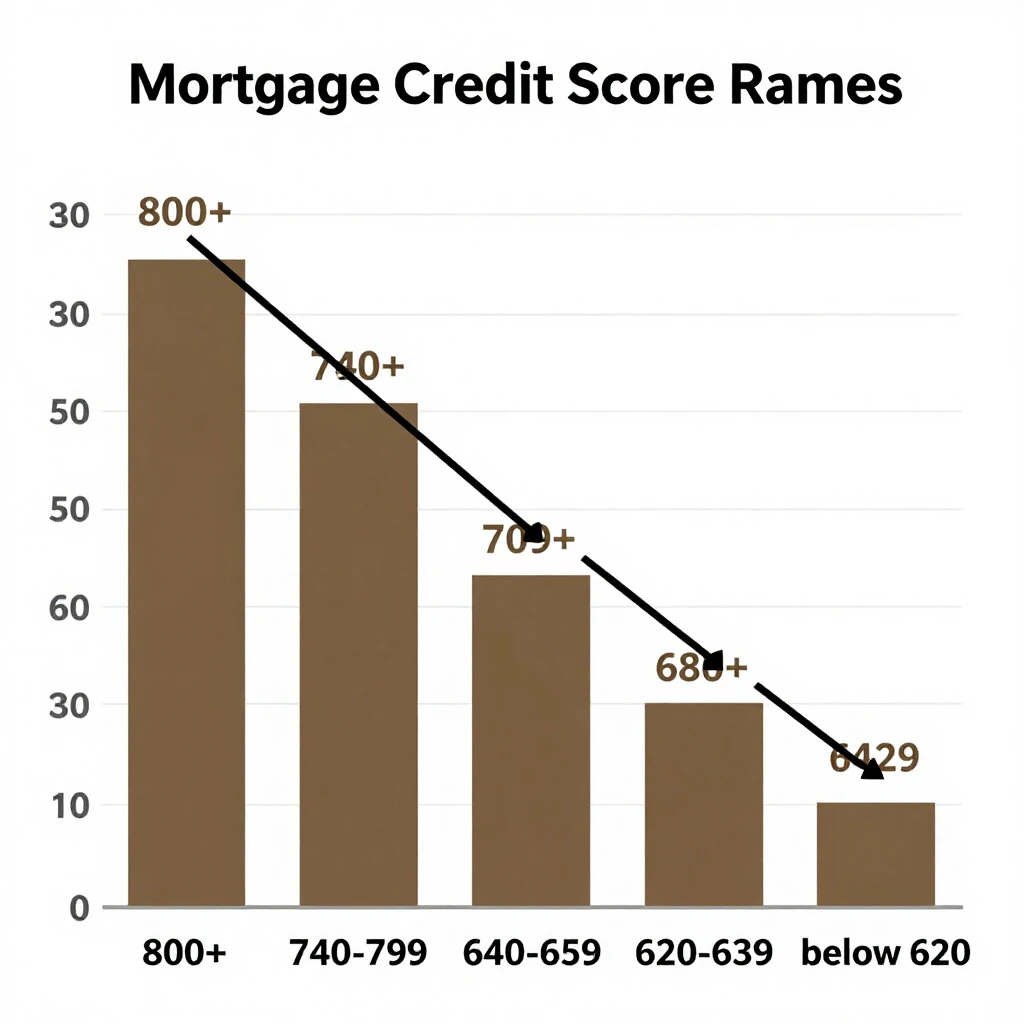

How Scores Impact Interest Rates

Interest rates change a lot based on your score. Even a small difference can add up over 30 years.

Here are average rates from recent data (as of early 2026):

| Credit Score Range | Average 30-Year Fixed APR |

|---|---|

| 760+ | 6.4% - 6.5% |

| 700-759 | 6.7% - 6.8% |

| 680-699 | 6.9% |

| 620-639 | 7.2% - 7.3% |

A higher score can drop your rate by half a percent or more. On a $300,000 loan, that saves hundreds per month.

Approval and Down Payment Requirements

Beyond rates, your score affects approval. For conventional loans backed by Fannie Mae or Freddie Mac, lenders look at your full profile, but scores below 620 make it harder.

FHA mortgages offer more flexibility. You can qualify with a score as low as 580 for 3.5% down, or 500-579 for 10% down. This helps many first-time buyers.

If your score is low, consider FHA approved lenders. They specialize in these loans and guide you through the process.

Top Mortgage Tips for Homeowners

Here are practical steps to manage your credit:

- Pay bills on time every month. This counts for 35% of your score.

- Keep credit card balances low. Aim under 30% of your limit.

- Avoid new credit applications before buying a home.

- Check your credit reports for errors at AnnualCreditReport.com.

- Build credit slowly if needed.

These top mortgage tips for homeowners work. One friend boosted his score 50 points in six months by paying down debt.

Options for Lower Scores: FHA Mortgages

An FHA mortgage is great if your score isn't perfect. Backed by the government, these loans have easier rules. Find top FHA lenders for refinancing or buying. They often approve scores down to 580.

Refinancing with an FHA loan can lower your rate later when your score improves.

Long-Term Savings Example

Let's say you borrow $400,000 for 30 years.

- At 6.5% (excellent score): Monthly payment about $2,528. Total interest: ~$510,000.

- At 7.5% (lower score): Monthly payment about $2,795. Total interest: ~$606,000.

Difference: Over $95,000 saved with a better score!

Improving your score pays off big.

Personal Insights and Final Thoughts

From experience, don't rush into a mortgage with a low score. Take time to improve it. Shop multiple lenders too.

Your credit score shapes your mortgage journey, but you control it. Start today for better options tomorrow.

Summary

A strong credit score unlocks lower rates, easier approval, and big savings on your mortgage. Focus on good habits, consider FHA options if needed, and watch your homeownership dreams become reality.