Overview

Boosting your credit score can unlock lower interest rates and better terms on your home loan. With simple, consistent actions, you can see improvements in months and make homeownership more affordable.

Your credit score plays a huge role in getting approved for a mortgage and determining your interest rate. A higher score means lenders see you as less risky, so they offer better deals. I've seen friends save thousands over the life of their loan just by raising their score a few points before applying.

The average credit score for mortgage borrowers is around 737 these days. If yours is lower, don't worry—many people start there and improve it successfully.

Why Your Credit Score Matters for a Mortgage

Lenders use your score to decide if they'll lend you money and at what rate. Scores range from 300 to 850. Generally:

- 740+: Excellent rates

- 700-739: Good options

- 670-699: Fair

- Below 670: Higher rates or tougher approval

Even a 20-point boost can drop your rate enough to save big over 30 years.

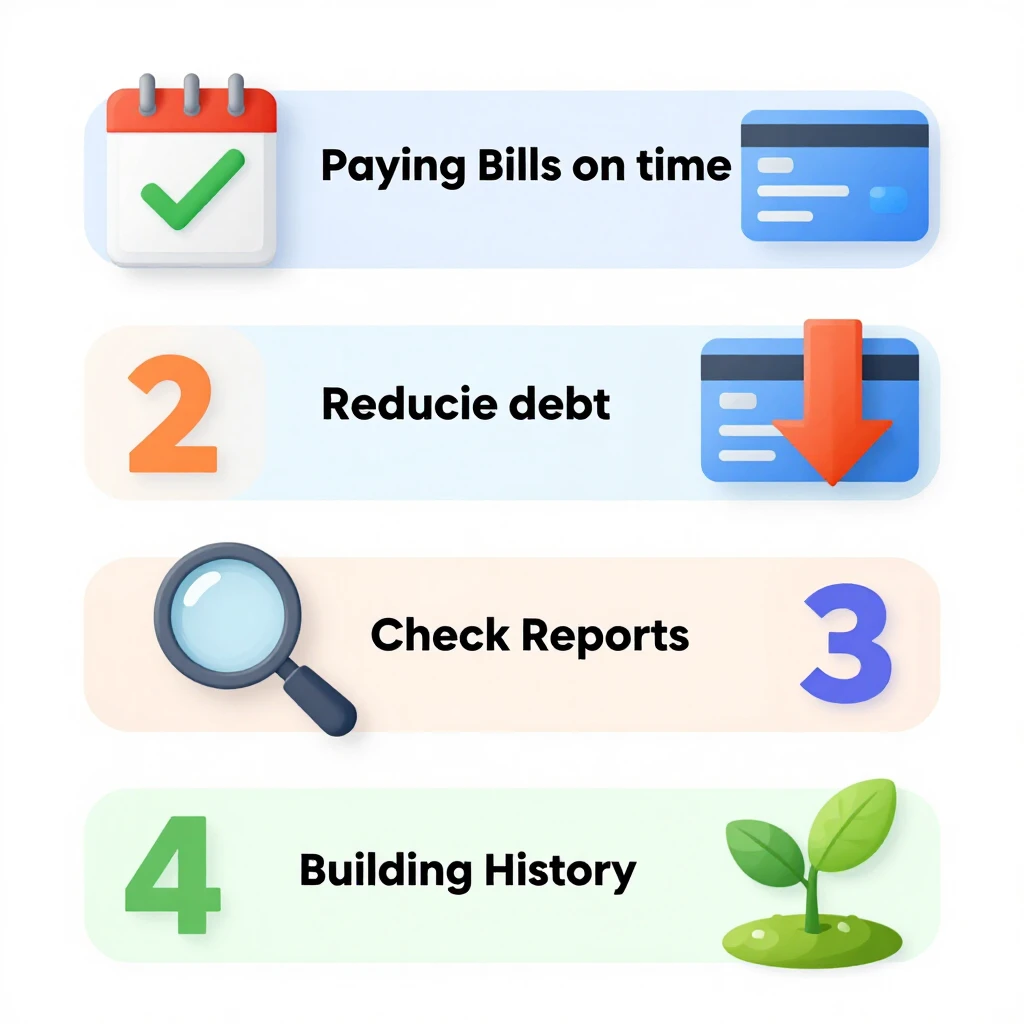

Step 1: Check Your Credit Reports

Start by getting your free credit reports from AnnualCreditReport.com. Review them from all three bureaus: Equifax, Experian, and TransUnion.

Look for errors like wrong accounts or late payments that aren't yours. Dispute mistakes online—fixes can happen fast and boost your score quickly.

Step 2: Pay Bills on Time

Payment history is 35% of your score—the biggest factor. Set up autopay for everything: credit cards, loans, utilities.

If you've missed payments, get current now. One late payment can hurt, but consistent on-time ones rebuild trust.

Step 3: Lower Your Credit Utilization

This is how much of your available credit you're using—aim for under 30%. For example, if your card limit is $10,000, keep the balance below $3,000.

Pay down high balances first. This can raise your score fast, often in a month or two.

Step 4: Avoid New Credit Applications

Each hard inquiry can ding your score a few points. Don't open new cards or loans right before applying for a mortgage.

But shopping for mortgages is okay—multiple inquiries in a 45-day window count as one.

Step 5: Build Positive History

Become an authorized user on a family member's good-standing card. Or use tools like Experian Boost to add on-time rent or utility payments to your report.

If your score is low, consider a secured credit card—use it lightly and pay in full.

Quick Wins Table

| Action | Potential Impact | Time Frame |

|---|---|---|

| Fix report errors | 20-100 points | 30-60 days |

| Pay down utilization | 20-50 points | 1-2 months |

| On-time payments | Steady increase | Ongoing |

| Add positive accounts | 10-30 points | 1-3 months |

Considering an FHA Mortgage?

If your score is between 580 and 739, an FHA mortgage could be a great option. These government-backed loans allow just 3.5% down and are more forgiving on credit.

FHA loans require mortgage insurance, but recent reductions make it more affordable. For most borrowers, the annual FHA mortgage insurance is around 0.55% of the loan amount.

FHA Mortgage Insurance Application Tips

When applying for an FHA mortgage:

- Shop lenders—some specialize in FHA and offer better service.

- Prepare documents early: pay stubs, tax returns, bank statements.

- Understand FHA mortgage insurance: There's an upfront premium (often rolled into the loan) and annual one added monthly.

- If your score is low, work on boosting it first for better terms.

I remember helping a relative boost their score from 620 to 680 in six months. They paid down cards, fixed an error, and got approved for an FHA mortgage with a decent rate. Small steps add up.

Be patient but consistent. Track your score monthly with free tools.

Final Thoughts

Improving your credit takes effort, but it's worth it for your dream home. Start today: pull reports, pay on time, reduce debt. You'll be in a stronger position for that mortgage approval.

For authoritative info, check sites like FHA.gov or Experian.com.