Quick Overview

Mortgage insurance premiums (MIP) are a key part of FHA loans. They protect lenders if you can't pay back your loan, letting you buy a home with a small down payment. This guide explains everything you need to know about understanding mortgage insurance premiums in simple terms. (38 words)

What Are Mortgage Insurance Premiums?

When you get an FHA mortgage, you pay mortgage insurance premiums. These are not the same as homeowners insurance, which covers damage to your house.

MIP protects the lender, not you. If you stop making payments, the Federal Housing Administration (FHA) steps in to cover the lender's loss. This is why lenders offer FHA loans with down payments as low as 3.5%.

Many first-time buyers choose FHA loans because of this flexibility. I've seen friends buy their first home sooner thanks to these options.

Types of FHA Mortgage Insurance Premiums

There are two main types:

-

Upfront Mortgage Insurance Premium (UFMIP): Paid at closing, usually 1.75% of the loan amount. You can pay it in cash or add it to your loan.

-

Annual Mortgage Insurance Premium (Annual MIP): Paid monthly, divided over 12 payments. Rates range from 0.45% to 0.55% for most borrowers in recent years.

According to the U.S. Department of Housing and Urban Development (HUD), these premiums fund the FHA insurance program that helps millions become homeowners HUD.gov - Single Family Mortgage Insurance Premiums.

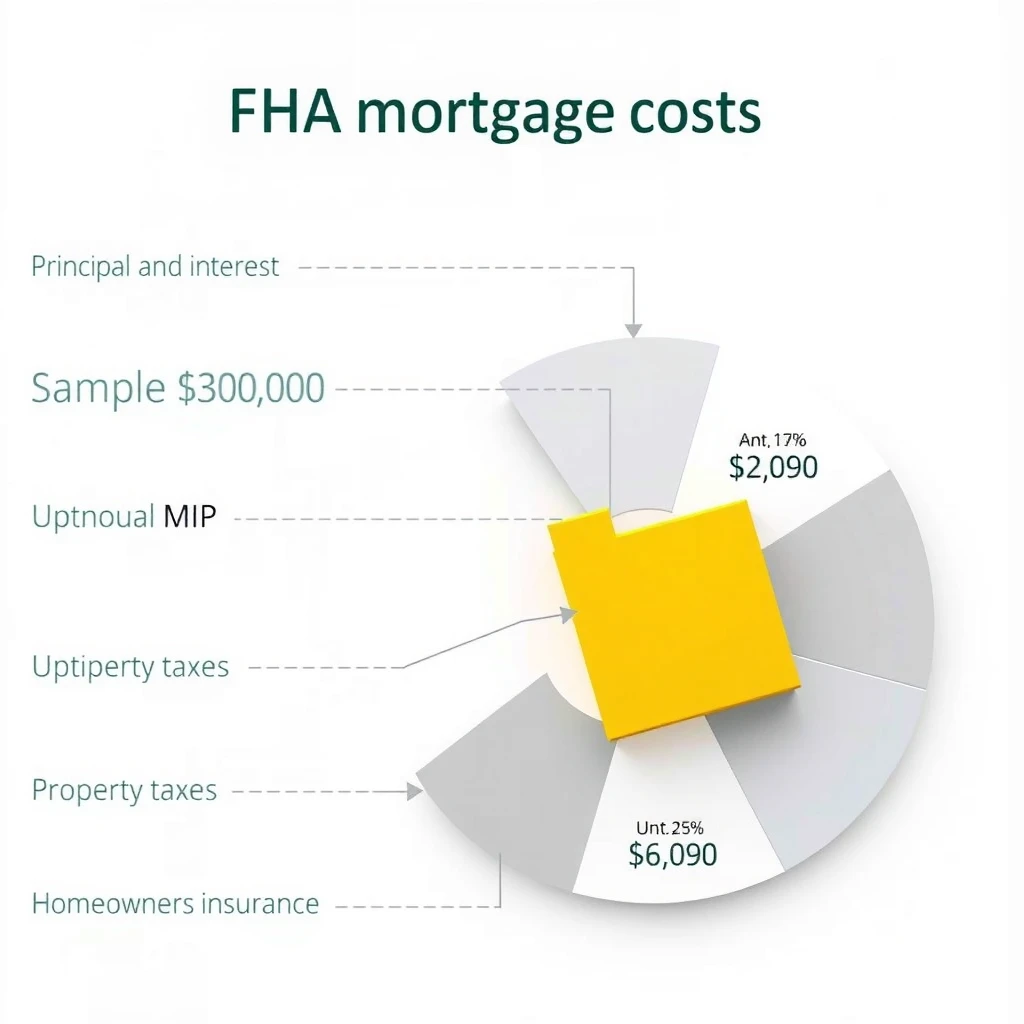

How Much Do You Pay for MIP?

Costs depend on your loan size, down payment, and term.

Here’s a simple table for typical 30-year FHA loans:

| Down Payment | Loan Amount ≤ $726,200 | Annual MIP Rate |

|---|---|---|

| Less than 10% | Most cases | 0.55% |

| 10% or more | Shorter duration | Lower or removable |

Upfront is always 1.75%. For details on current rates, check the official HUD handbook appendix HUD Appendix 1.0 – Mortgage Insurance Premiums.

In my experience, adding the upfront to the loan keeps closing costs low, but it increases your monthly payment slightly.

FHA Loan Eligibility: Do You Qualify?

FHA loan eligibility is more forgiving than conventional loans.

Key requirements:

- Credit score: At least 580 for 3.5% down (or 500-579 for 10% down).

- Steady income and employment history.

- Debt-to-income ratio usually under 43%.

- The home must be your primary residence.

HUD outlines these standards to make homeownership accessible HUD.gov - Loans.

One couple I know had a credit dip from student loans but still qualified because FHA looks at your full picture.

Steps to Apply for an FHA Loan

Ready to move forward? Here are the steps to apply for an FHA loan:

- Check your credit and fix any errors.

- Find an FHA-approved lender (search on HUD's site).

- Get pre-approved to know your budget.

- Shop for homes within FHA limits.

- Make an offer and submit your full application.

- Complete the appraisal and underwriting.

- Close and pay the upfront MIP.

The process takes 30-45 days usually. Start with pre-approval—it strengthens your offers.

Can You Remove MIP from Your FHA Loan?

Yes, sometimes!

- If you put down 10% or more, annual MIP drops off after 11 years.

- With less than 10% down, it's for the life of the loan (for newer loans).

- Refinance to a conventional loan when you have 20% equity to drop it entirely.

Many borrowers refinance later as home values rise. Plan for this from the start.

Pros and Cons of FHA Mortgage Insurance

Pros: - Low down payment. - Easier qualification. - Helps build equity faster in rising markets.

Cons: - Adds to monthly payment. - May last the full loan term.

Weigh these against your goals. For many, the benefits outweigh the costs.

Tips to Manage Mortgage Insurance Premiums

- Shop multiple lenders for the best rates.

- Improve your credit before applying.

- Consider a larger down payment if possible.

- Budget for MIP in your monthly payments.

- Track home value for future refinance.

Understanding mortgage insurance premiums helps you make smart choices. Talk to a lender early—they can run numbers for your situation.

Final Thoughts

Understanding mortgage insurance premiums is key to succeeding with an FHA mortgage. These premiums make homeownership possible for many who couldn't qualify otherwise. With planning, the extra cost pays off in owning your home.

If you're ready, start checking your eligibility today. Homeownership is within reach!