Buying a home can feel like a big step, especially if it’s your first time. An FHA mortgage might be the key to making it happen. This guide breaks down Understanding FHA mortgage requirements in a simple, clear way so you can move forward with confidence.

What Are FHA Mortgages?

An FHA mortgage is a loan backed by the Federal Housing Administration. If you can’t pay it back, the FHA steps in to protect the lender. This setup makes lenders more open to helping people who might not qualify for regular loans. It’s a popular choice for first-time buyers because the rules are easier to meet.

Why Pick an FHA Loan?

Here’s why an FHA loan might work for you:

- Smaller Down Payment: You only need 3.5% down, not the 20% some other loans ask for.

- Easier Credit Rules: You can qualify with a lower credit score—sometimes as low as 500.

- Help for New Buyers: There are perks like lower rates and resources to guide you through.

Key FHA Mortgage Guidelines

To get an FHA loan, you need to meet some basic rules. Let’s walk through them.

Credit Score

Your credit score matters, but it doesn’t have to be perfect: - 580 or Higher: You can put down just 3.5%. - 500-579: You’ll need 10% down.

A better score means better rates, so it’s worth checking yours early.

Down Payment

The down payment is a big deal for most buyers: - With a 580+ credit score, it’s 3.5% of the home price. - Below that, it jumps to 10%.

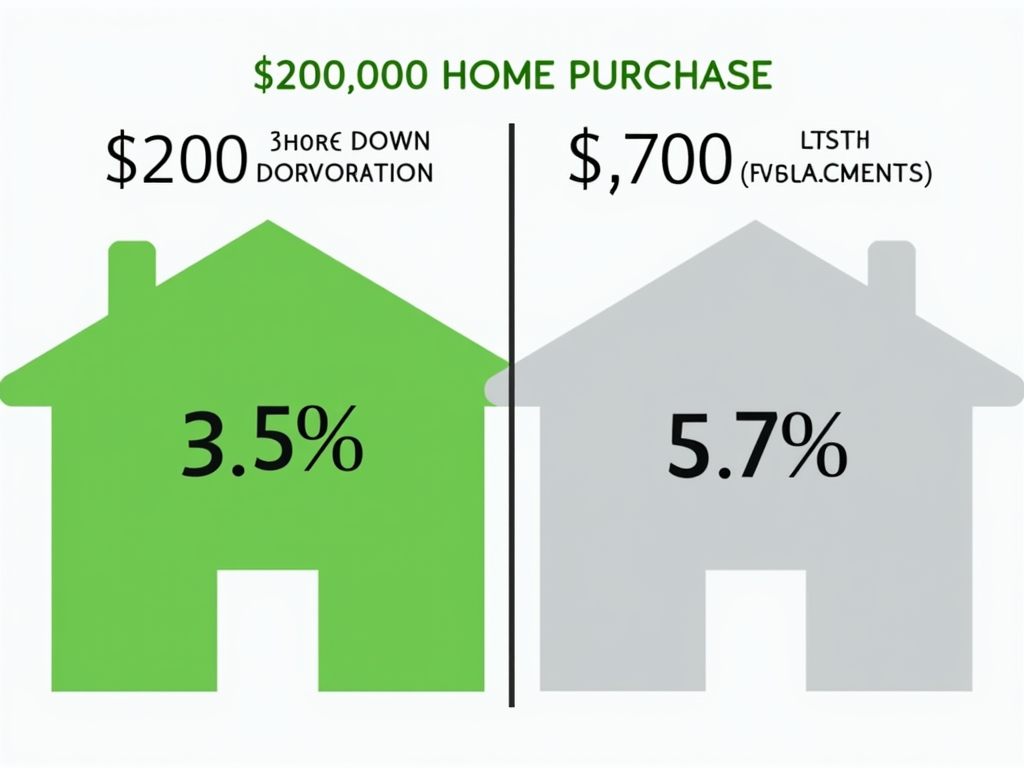

For a $200,000 house, that’s $7,000 versus $20,000—huge difference!

Debt-to-Income Ratio

This is how much of your income goes to bills: - Housing Costs: Shouldn’t be more than 31% of your income. - All Debt: Should stay under 43%, though some lenders stretch to 50% if you’re strong elsewhere.

If you make $4,000 a month, your mortgage payment should be $1,240 or less.

Work History

Lenders want to see you’ve got steady work: - Two Years: They’ll look at the last two years of your job history. - Proof: Bring pay stubs or tax returns to show your income.

If you switched jobs, just explain it—they’re flexible.

Property Rules

The house has to fit certain standards: - Live There: You must use it as your main home. - Check It: An FHA appraiser has to approve it.

This keeps the loan safe for everyone involved.

Insurance Costs

FHA loans come with extra fees: - Upfront Fee: 1.75% of the loan, paid once (can be added to the loan). - Monthly Fee: A small amount each month, based on your loan size.

These protect the lender if something goes wrong.

How to Qualify for an FHA Mortgage

Ready to get started? Follow these steps:

- Know Your Credit: Check your score online or with a lender.

- Figure Out Debt: Add up your bills and income to see your ratio.

- Save Up: Aim for that 3.5% down payment plus some extra for fees.

- Get Pre-Approved: Talk to a lender early to lock in your budget.

- Pick a Lender: Find one who knows FHA loans inside out.

- Apply: Send in your paperwork and wait for the green light.

- Appraisal Time: The house gets checked by an expert.

- Close the Deal: Sign the papers and get your keys!

Myths About FHA Loans

Let’s bust some wrong ideas:

- Not Just for First-Timers: Anyone can apply if they qualify.

- Not Slow: Closing takes about a month, like most loans.

- Bankruptcy’s Okay: You might just need to wait a bit after one.

My FHA Story

When I bought my first place, I was nervous. My credit was okay—around 600—but my savings were thin. The FHA loan let me put down 3.5%, which was a lifesaver. My lender walked me through everything, and the appraisal took a week longer than I hoped, but it was worth it. Now, I’m in my home, and it feels real.

Wrapping Up

Understanding FHA mortgage requirements opens the door to homeownership for so many. With a low down payment, easier credit rules, and clear steps, an FHA mortgage can be your path forward. Do your homework, talk to a lender, and take it one step at a time. You’ve got this!