Buying a home is a big step, but a good credit score can make it easier. This guide shows you how to boost your credit score before buying a home, shares expert tips for first-time home buyers, and explains steps to apply for an FHA loan. Get ready to own your dream home!

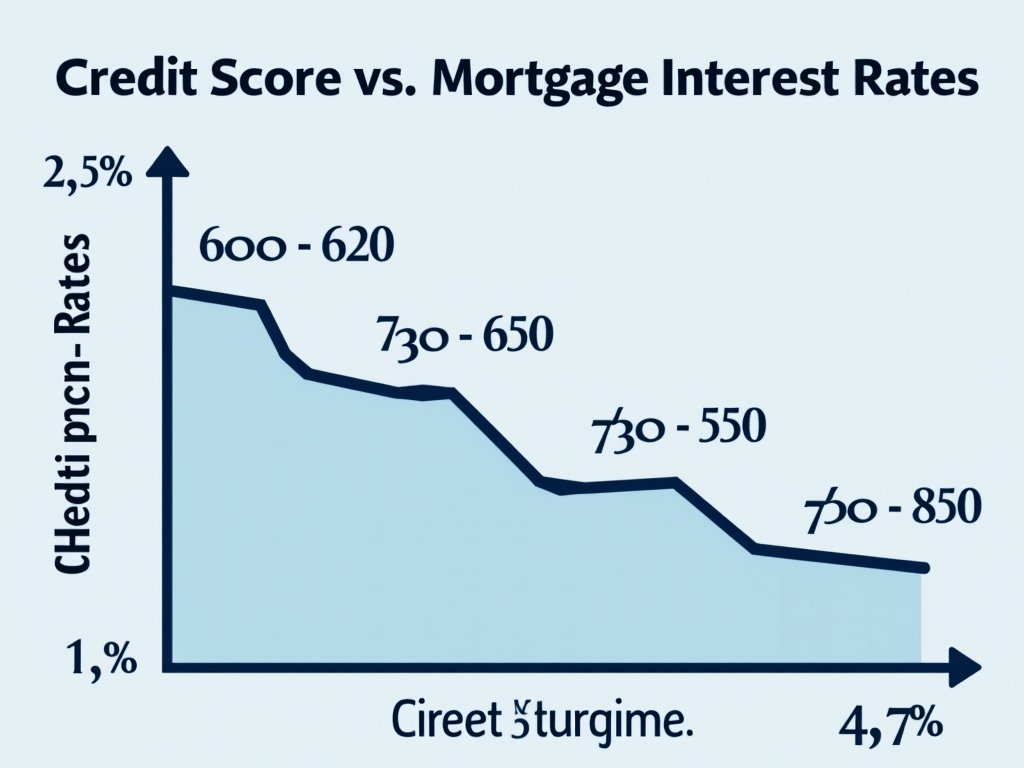

Your credit score matters a lot when you want to buy a home. It’s a number that tells lenders if you’re good at paying back money. A higher score means better mortgage rates and terms. For example, a score above 760 might get you a 3.5% interest rate, while a 620 could mean 5%. That gap can cost you thousands over 30 years.

So, how do you raise your score? It’s not magic, but it takes effort. Here are five steps I’ve seen work for real people:

-

Pay Bills on Time - Late payments hurt your score big time. Use reminders or auto-pay. I once helped a friend set this up, and her score jumped 20 points in months!

-

Lower Credit Card Balances - Keep your card balances under 30% of the limit. Paying off $500 on a $2,000 limit card can lift your score fast.

-

Skip New Credit Applications - Every new application dings your score a little. Hold off until after your mortgage is approved.

-

Fix Credit Report Mistakes - Errors happen. I found a wrong late payment on my report once and got it removed—it boosted my score by 15 points.

-

Keep Old Accounts Open - Older accounts show you’ve managed credit well. Don’t close that first card you got in college!

Now, let’s talk about FHA loans, a great option for first-time buyers. An FHA mortgage is backed by the government, so lenders are more flexible. You can get in with a lower score and a smaller down payment. I’ve seen friends with scores around 580 buy homes they thought were out of reach because of this.

Why Choose an FHA Loan? - Down payments as low as 3.5%. - Accepts scores as low as 580 (or 500 with 10% down). - Rates stay competitive. - Closing costs can roll into the loan.

FHA Loan Eligibility includes: - Credit score of 580+ for 3.5% down. - Debt-to-income ratio under 43%. - Steady job for at least two years. - The home must be your main place to live.

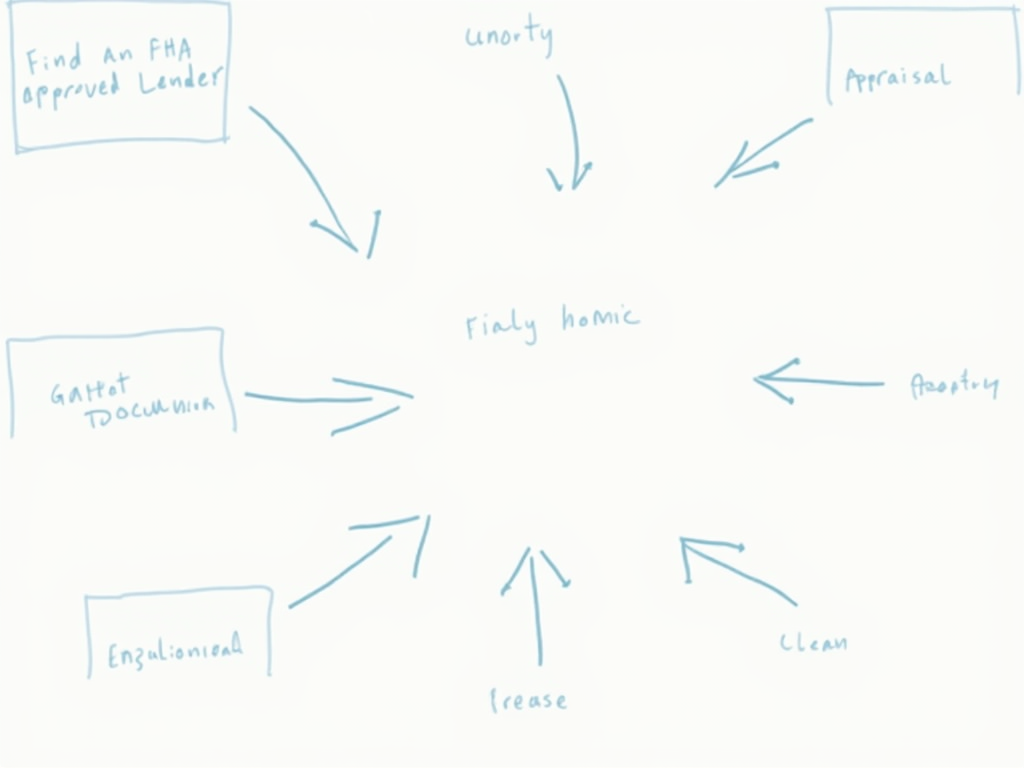

Ready to apply? Here are the steps to apply for an FHA loan:

-

Find an FHA-Approved Lender - Check online for local options. Not every bank does these.

-

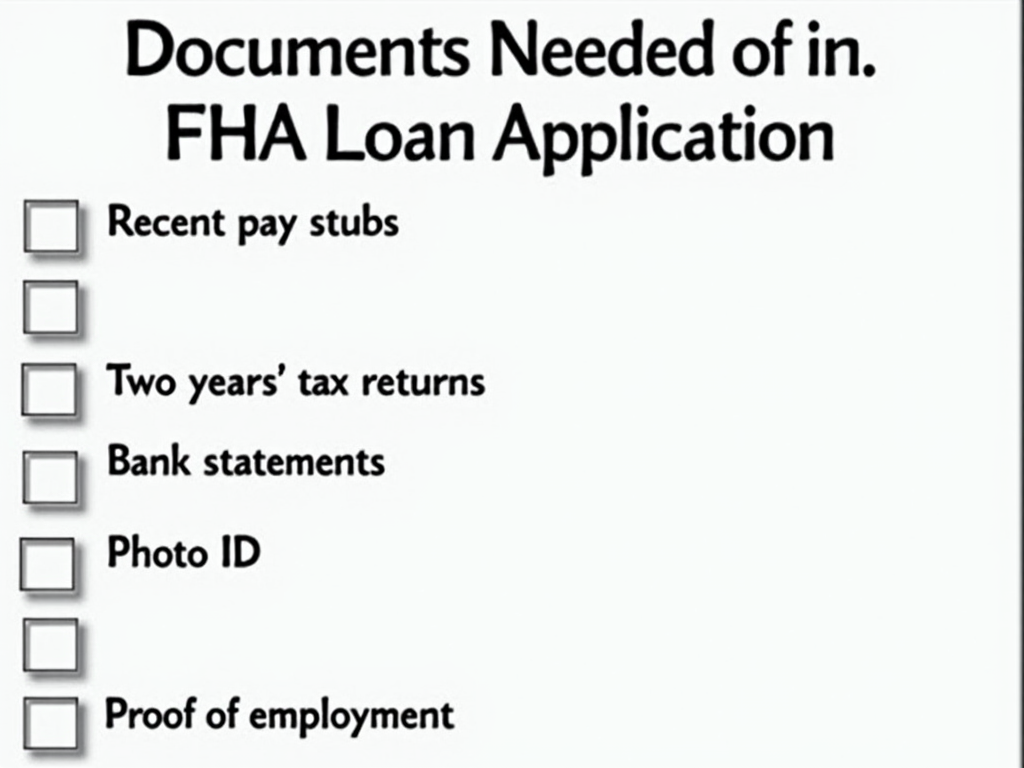

Gather Your Papers - You’ll need pay stubs, tax returns, and ID. I keep mine in a folder to stay organized.

-

Submit the Application - Your lender walks you through this. Answer their questions honestly.

-

Get the Property Checked - An appraiser makes sure the home’s value matches the loan.

-

Close the Deal - Sign papers, pay fees, and get your keys!

First-time buyers, listen up! Here are some expert tips for first-time home buyers I’ve picked up:

-

Save More Up Front - A bigger down payment cuts your monthly bill. I saved an extra $2,000 and avoided some insurance costs.

-

Get Pre-Approved - This tells sellers you’re serious. It also sets your budget. My pre-approval helped me focus on homes I could actually buy.

-

Team Up with an Agent - A good agent knows the market and fights for you. Mine found me a deal $10,000 below asking!

Boosting your credit score opens the door to homeownership. Follow these steps to improve your score, explore FHA loan eligibility, and use these tips to buy your first home. It’s a journey, but with effort, you’ll be holding those keys sooner than you think!