Choosing the right mortgage is a big step toward owning your dream home. With so many options out there, it’s easy to feel lost. This guide simplifies the process, helping you pick a mortgage that fits your life and budget. Let’s walk through it together, step by step.

Understanding Your Mortgage Options

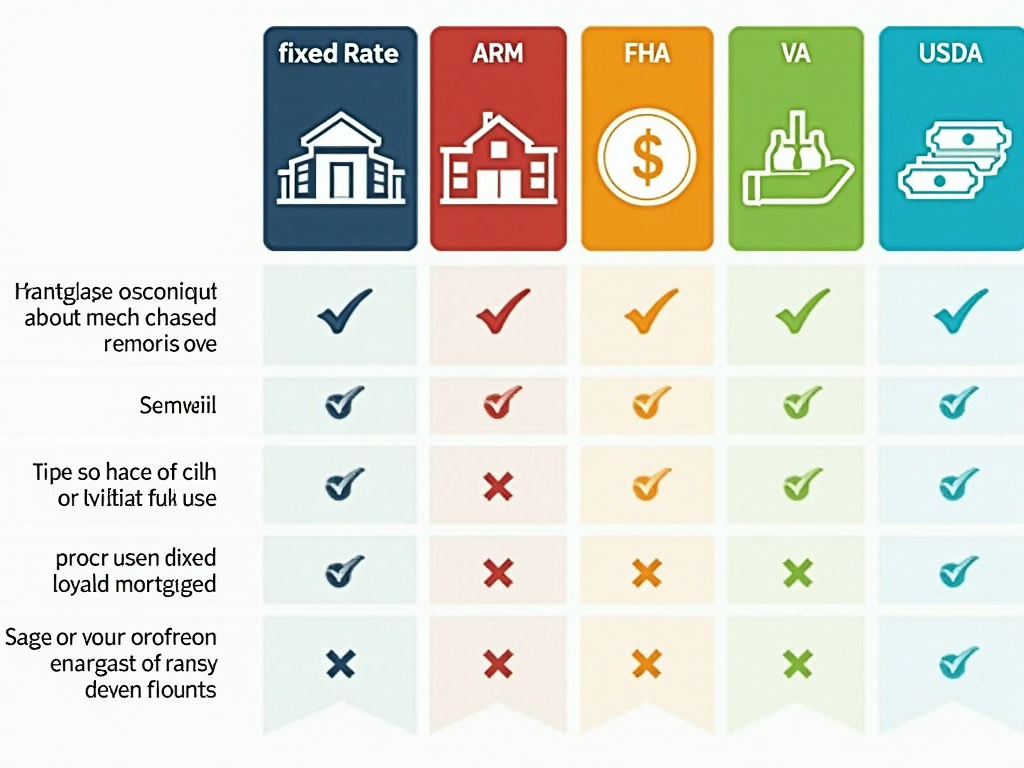

Not all mortgages are the same. Each type has its own perks and challenges. Knowing what’s out there helps you find the one that’s right for you. Here’s a breakdown of the main options:

- Fixed-Rate Mortgages: Your interest rate stays the same for the whole loan term. This means your monthly payment won’t change, giving you peace of mind.

- Adjustable-Rate Mortgages (ARMs): The interest rate can shift over time. It might start low, but it could rise later, so it’s a bit of a gamble.

- FHA Loans: These are great if your credit isn’t perfect or you don’t have much for a down payment. The government backs them, which can make approval easier.

- VA Loans: If you’re a veteran or in the military, these offer awesome benefits like no down payment.

- USDA Loans: Perfect for buying in rural areas, with low rates and no down payment needed.

Figuring Out Your Finances

Before you pick a mortgage, take a good look at your money situation. This isn’t just about what you can afford today—it’s about what works tomorrow too. Here’s what to think about:

- Credit Score: A higher score gets you better rates. Check yours before you start.

- Down Payment: How much can you pay upfront? More cash now means less to borrow.

- Debt-to-Income Ratio: Lenders care about how much you owe compared to what you earn. Keep this low if you can.

- Future Plans: How long will you stay in this home? A short stay might mean a different mortgage makes sense.

Your Step-by-Step Home Buying Guide: The Mortgage Process

Ready to apply? The mortgage process can feel like a maze, but it’s manageable if you break it down. Here’s how it goes:

- Gather Your Papers: You’ll need pay stubs, tax returns, and bank statements.

- Get Pre-Approved: This shows how much you can borrow and proves you’re serious to sellers.

- Shop Around: Don’t grab the first offer. Compare lenders for the best rates.

- Apply: Fill out the forms and send in your documents.

- Wait for Underwriting: The lender checks everything to make sure you qualify.

- Close the Deal: Sign the papers, and the house is yours!

I remember gathering my own papers late at night, triple-checking everything. It’s stressful, but so worth it when you get those keys.

FHA Loan Application Process: A Closer Look

If an FHA mortgage sounds right for you, here’s what to expect. The FHA loan application process is a bit unique because it’s designed to help people who might not qualify otherwise. You’ll still need your income proof and credit history, but the rules are more flexible. Lenders often move faster with these, too, since the government backs them. My cousin used an FHA loan for her first home—she loved how it didn’t demand a huge down payment.

Real Tips from Real Experience

Choosing the right mortgage isn’t just numbers—it’s personal. Here’s what I’ve learned from my own journey and talking to others:

- Stick to Your Budget: Don’t stretch yourself thin. Leave room for life’s surprises.

- Look Ahead: A low rate now might not stay low. Think about the next 10 years.

- Take Your Time: I rushed my first offer and regretted it. Shop around instead.

- Ask for Help: A good advisor can spot things you’d miss.

- Read Everything: Those tiny terms matter. I once skipped a fee detail and paid for it later.

How Different Mortgages Compare

Here’s a quick table to see your options side by side:

| Mortgage Type | Down Payment | Interest Rate | Best For |

|---|---|---|---|

| Fixed-Rate | 3-20% | Stable | Long-term stability |

| ARM | 5-20% | Changes | Short-term savings |

| FHA | 3.5% | Fixed or Adjustable | First-time buyers |

| VA | 0% | Fixed or Adjustable | Veterans |

| USDA | 0% | Fixed | Rural buyers |

This table helped me narrow down my choice—seeing it laid out made the decision clearer.

Why This Matters to You

Picking a mortgage isn’t just about the house—it’s about your life. A friend of mine locked into a fixed-rate mortgage and slept easy knowing her payments wouldn’t jump. Another went with an ARM, betting rates would drop. Both made it work because they knew their goals. That’s the trick: match the mortgage to your story.

Take it slow. Dig into your options. Talk to someone who’s been there. You’re not just buying a home—you’re building a future.

Wrapping It Up

How to choose the right mortgage for you comes down to three things: knowing your options, checking your finances, and planning ahead. This guide has walked you through the types, the process, and some honest tips to get it right. Whether it’s an FHA loan application or a VA deal, you’ve got the tools now. Take your time, and soon you’ll be unlocking your own front door.