Navigating the world of mortgages can feel like a big challenge. This guide explains different mortgage types and options, focusing on FHA loans, to help you choose wisely.

Buying a home is exciting, but it’s also a huge financial step. Picking the right mortgage can make all the difference. With so many choices out there, it’s easy to feel lost. That’s why understanding mortgage types and options is key. In this guide, we’ll walk through fixed-rate mortgages, adjustable-rate mortgages (ARMs), conventional loans, FHA loans, VA loans, and USDA loans. We’ll dig deep into FHA loans, covering how to apply for an FHA mortgage and what FHA loan requirements you need to meet.

So, what’s a mortgage anyway? It’s a loan you use to buy a home. The home itself acts as security for the loan. You pay it back over time—usually 15 or 30 years—through monthly payments. The mortgage type you pick affects your interest rate, payment schedule, and more.

One big choice is between a fixed-rate mortgage and an adjustable-rate mortgage, or ARM. A fixed-rate mortgage keeps the same interest rate forever. Your payments stay steady, which helps with planning. An ARM, though, starts with a lower rate that can change later. This might save you money at first, but payments could rise down the road.

You’ll also hear about conventional loans and government-backed loans. Conventional loans come from private lenders and often need a strong credit score and a bigger down payment. Government-backed loans—like FHA, VA, and USDA loans—get support from federal programs. They’re easier to qualify for, especially if your credit isn’t perfect or your savings are low.

What Are FHA Loans?

FHA loans, backed by the Federal Housing Administration, help people buy homes with less money upfront. They’re great for first-time buyers. To get an FHA mortgage, you need a credit score of at least 500—though 580 is better—a down payment of 3.5%, and a debt-to-income ratio under 43%.

I remember shopping for my first home. My credit was okay, but I didn’t have much saved. An FHA loan caught my eye because of the low down payment. I met with a mortgage broker who made it all clear—step by step. She helped me pull together my paperwork and calmed my nerves. It felt good to have support.

How to Apply for an FHA Mortgage

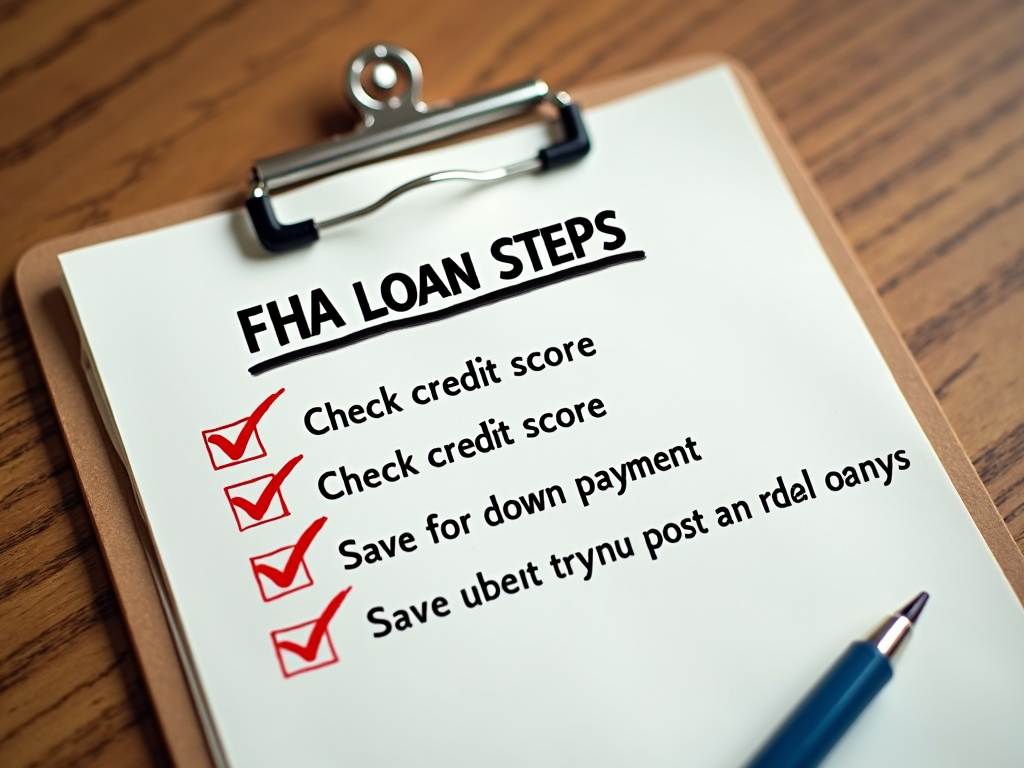

Ready to apply for an FHA mortgage? Here’s what to do:

- Check your credit score: Aim for at least 580. Below that, work on boosting it first.

- Save for a down payment: You’ll need 3.5% of the home’s price ready.

- Get pre-approved: This shows how much you can borrow and proves you’re serious to sellers.

- Find a lender: Look for one experienced with FHA loans. Compare rates and reviews.

- Gather documents: Have pay stubs, tax returns, and bank statements handy.

- Submit your application: Once you pick a home, send everything to your lender.

FHA loans have perks, like easier approval and smaller down payments. But there’s a catch—you pay mortgage insurance premiums (MIP) for the whole loan term. That adds to your costs. Plus, FHA loans have borrowing limits, which might not work for pricey areas.

Think about your needs when choosing a mortgage. If you’re staying put for years, a fixed-rate mortgage offers peace of mind. Planning to move soon? An ARM might save you money early on. It’s all about what fits your life.

There’s also VA loans for veterans and their families. These come with no down payment and no extra insurance costs. USDA loans are another option for rural buyers, offering low rates and no money down if you qualify.

My sister bought a home in a small town and used a USDA loan. She couldn’t believe she didn’t need a down payment. It opened the door to owning a home way sooner than she expected. Seeing her excitement was awesome.

Customizing Your Mortgage

Beyond types, you can tweak your loan. A 15-year term pays it off faster and cuts interest, but monthly payments jump. A 30-year term keeps payments lower but costs more over time.

You can also pick between fixed or adjustable rates. Some loans blend both—a fixed rate for a few years, then it adjusts. It’s a middle ground if you’re unsure.

Ever heard of points? They’re fees you pay upfront to lower your interest rate. One point costs 1% of your loan and might drop your rate by 0.25%. It’s a trade-off—spend now to save later. Run the numbers to see if it works for you.

When I got my mortgage, I shopped around hard. Some lenders budged on fees or points when I asked. It taught me to speak up—you might score a better deal just by asking.

Wrapping It Up

Understanding mortgage types and options is your ticket to a smart homebuying choice. Fixed-rate, ARM, FHA, VA, USDA—each has its strengths. Match them to your budget and plans. Research well, talk to lenders, and don’t rush. The right mortgage sets you up for success.

Owning a home is a big deal, and your mortgage shapes your financial future. Take time to learn your options. Ask questions until it’s clear. With the perfect loan, that dream home is yours—and your wallet stays happy too.