Buying a home is one of the biggest financial decisions you'll ever make. But understanding home loans can feel overwhelming, especially if you're a first-time buyer. In this guide, we'll break down the basics of home loans, with a special focus on FHA loans, their benefits, and what you need to know to get pre-approved in 2024. Whether you're just starting to explore your options or you're ready to apply, this article will provide you with the knowledge and confidence to navigate the home loan process.

A home loan, also known as a mortgage, is a loan provided by a bank or mortgage lender to help you purchase a home. You borrow a certain amount of money and agree to pay it back over time, usually with interest. The home itself serves as collateral, which means if you fail to make payments, the lender can take possession of the property.

Think of it like this: Instead of paying the full price of the house upfront, you're spreading the cost over many years, making it more affordable month-to-month.

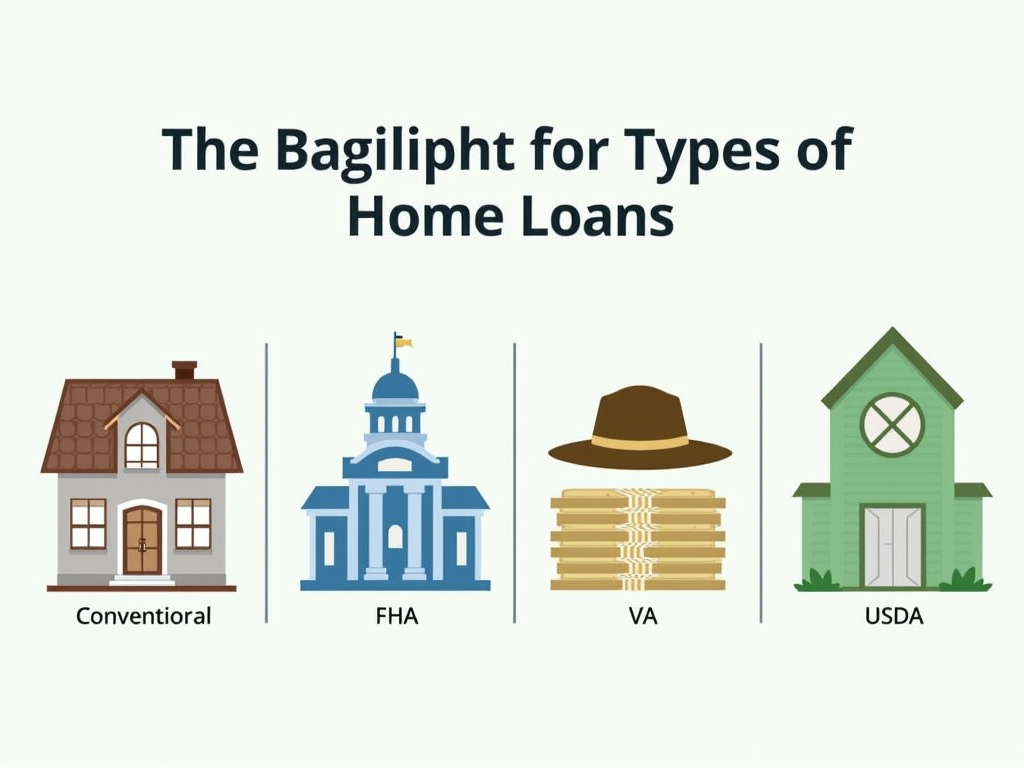

There are several types of home loans available, each with its own set of requirements and benefits. The most common types include:

-

Conventional Loans: These are not insured by the government and typically require a higher credit score and down payment.

-

FHA Loans: Backed by the Federal Housing Administration, these loans are designed for low-to-moderate income borrowers and often have more lenient credit requirements.

-

VA Loans: Available to veterans and active military members, these loans offer favorable terms and often require no down payment.

-

USDA Loans: Aimed at rural homebuyers, these loans offer low interest rates and no down payment for eligible properties.

In this article, we'll focus on FHA loans, as they are a popular choice for first-time homebuyers.

An FHA loan is a mortgage insured by the Federal Housing Administration. This means that if you default on the loan, the FHA will cover the lender's losses. Because of this insurance, lenders are more willing to offer loans to borrowers who might not qualify for conventional loans.

FHA loans are particularly beneficial for:

- First-time homebuyers

- Borrowers with lower credit scores

- Those who can only afford a small down payment.

To qualify for an FHA loan, you'll need to meet certain criteria, such as having a steady income, a valid Social Security number, and a property appraisal from an FHA-approved appraiser.

There are several advantages to choosing an FHA loan:

-

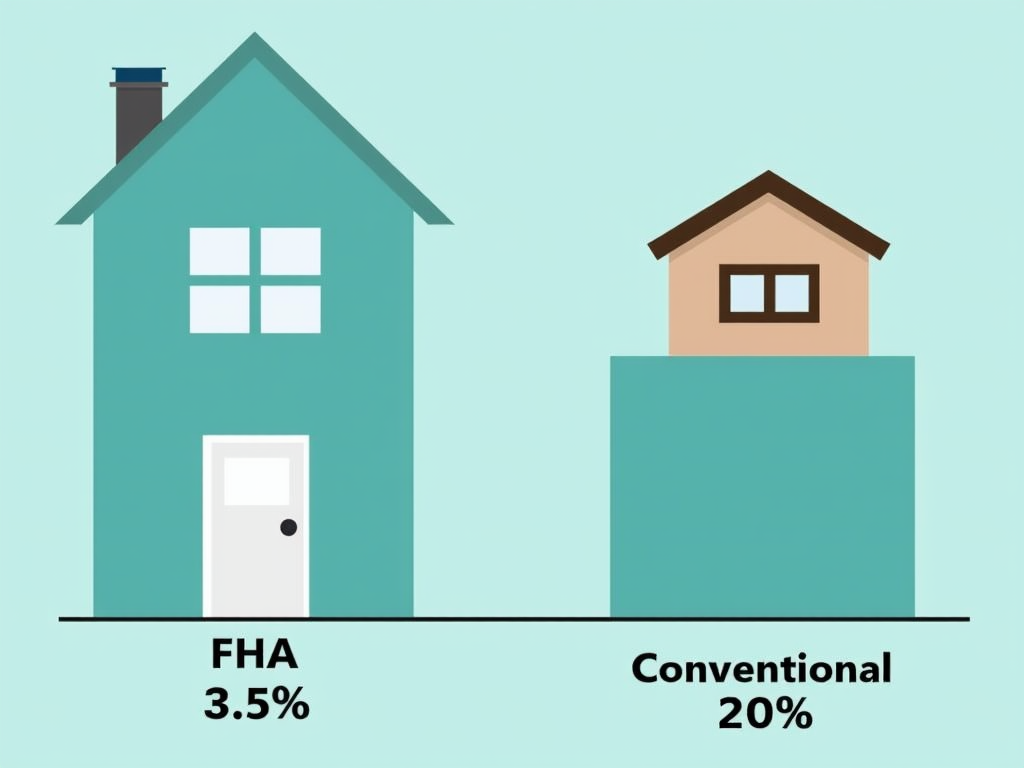

Lower Down Payment: You can qualify for an FHA loan with a down payment as low as 3.5% of the purchase price, compared to the 20% often required for conventional loans.

-

Lenient Credit Requirements: FHA loans are more forgiving of past credit issues. You can qualify with a credit score as low as 580, and in some cases, even lower.

-

Assumable Loans: If you sell your home, the buyer can take over your FHA loan, which can be an attractive selling point.

-

Rehabilitation Loans: FHA offers 203(k) loans that allow you to finance both the purchase and renovation of a home.

-

Lower Closing Costs: Sellers can contribute up to 6% of the purchase price towards closing costs, reducing your out-of-pocket expenses.

Getting pre-approved for an FHA loan is an important step in the home buying process. It shows sellers that you're a serious buyer and gives you a clear idea of how much you can afford. Here's a checklist to help you prepare for pre-approval in 2024:

- Proof of Income: Gather your last two pay stubs, W-2 forms from the past two years,