Overview: A credit score is a three-digit number that represents your creditworthiness. It's used by lenders to assess the risk of lending you money. Understanding your credit score is crucial for managing your financial health and achieving your financial goals.

What is a Credit Score? A credit score is a numerical representation of your credit history. It's calculated based on information in your credit report, which includes your payment history, the amount of debt you owe, the length of your credit history, and other factors. Lenders use your credit score to determine whether to approve your loan applications and what interest rates to offer you.

Why Credit Scores Matter Your credit score can have a significant impact on your financial life. A high credit score can help you qualify for better loan terms, lower interest rates, and even better insurance premiums. On the other hand, a low credit score can make it difficult to get approved for loans or credit cards, and you may end up paying higher interest rates.

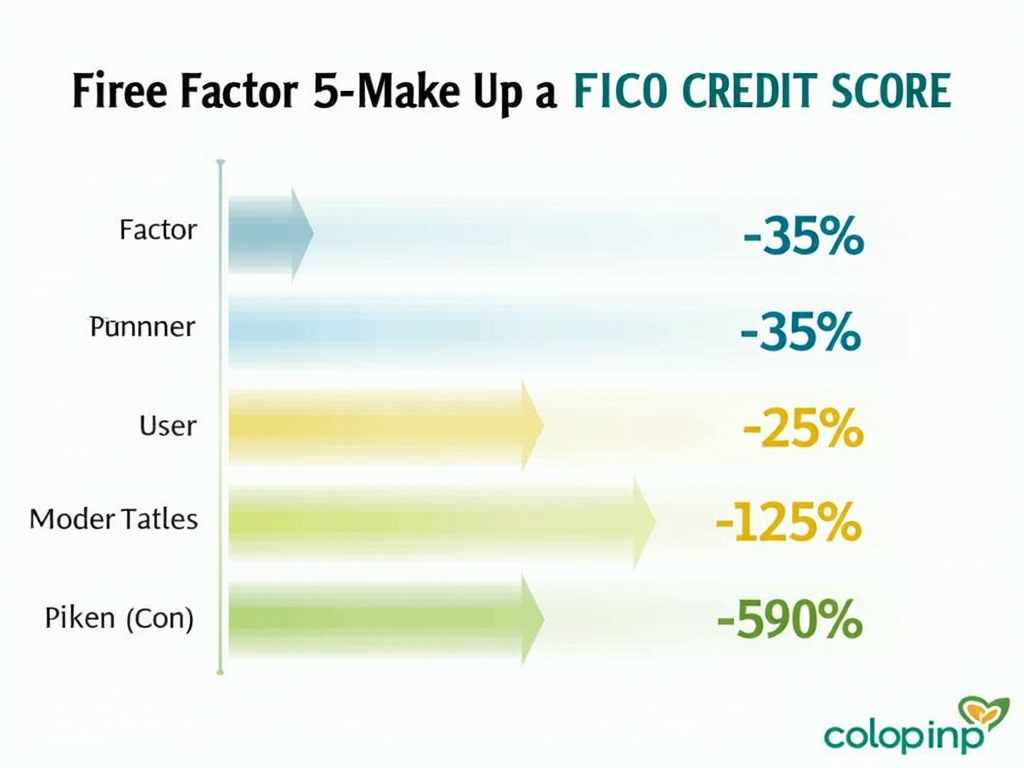

How Credit Scores Are Calculated Credit scores are calculated using complex algorithms that analyze your credit history. The most common credit scoring model is the FICO score, which ranges from 300 to 850. The higher your score, the better your creditworthiness.

The FICO score is based on five main factors:

-

Payment History (35%): This is the most important factor. It includes whether you've paid your bills on time, any late payments, and any bankruptcies or foreclosures.

-

Amounts Owed (30%): This factor looks at how much debt you owe compared to your credit limits. It's also known as your credit utilization ratio.

-

Length of Credit History (15%): This factor considers how long you've had credit accounts open. A longer credit history can positively impact your score.

-

Credit Mix (10%): This factor looks at the types of credit you have, such as credit cards, installment loans, and mortgages. A diverse credit mix can be beneficial.

-

New Credit (10%): This factor considers how many new credit accounts you've opened recently. Opening too many accounts in a short period can negatively impact your score.

Factors That Affect Your Credit Score Several factors can influence your credit score, both positively and negatively. Understanding these factors can help you make informed decisions about your credit.

Positive Factors:

-

Paying your bills on time

-

Keeping your credit card balances low

-

Having a long credit history

-

Maintaining a diverse mix of credit types

Negative Factors:

-

Late or missed payments

-

High credit card balances

-

Applying for too much credit in a short period

-

Bankruptcies or foreclosures

How to Improve Your Credit Score Improving your credit score takes time and effort, but it's possible with the right strategies. Here are some tips to help you boost your credit score:

-

Pay Your Bills on Time: This is the most important factor in your credit score. Set up reminders or automatic payments to ensure you never miss a due date.

-

Reduce Your Debt: Pay down your credit card balances to lower your credit utilization ratio. Aim to keep your balances below 30% of your credit limits.

-

Avoid Opening Too Many New Accounts: Each new credit application can temporarily lower your score. Only apply for credit when necessary.

-

Check Your Credit Report Regularly: Monitor your credit report for errors or inaccuracies. You can get a free copy of your credit report from each of the three major credit bureaus once a year.

-

Consider a Secured Credit Card: If you have a low credit score, a secured credit card can help you build credit. Just make sure to use it responsibly.

Credit Scores and Mortgage Rates Your credit score plays a crucial role in determining the interest rate you'll receive on a mortgage. Lenders use your credit score to assess the risk of lending you money, and a higher score can lead to better mortgage rates.

For example, according to the FHA mortgage guidelines 2023, borrowers with a credit score of 580 or higher may qualify for an FHA loan with a down payment as low as 3.5%. However, borrowers with a credit score between 500 and 579 may still qualify but will need to make a larger down payment of at least 10%.

It's important to note that FHA guidelines can change, so it's essential to stay up-to-date with the latest requirements. For more information on FHA mortgage guidelines, you can visit the official FHA website.

Personal Insights As someone who has navigated the world of credit scores, I can attest to the importance of understanding and managing your credit. When I first started building my credit, I made the mistake of maxing out my credit cards, which negatively impacted my score. It took time and discipline to pay down my debt and improve my score, but it was worth it in the end.

One thing I've learned is that patience is key when it comes to credit scores. It takes time to build a good credit history, and there's no quick fix for improving your score. However, by following the tips mentioned earlier and being consistent with your financial habits, you can achieve a healthy credit score.

Summary Understanding your credit score is essential for managing your financial health. By knowing what factors influence your score and how to improve it, you can take control of your credit and achieve your financial goals. Remember to pay your bills on time, keep your debt levels low, and monitor your credit report regularly.