Overview

The FHA appraisal process is a key step in securing an FHA mortgage. It checks if a home is safe, sound, and worth the loan amount. In this article, we’ll explain the FHA appraisal process in detail, share what happens during it, and offer practical tips to help you succeed.

What Is an FHA Appraisal?

An FHA appraisal is a professional evaluation of a home’s value and condition. It’s required when you apply for an FHA mortgage, a loan backed by the Federal Housing Administration. Unlike a regular appraisal, which mainly focuses on value, an FHA appraisal also ensures the property meets strict safety and quality standards. Think of it as a double-check: it protects you and the lender by confirming the home is a good investment.

I remember when my cousin Jake bought his first house with an FHA loan. He was surprised the appraisal wasn’t just about price. The appraiser actually flagged a broken stair rail that needed fixing before the loan could go through. It’s this focus on livability that sets the FHA appraisal apart.

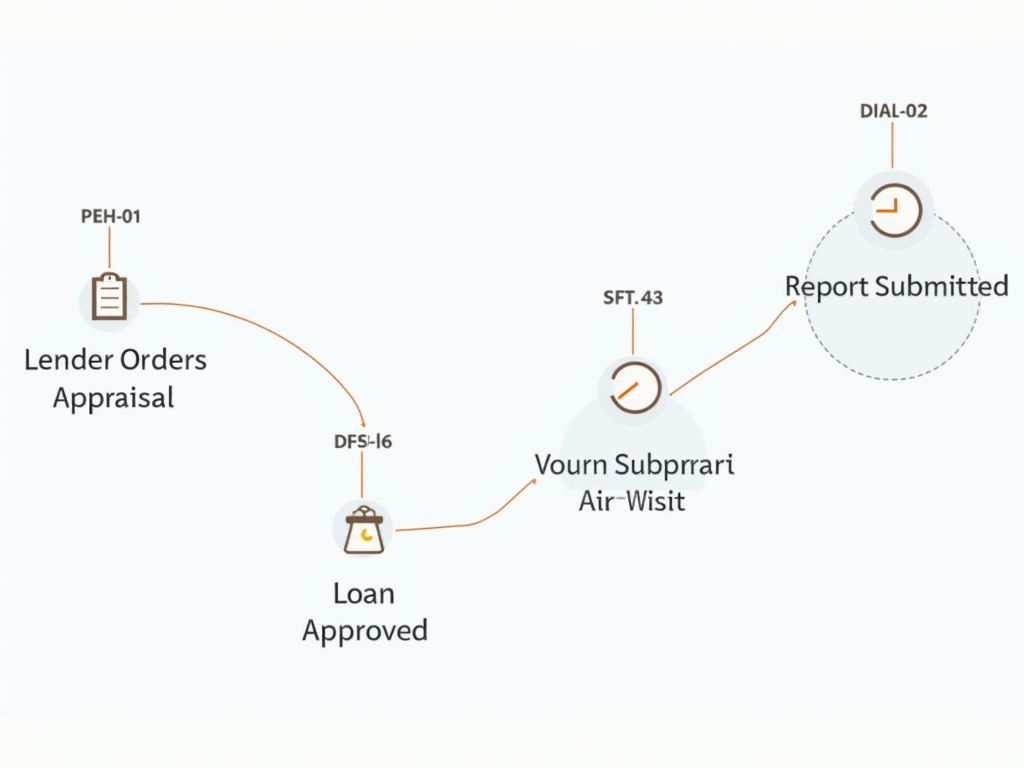

How Does the FHA Appraisal Process Work?

The FHA appraisal process follows clear steps. First, your lender orders the appraisal after you sign a purchase agreement. An FHA-approved appraiser then visits the property. They inspect it inside and out, taking notes and photos. After the visit, they write a report with their findings on value and condition. Finally, the lender reviews the report to decide if the loan can move forward.

The whole thing usually takes about a week, depending on how busy appraisers are in your area. If repairs are needed, it might take longer. Jake’s appraisal took 10 days because the appraiser found that stair issue I mentioned earlier.

What Do Appraisers Look For?

During an FHA appraisal, the appraiser checks three main things: condition, safety, and value. They want to see that the home is in good shape—no major damage like leaky roofs or cracked walls. Safety is huge too. They look for working smoke detectors, secure handrails, and no hazards like exposed wiring. For value, they compare the home to similar ones nearby to make sure it’s worth the loan amount.

You can find the full list of requirements on the U.S. Department of Housing and Urban Development (HUD) website, which sets the rules for FHA appraisals. It’s a good resource if you want to dig deeper into the standards.

How It Affects Your FHA Mortgage

The appraisal directly impacts your FHA mortgage approval. If the home’s value matches or exceeds the loan amount, and it meets FHA standards, you’re in the clear. But if the value is too low or repairs are needed, it can delay things. You might need to negotiate with the seller to fix issues or adjust the price.

When my friend Sarah went through this, her appraisal came in $5,000 below the asking price. She worked with the seller to lower the cost, and it all worked out. It’s a reminder that the appraisal isn’t just a hurdle—it’s a tool to protect you from overpaying.

Common Issues and How to Avoid Them

Some problems pop up often in FHA appraisals. Repairs are a big one—things like peeling paint or broken windows can stop the process. Valuation gaps happen too, where the home’s worth doesn’t match the loan. Delays can also occur if the appraiser’s schedule is packed.

Here’s a quick list of common issues: - Repairs Needed: Fix small stuff like leaks or missing handrails ahead of time. - Low Valuation: Research local home prices to set realistic expectations. - Delays: Book the appraisal early to avoid waiting.

A study from the University of Illinois found that appraisals often flag minor safety issues that owners overlook. Catching these early can save you stress.

How to Prepare for an FHA Appraisal

Getting ready for an FHA appraisal is straightforward. Start by checking your home for safety features—install smoke detectors and secure loose railings. Fix small repairs like cracked tiles or chipped paint. Clean up the yard and make the place look welcoming. It’s like getting your house ready for a guest, but with a checklist.

Sarah told me she walked through her trouvailles with a flashlight before her appraisal. She found a wobbly fence post and fixed it herself. That little effort paid off when the appraiser gave her home a thumbs-up.

If something goes wrong, don’t panic. Talk to your lender about options. Sometimes, you can get a second appraisal or appeal the report. It’s not over until the loan’s denied, so stay proactive.

FHA Appraisal vs. Conventional Appraisal

Here’s a quick comparison to clarify how FHA appraisals differ:

| Feature | FHA Appraisal | Conventional Appraisal |

|---|---|---|

| Purpose | Value and condition check | Mostly value check |

| Standards | FHA minimum property rules | No strict condition rules |

| Appraiser | Must be FHA-approved | Any licensed appraiser |

| Cost | About the same | About the same |

This table shows why FHA appraisals are stricter—it’s all about protecting the buyer and the lender.

Summary

The FHA appraisal process might feel overwhelming, but it’s manageable with preparation. Choose an FHA-approved appraiser, ensure your home meets safety standards, and fix issues early. It’s your chance to confirm the home is worth it and safe to live in. Want to learn more? Check out the recommended readings below.