Looking to simplify your FHA mortgage? An FHA streamline refinance might be the answer. It’s a fast, easy way for homeowners with an existing FHA loan to lower monthly payments or snag a better interest rate. Less paperwork, fewer hurdles—just savings. Let’s dive into what it is and if it fits your needs.

So, who can get an FHA streamline refinance explained in simple terms? You need an existing FHA loan—sorry, no conventional loans here. You must be up-to-date on payments, with no late ones in the past year. You’ve got to have owned your home for at least six months. Oh, and the refinance has to help you—like cutting your rate or stabilizing your loan. Lenders might tweak these rules a bit, so shop around!

The perks are pretty sweet. First, it can shrink your monthly payment. How? A lower interest rate or a longer loan term. The FHA says you might drop your rate by about 0.5%—that’s real money over time. Plus, the process is a breeze—less paperwork than a regular refinance. Often, no appraisal or credit check is needed. I remember skipping the appraisal when I refinanced my FHA mortgage. My home value had dipped, so that saved me a headache!

But it’s not all sunshine. There are costs—like closing fees (2-5% of your loan) and an upfront mortgage insurance premium (1.75%). For a $200,000 loan, that’s $3,500 just for the premium. You can’t pull cash out either, so if you need equity, look elsewhere. And if you’re moving soon, the savings might not cover the costs. I had to crunch numbers to see if it worked for me long-term.

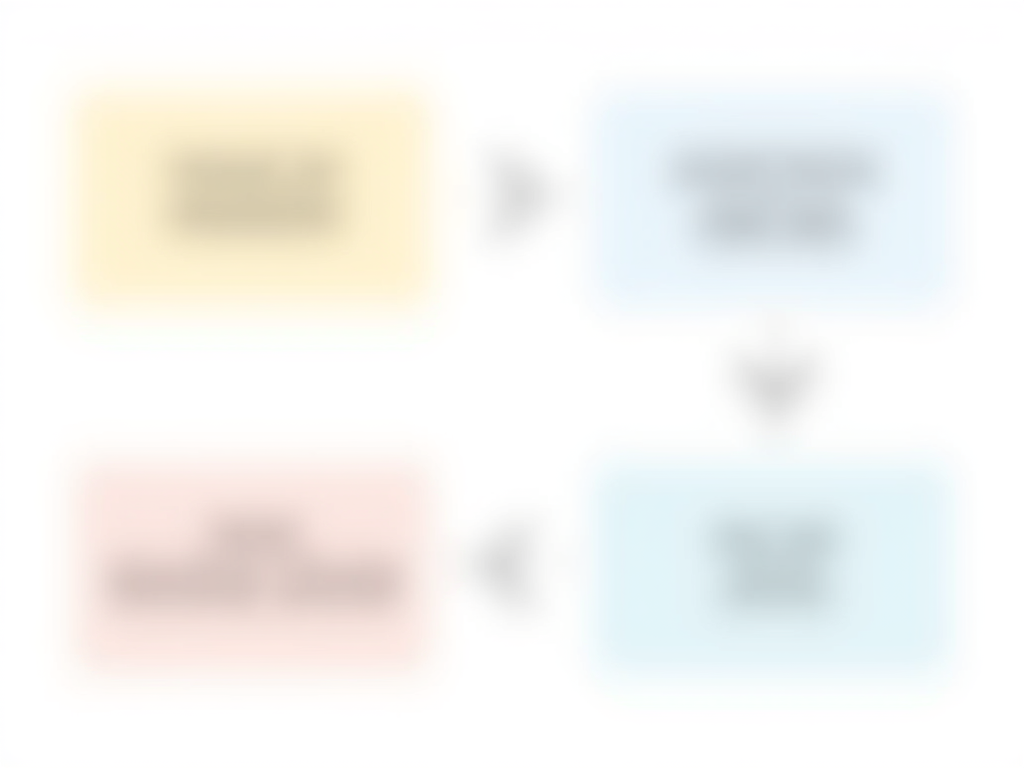

Here’s how it works:

- Call a lender who does FHA loans. Tell them you want a streamline refinance.

- Hand over some papers—think pay stubs or job proof, but way less than usual.

- Wait for approval—they’ll check your loan and offer new terms.

- Sign and close—wrap it up, often in 30 days.

Faster than the 45-60 days of a typical refinance, right? It’s like express checkout for your mortgage.

Costs can sting a bit upfront. Closing costs might hit $4,000-$10,000 on a $200,000 loan, plus that 1.75% mortgage insurance fee. Good news? You can roll them into the loan—no cash needed now. Some lenders pitch ‘no-cost’ options, but watch out—those often mean higher rates. Check out Understanding Mortgage Insurance Premiums for more on that fee.

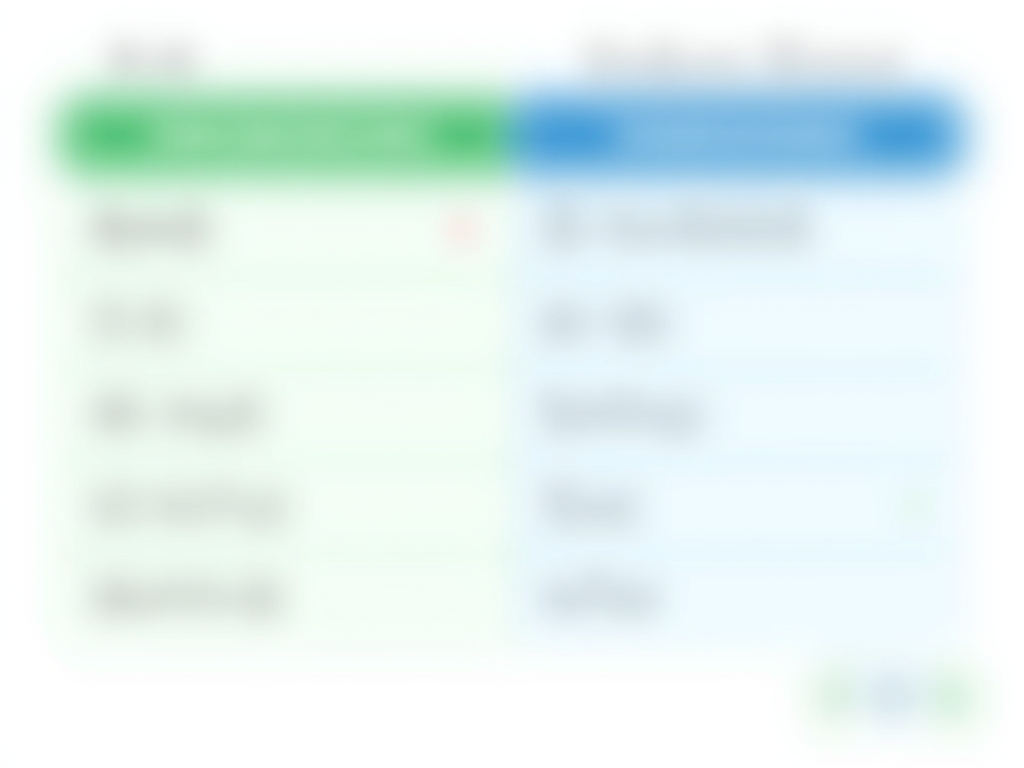

How does it stack up? A traditional refinance needs an appraisal and credit check—more work, but you might score a lower rate or cash out. A cash-out refinance taps your equity, perfect if you need funds, though it’s tougher to get. Conventional loans? They’re an option if you’ve got strong credit, but not for FHA folks. Your goals—savings or cash—decide what’s best.

Here’s the bottom line: an FHA streamline refinance is great if you’ve got an FHA mortgage and want simpler, cheaper payments. It’s quick, light on hassle, and can save you cash long-term. But those upfront costs and no cash-out rule? Dealbreakers for some. Talk to a few lenders—compare rates and fees. It worked for me when I stayed put, but your situation might differ.