FHA loans are a popular choice for homebuyers, especially those buying their first home. They offer several advantages, such as lower down payments and more lenient credit requirements compared to conventional loans. However, one key aspect to understand is the FHA loan limit, which determines the maximum amount you can borrow in your area. These limits vary depending on where you live, reflecting the local housing market. In this article, we'll explore what FHA loan limits are, how to find them, and why they matter. We'll also cover the credit score requirements for FHA loans and highlight the WEIGHT and potential drawbacks of choosing this type of mortgage. By the end, you'll have a clear understanding of whether an FHA loan is right for you and how to navigate the process.

What are FHA Loans?

FHA loans are mortgages insured by the Federal Housing Administration (FHA), which is part of the U.S. Department of Housing and Urban Development (HUD). This insurance protects lenders against losses if borrowers default on their loans, making it less risky for lenders to offer mortgages to individuals who might not qualify for conventional loans.

Unlike conventional loans, which are not government-backed, FHA loans are designed to make homeownership more accessible. They are particularly popular among first-time homebuyers, but they can be used by anyone who meets the eligibility criteria.

Understanding FHA Loan Limits

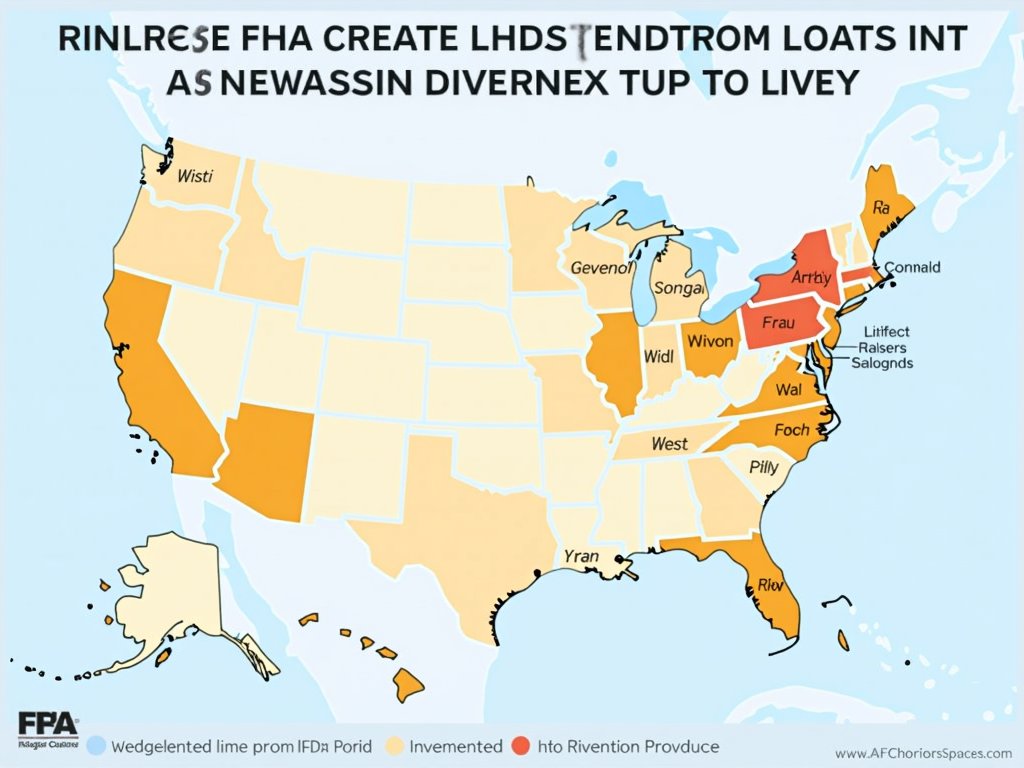

FHA loan limits are the maximum amounts that borrowers can obtain through an FHA-insured mortgage. These limits are set by the FHA and vary by location, based on the median home prices in each area. The idea is to ensure that FHA loans are used for modest housing, in line with the program's goal of promoting affordable homeownership.

For example, in areas where home prices are high, such as major metropolitan cities, the loan limits are higher to accommodate the cost of housing. Conversely, in rural or less expensive areas, the loan limits are lower. For 2023, the standard FHA loan limit for a single-family home is $472,030 in most parts of the country. However, in high-cost areas, it can be as high as $1,089,300.

When I was house hunting, I initially set my sights on a property that was just above the FHA loan limit in my area. After learning about the limit, I had to reassess my options and focus on homes within the allowable range. It was a valuable lesson in understanding how loan limits can impact your homebuying journey.

How to Find FHA Loan Limits in Your Area

To determine the FHA loan limit for your specific location, you can use the online lookup tool provided by the U.S. Department of Housing and Urban Development (HUD). Here's how:

- Visit the HUD FHA loan limit lookup page.

- Select your state from the dropdown menu.

- Choose your county.

- Click 'Send' to view the current loan limits for that area.

The tool will display the loan limits for different property types, such as single-family homes, duplexes, triplexes, and fourplexes. Make sure to select the appropriate property type for your needs.

Additionally, you can contact a local lender or mortgage broker, as they often have access to up-to-date information on FHA loan limits and can provide guidance tailored to your situation.

FHA Loan Credit Score Requirements

One of the key benefits of FHA loans is their flexibility when it comes to credit scores. While conventional loans often require a credit score of 620 or higher, FHA loans have a lower threshold.

- If your credit score is 580 or above, you may qualify for a down payment as low as 3.5%.

- If your credit score is between 500 and 579, you can still qualify, but you'll typically need to make a down payment of at least 10%.

- Scores below 500 may not be eligible for FHA financing.

It's worth noting that while the FHA sets these minimum requirements, individual lenders may have their own overlays, meaning they might require higher credit scores or additional documentation. Therefore, it's a good idea to shop around and compare offers from different lenders.

Tip: If your credit score is close to the threshold, consider taking steps to improve it before applying. Even a small boost in your score could help you qualify for better terms.

Benefits of FHA Loans

FHA loans offer several advantages that make them an attractive option for many borrowers:

- Lower down payments: With a minimum down payment of just 3.5%, FHA loans allow you to buy a home with less money upfront compared to the 5-20% typically required for conventional loans.

- More lenient credit requirements: Borrowers with lower credit scores can still qualify, making homeownership accessible to a broader range of people.

- Assumable loans: FHA loans can be transferred to a new buyer when you sell your home, which can be beneficial if interest rates have risen since you took out the loan.

- Financing for home improvements: The FHA 203(k) program allows you to finance both the purchase and renovation of a home, which is ideal for buyers looking at fixer-uppers.

- Flexible debt-to-income ratios: FHA loans may allow higher debt-to-income ratios than conventional loans, making it easier to qualify if you have existing debts.

Moreover, FHA loans can be used for a variety of property types, including single-family homes, multi-family homes (up to four units), and FHA-approved condominiums.

Considerations and Drawbacks

While FHA loans have many benefits, there are also some potential downsides to consider:

- Mortgage insurance premiums (MIP): FHA loans require both an upfront MIP (which can be financed into the loan) and annual premiums paid monthly. These insurance costs can make FHA loans more expensive over time compared to conventional loans, especially if you have a good credit score and can qualify for a conventional loan without private mortgage insurance (PMI).

- Loan limits: The maximum loan amount is capped, which might limit your purchasing power in high-cost areas where home prices exceed the FHA limits.

- Property standards: The property must meet certain safety and habitability standards set by the FHA. This could mean additional inspections or required repairs before closing, which might delay the process or add to the cost.

- Occupancy requirements: FHA loans are intended for owner-occupied properties, so you must live in the home as your primary residence. They cannot be used for investment properties.

Considering these factors, it's important to evaluate whether an FHA loan aligns with your financial situation and homebuying goals. For some, the benefits outweigh the drawbacks, while others might find that a conventional loan or other mortgage options are more suitable.

In conclusion, FHA loans are a valuable tool for many homebuyers, offering a path to homeownership with lower barriers to entry. By understanding the loan limits in your area, you can determine how much you can borrow and set realistic expectations for your home search. Additionally, knowing the credit score requirements and the benefits and drawbacks of FHA loans will help you make an informed decision about whether this type of mortgage is right for you. Remember to consult with lenders and explore all your options to find the best fit for your needs.