Stepping into homeownership can feel overwhelming, especially if it’s your first time. That’s where FHA loans come in. This guide breaks down The Beginner's Guide to FHA Loans into simple, actionable steps. Whether you’re curious about down payments or FHA refinancing rates and terms, we’ve got you covered with clear insights and tips.

What Are FHA Loans?

An FHA loan is a mortgage backed by the Federal Housing Administration, or FHA. It’s a government program created to help people buy homes, especially if they’re new to the process or have lower credit scores. Unlike regular loans from banks, FHA loans make it easier to get approved and often come with better terms.

Why FHA Loans Work for Beginners

Here’s why so many first-timers love FHA loans:

- Small Down Payments: You only need 3.5% of the home’s price upfront. That’s way less than the 20% some loans ask for.

- Easier Credit Rules: A credit score as low as 580 can qualify you. Even scores between 500-579 might work with a bigger down payment.

- Lower Interest Rates: The government backing keeps rates competitive.

- Future Flexibility: If you sell, the buyer can take over your loan, making your home more appealing.

Who Can Get an FHA Loan?

Not everyone qualifies, but the rules are pretty friendly. Here’s what you need:

- Credit Score: Aim for 580 or higher for the 3.5% down payment. Below that, you’ll need 10%.

- Debt-to-Income Ratio: Your monthly debts shouldn’t be more than 43% of your income.

- Steady Job: Show two years of solid work history.

- Safe Home: The house must pass FHA safety checks.

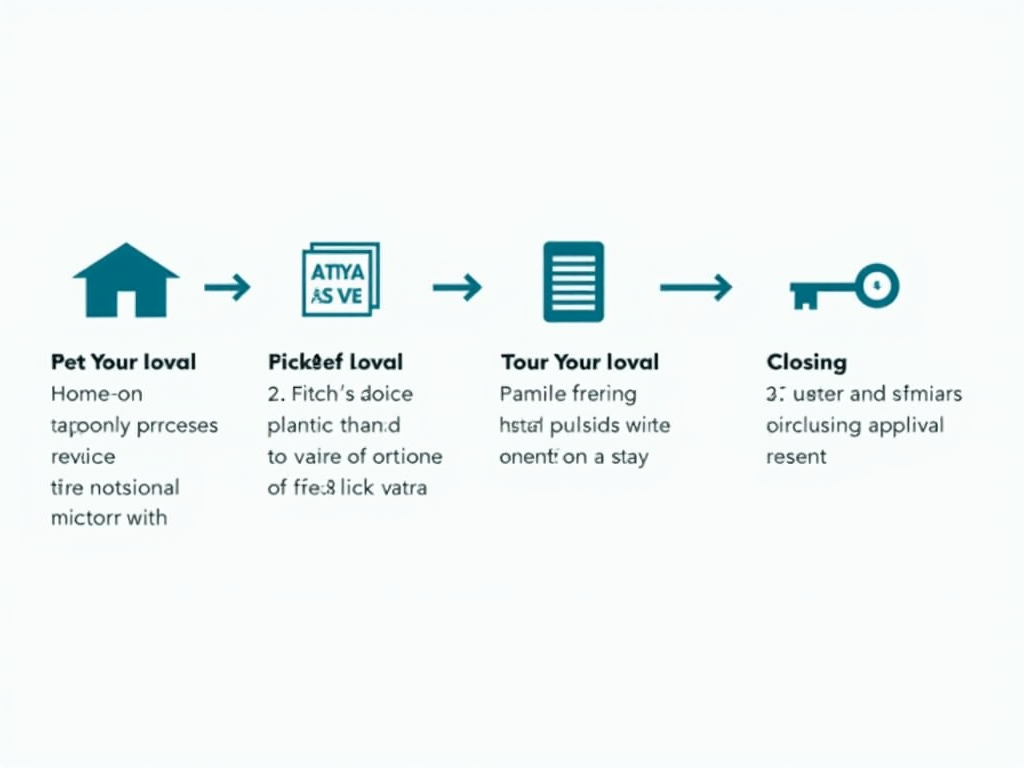

How to Apply for an FHA Mortgage

Getting an FHA mortgage is straightforward. Follow these steps:

- Pre-Approval: Find an FHA-approved lender and see what you can borrow.

- House Hunt: Look for a home in your price range.

- Apply: Send in your paperwork—think pay stubs and bank statements.

- Appraisal: The lender checks if the home meets FHA standards.

- Close: Sign the papers and move in!

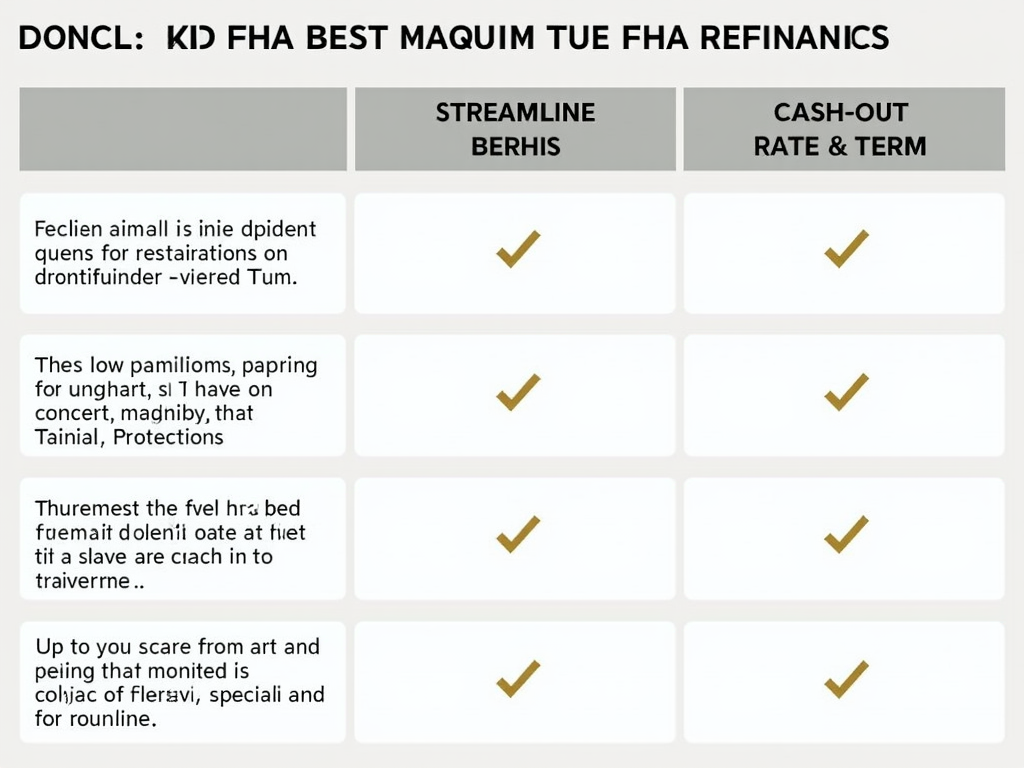

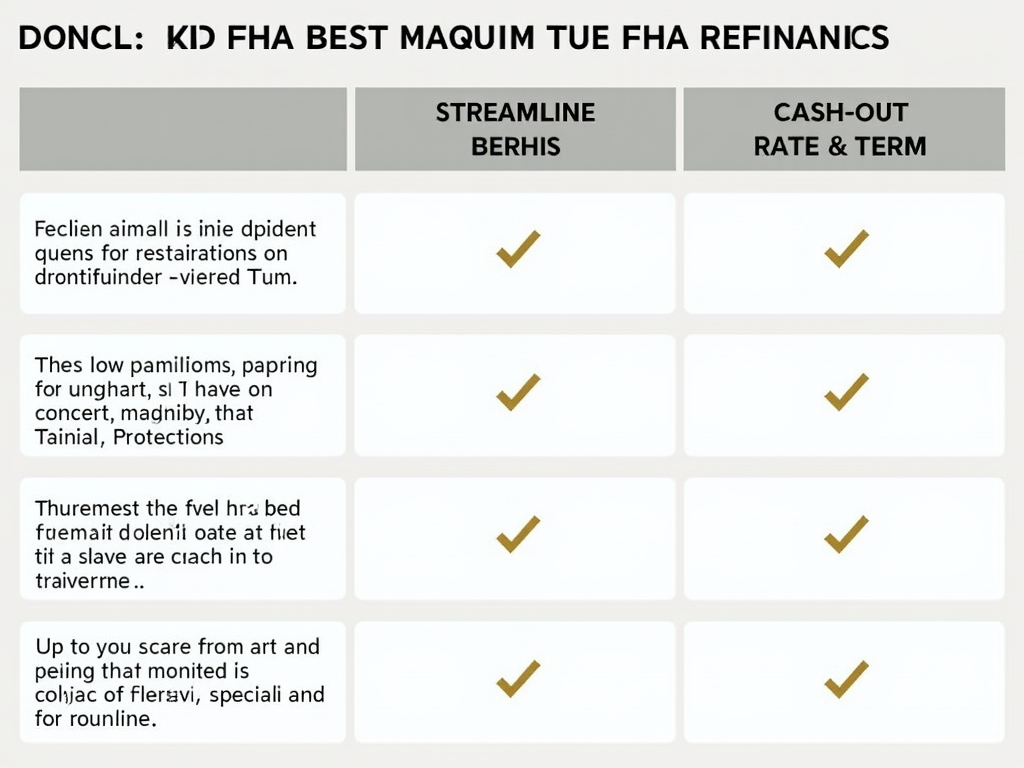

FHA Refinancing: A Smart Option

Got an FHA loan already? FHA refinancing could save you money. It’s a way to tweak your loan terms or pull cash from your home’s value. Check out these options:

- Streamline Refinance: Quick and easy, no appraisal needed—just lowers your rate.

- Cash-Out Refinance: Borrow more than you owe and use the extra cash.

- Rate and Term Refinance: Adjust your rate or loan length for better payments.

Understanding FHA Refinancing Rates and Terms

Refinancing sounds great, but what about FHA refinancing rates and terms? Rates change with the market, so compare lenders. Terms can be short (like 15 years) or long (30 years)—shorter saves interest but raises monthly costs. Watch out for closing costs, too; they’re usually 2-5% of the loan. Some lenders skip them, but rates might climb.

My FHA Loan Story

When I bought my first place, I was nervous—my credit wasn’t perfect, and I didn’t have much saved. An FHA loan changed everything. That 3.5% down payment let me move in fast, and the lower rates kept my budget happy. I even used some savings to fix up the kitchen. It wasn’t fancy, but it felt like home.

Busting FHA Loan Myths

Let’s clear up some confusion:

- Not Just for Newbies: Anyone eligible can use them, not only first-timers.

- Rates Aren’t High: They’re often lower than regular loans.

- Refinancing Is Real: You’ve got plenty of options to adjust your loan later.

Tips to Win with Your FHA Loan

Want the best deal? Try these:

- Compare Lenders: Rates vary, so shop around.

- Boost Your Credit: A little improvement can cut your rate.

- Think Ahead: Plan to switch to a regular loan later to drop extra insurance costs.

- Stay Updated: Watch market trends, especially for refinancing.

Final Thoughts

FHA loans open doors for beginners with smaller down payments and easier approvals. They’re not perfect for everyone, but they’re a solid start. Whether you’re buying or exploring FHA refinancing, take time to research. The right choice now can set you up for years of happy homeownership.