Your credit score can feel like a mystery, but it’s a huge factor in buying a home. This guide simplifies it all—explaining what it is, how to improve it, and why it matters for mortgages, including FHA loans. Ready to take control and save money? Let’s dive in!

What is a Credit Score?

A credit score is a number between 300 and 850 that shows how well you handle money. Lenders look at it to decide if they’ll loan you cash—and how much it’ll cost you. The higher your score, the better your chances of landing a great mortgage deal. I used to think it was just about paying bills, but it’s so much more than that.

How is Your Credit Score Calculated?

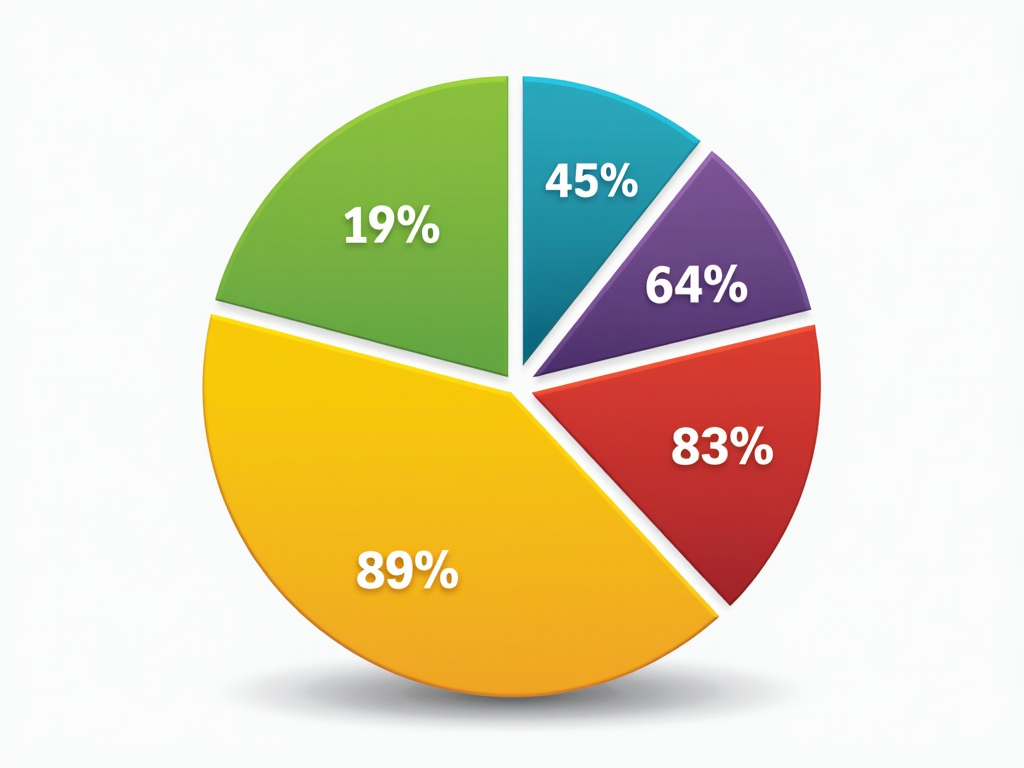

Your score comes from five key pieces. Knowing these helped me turn my credit around:

- Payment History (35%): Paying on time is huge. Miss a payment, and your score takes a hit.

- Credit Utilization (30%): This is how much of your credit you’re using. Keep it under 30%—I learned this the hard way after maxing out a card!

- Length of Credit History (15%): Older accounts boost your score.

- New Credit (10%): Opening lots of accounts fast can hurt.

- Credit Mix (10%): A mix of credit types, like cards and loans, can help.

Check out more details from the Federal Trade Commission.

Why Your Credit Score Matters for Mortgages

A good credit score can save you thousands on a mortgage. Lenders use it to set your interest rate and decide if you qualify. For example, a score over 760 might get you a low rate, while below 620 could mean rejection—or higher costs. FHA loans, though, give hope to folks with lower scores. My cousin got a mortgage with a 590 score thanks to an FHA option!

How to Boost Your Credit Score for a Mortgage

Want a better score before applying for a mortgage? Try these steps:

- Review Your Credit Report: Get it free at AnnualCreditReport.com and fix errors.

- Pay On Time: Late payments kill your score—set reminders!

- Cut Debt: Pay down cards to below 30% of your limit.

- Don’t Open New Credit: Wait until after your mortgage closes.

- Keep Old Accounts: They show you’ve got experience.

I boosted my score 50 points in six months by focusing on these. Start early—it pays off!

Understanding FHA Mortgage Insurance

An FHA mortgage is backed by the government, making it easier for people with lower scores to buy homes. But it comes with FHA mortgage insurance, or MIP. This protects the lender if you can’t pay. You’ll pay an upfront fee (1.75% of the loan) and a yearly cost (about 0.85%). It’s a trade-off—higher costs, but lower down payments. Learn more at HUD’s FHA page.

FHA Mortgage Insurance Application Tips

Applying for an FHA mortgage? Here’s how to nail it:

- Check Your Score: Aim for 580+ for a 3.5% down payment; 500-579 needs 10%.

- Gather Papers: Have pay stubs, tax returns, and bank statements ready.

- Compare Lenders: Rates vary—shop around!

- Watch Debt: Keep your debt-to-income ratio under 43%.

When I helped a friend apply, we found a lender who explained everything clearly. It made the process way less stressful.

Wrapping It Up

Your credit score isn’t just a number—it’s your ticket to a better mortgage. By understanding it and taking action, you can boost your score and open doors to homeownership, even with FHA mortgage insurance. Start today, and you’ll be ready to buy that dream home before you know it.