Have you ever wondered why some people snag low interest rates while others struggle to get approved for a loan? It often boils down to one thing: your credit score. This article breaks down Credit Score Basics, showing you what it is, why it matters, and how to make it work for you.

What is a Credit Score?

A credit score is a three-digit number that sums up how well you handle money. Think of it as a financial report card. Lenders use it to decide if you’re a safe bet for loans or credit cards. The most common type, the FICO score, ranges from 300 to 850. A higher number means you’re more likely to pay back what you borrow. Here’s a quick look at the ranges:

- 300-579: Poor

- 580-669: Fair

- 670-739: Good

- 740-799: Very Good

- 800-850: Excellent

Knowing where you stand can help you plan your next financial move.

Factors That Affect Your Credit Score

Your credit score isn’t random—it’s built from specific parts of your financial life. Here’s what counts:

- Payment History (35%): Do you pay bills on time? Late payments can hurt your score.

- Credit Utilization (30%): This is how much of your credit limit you’re using. Keeping it below 30% is a smart move.

- Length of Credit History (15%): Longer credit history usually means a better score.

- Types of Credit (10%): Having a mix—like credit cards and a car loan—can help.

- Recent Credit Inquiries (10%): Applying for lots of credit in a short time can lower your score.

Focus on these areas, and you’ll see your score start to climb.

Understanding Your Credit Report

Want to know what’s behind your credit score? Check your credit report. It’s like a detailed story of your financial past, listing your accounts, payments, and any big issues like missed payments. In the U.S., you can get a free report once a year from Equifax, Experian, and TransUnion at AnnualCreditReport.com. Understanding Your Credit Report is key to spotting mistakes—like a bill marked late that you paid on time—and fixing them to boost your score.

Why Your Credit Score Matters

Your credit score isn’t just a number—it’s a key that unlocks financial doors. A good score can get you approved for loans, snag lower interest rates, and even land better credit card deals. For example, someone with a 750 score might pay 3% on a car loan, while a 600 score could mean 10% or more. It can also affect insurance rates or job applications in some cases. Bottom line: a strong score saves you money and stress.

How to Improve Your Credit Score

Good news—you can raise your score with the right habits. Here’s How to Improve Your Credit Score for Better Loans:

- Pay on Time: Late payments are the biggest score-killer. Use reminders or auto-pay.

- Lower Debt: Keep credit card balances low—aim for under 30% of your limit.

- Keep Old Accounts: Don’t close your oldest card; it helps your history.

- Limit New Credit: Too many applications signal risk to lenders.

- Fix Errors: Review your report and dispute anything wrong.

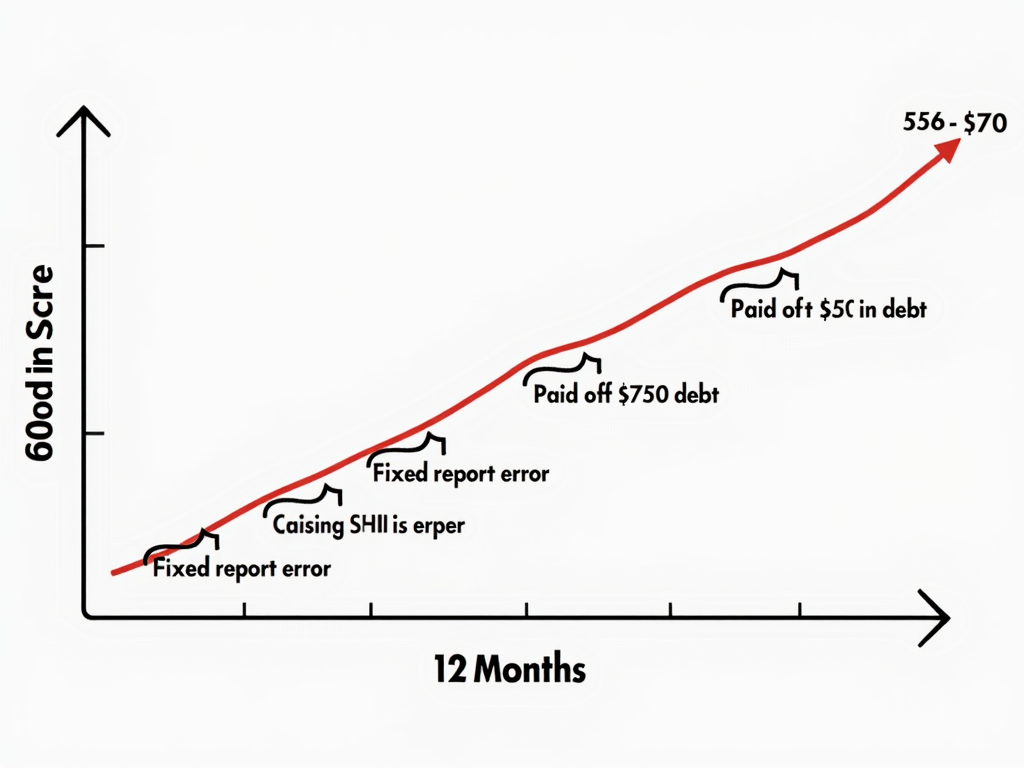

Picture this: someone I know went from a 620 to a 720 in a year by paying off debt and catching up on bills. It’s not instant, but it works.

Credit Scores and Loans

When it comes to borrowing, your credit score is front and center. A solid score can mean better loan terms—like lower rates or easier approvals. Take FHA loans, a favorite for first-time homebuyers. The FHA loan benefits include lower down payments, and you can qualify with a score as low as 580 for full financing. Part of an FHA mortgage pre-approval checklist for 2024 is your credit score, alongside income and job history. A higher score just makes the process smoother.

Common Myths About Credit Scores

Let’s clear up some confusion:

- Myth: Checking your score hurts it.

Fact: Using a free service like Credit Karma is a ‘soft’ check—no impact. - Myth: Closing old cards boosts your score.

Fact: It can shorten your history and drop your score. - Myth: You’ve got one score.

Fact: Different bureaus and models mean multiple scores.

Knowing the truth helps you make smarter moves.

Summary

Mastering Credit Score Basics sets you up for financial success. It’s about knowing what shapes your score, checking your credit report, and building good habits to improve it. Whether you’re aiming for a loan or just peace of mind, start small—pay on time, cut debt, and watch your score grow. You’ve got this!