Buying your first home is an exciting milestone, but it can also be daunting, especially when it comes to financing. That's where FHA loans come in—a government-backed option designed to make homeownership more accessible for first-time buyers. In this comprehensive guide, we'll walk you through the FHA loan requirements for first-time homebuyers, providing you with the knowledge and confidence to navigate the process.

What is an FHA Loan?

An FHA loan is a mortgage insured by the Federal Housing Administration (FHA), a part of the U.S. Department of Housing and Urban Development (HUD). This insurance protects lenders against losses if borrowers default on their loans, allowing them to offer more favorable terms to borrowers who might not qualify for conventional loans. FHA loans are particularly popular among first-time homebuyers due to their lower credit score requirements and smaller down payments. For more detailed information, visit the HUD.gov FHA Loan Information page.

Eligibility Requirements for First-Time Homebuyers

To qualify for an FHA loan as a first-time homebuyer, you need to meet certain criteria:

- Credit Score: Generally, a minimum credit score of 580 is required for a 3.5% down payment. If your credit score is between 500 and 579, you may still qualify but will need to make a 10% down payment. It's important to note that while FHA loans are more lenient, a higher credit score can still help you secure better interest rates.

- Debt-to-Income Ratio (DTI): Your DTI should not exceed 43%. This ratio compares your monthly debt payments to your gross monthly income. For example, if your monthly income is $5,000 and your monthly debt payments are $2,000, your DTI is 40%. Keeping your DTI low shows lenders that you can manage your debts responsibly.

- Employment History: You must have a steady employment history for at least two years. This demonstrates to lenders that you have a reliable source of income to make your mortgage payments.

- Property Requirements: The home you intend to purchase must be your primary residence and meet certain safety and livability standards set by the FHA. This includes passing an FHA appraisal, which ensures the property is worth the loan amount and is safe for occupancy.

For more resources on mortgage eligibility, check out the Consumer Financial Protection Bureau's Mortgage Resources.

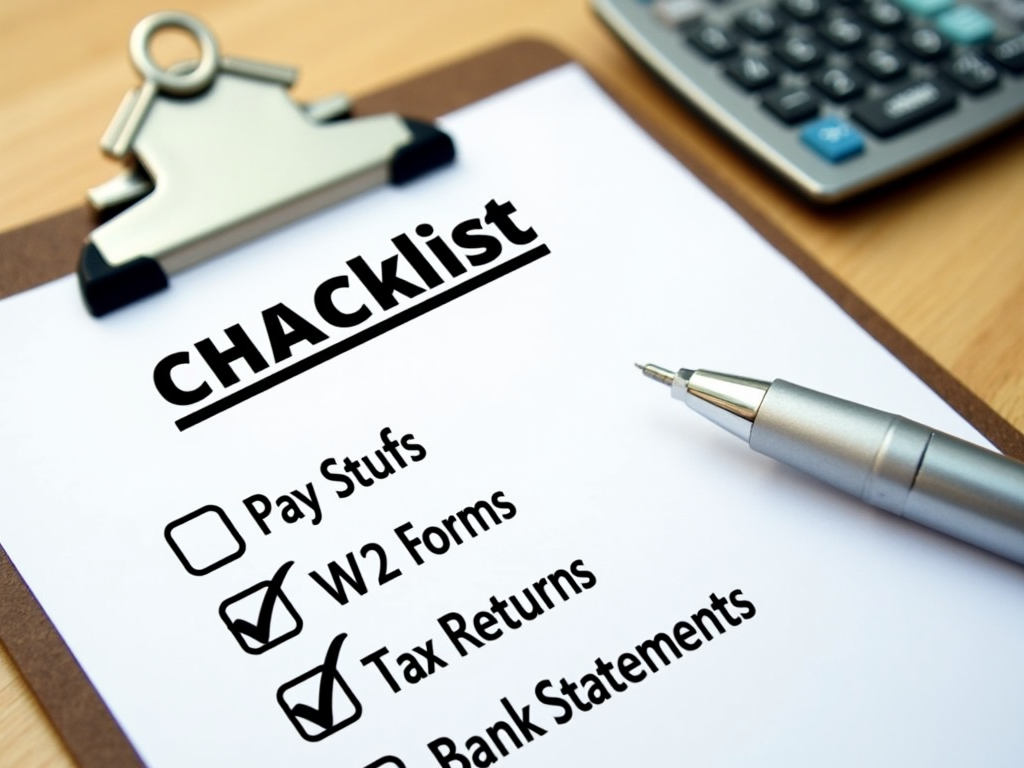

FHA Loan Documentation Checklist

When applying for an FHA loan, you'll need to provide several documents to verify your eligibility:

- Proof of Income: Recent pay stubs covering the last 30 days, W-2 forms for the past two years, and federal tax returns for the past two years. If you're self-employed, you may need to provide additional documentation, such as profit and loss statements.

- Employment Verification: A letter from your employer confirming your employment status and salary, or recent pay stubs that show year-to-date earnings.

- Credit Report: Lenders will pull your credit report to assess your creditworthiness. It's a good idea to review your credit report beforehand to correct any errors.

- Bank Statements: Statements from your checking and savings accounts for the past two months to verify your assets and ensure you have sufficient funds for the down payment and closing costs.

- Identification: A valid driver's license and Social Security card to confirm your identity.

- Property Appraisal: An FHA-approved appraiser must evaluate the property to ensure it meets FHA standards and is worth the loan amount.

Having all these documents organized and ready can streamline the application process and reduce delays.

Benefits and Drawbacks of FHA Loans

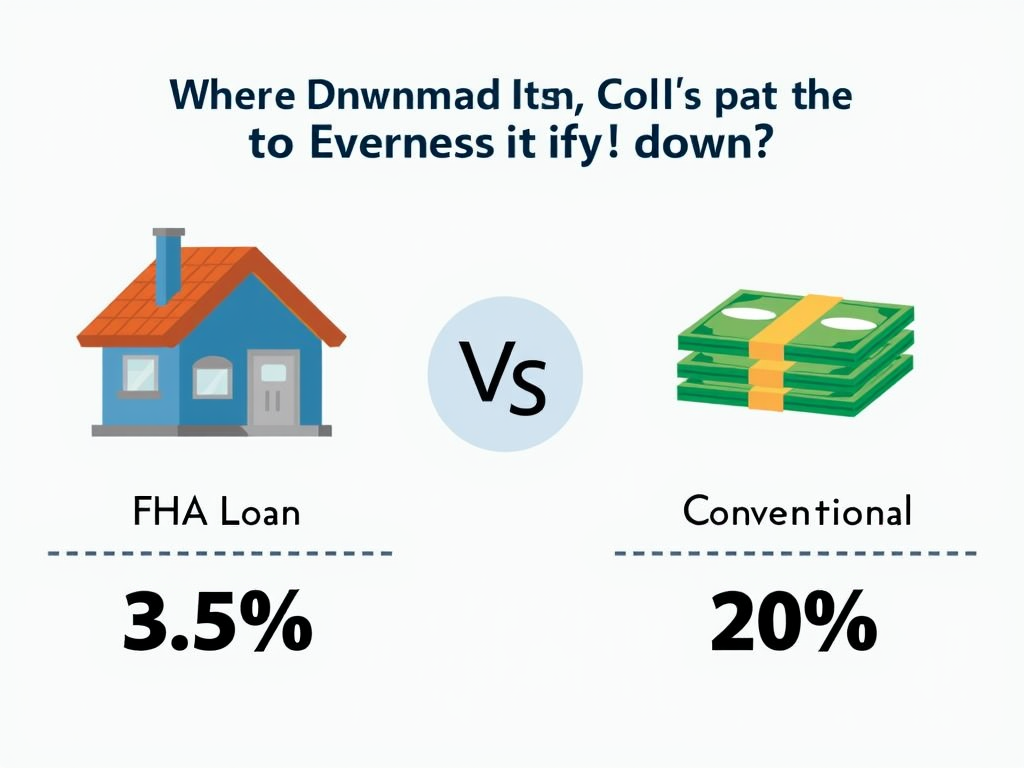

Benefits: - Lower Credit Score Requirements: Unlike conventional loans that often require credit scores of 620 or higher, FHA loans accept scores as low as 500 with a larger down payment. - Smaller Down Payments: With a credit score of 580 or higher, you can qualify for a down payment as low as 3.5% of the purchase price. This is significantly lower than the 20% typically required for conventional loans. - Competitive Interest Rates: Because FHA loans are backed by the government, lenders can offer lower interest rates compared to other loan types. - More Flexible Qualification Criteria: FHA loans consider factors beyond just credit scores, such as employment history and debt-to-income ratio, making them accessible to a wider range of borrowers.

Drawbacks: - Mortgage Insurance Premiums (MIP): FHA loans require both an upfront MIP (usually 1.75% of the loan amount) and annual premiums (ranging from 0.45% to 1.05% of the loan amount). These premiums protect the lender in case of default but add to the overall cost of the loan. - Property Standards: The home must meet specific FHA requirements, which can sometimes limit your options, especially if you're interested in fixer-uppers or properties that need significant repairs. - Loan Limits: FHA loans have maximum loan amounts based on the county where the property is located. In high-cost areas, these limits can be higher, but they may still restrict your purchasing power in certain markets.

How to Apply for an FHA Loan

- Find an FHA-Approved Lender: Not all lenders offer FHA loans, so it's crucial to choose one that is approved by the FHA. You can search for approved lenders on the HUD website or ask for recommendations from your real estate agent.

- Get Pre-Approved: Pre-approval involves submitting your financial information to a lender, who will then determine how much you can borrow. This step is essential as it helps you set a realistic budget and shows sellers that you're a serious buyer.

- Choose a Property: Look for homes that meet FHA standards and are within the loan limits for your area. Your real estate agent can help you identify properties that qualify.

- Submit Your Application: Once you've found a property, you'll need to complete the loan application and provide all required documents. Be prepared to answer questions about your financial history and the property.

- Wait for Underwriting and Approval: The lender will review your application during the underwriting process, which can take several weeks. If approved, you'll receive a commitment letter outlining the terms of the loan, and you can proceed to closing.

Tips for First-Time Homebuyers Using FHA Loans

- Improve Your Credit Score: Before applying, take steps to boost your credit score, such as paying down debts and correcting any errors on your credit report. A higher score can lead to better loan terms.

- Save for a Larger Down Payment: While 3.5% is the minimum, putting down more can reduce your monthly payments and the amount of MIP you pay over the life of the loan.

- Get Pre-Approved: Knowing your budget upfront helps you focus on homes you can afford and strengthens your offer when you find the right property.

- Work with an Experienced Agent: A real estate agent who is familiar with FHA loans can guide you through the process, from finding the right property to navigating the appraisal and closing.

- Prepare for the Appraisal: Since the property must meet FHA standards, it's wise to have a pre-inspection or choose a home that is in good condition to avoid surprises during the appraisal.

Common Mistakes to Avoid When Applying for an FHA Loan

- Not Checking Your Credit Report: Errors on your credit report can affect your eligibility. Review your report and dispute any inaccuracies before applying.

- Overlooking Closing Costs: In addition to the down payment, you'll need to cover closing costs, which can be 2-5% of the loan amount. Make sure to budget for these expenses.

- Choosing the Wrong Property: Not all homes qualify for FHA loans. Avoid properties that need significant repairs or are in poor condition, as they may not pass the appraisal.

- Ignoring Loan Limits: FHA loan limits vary by county. Ensure the property you're interested in falls within these limits to avoid disqualification.

- Failing to Shop Around: Different lenders offer different terms and fees. Compare multiple lenders to find the best deal for your situation.

By avoiding these common pitfalls, you can increase your chances of a successful FHA loan application.

In summary, FHA loans offer a viable path to homeownership for first-time buyers, especially those with lower credit scores or limited savings for a down payment. By understanding the requirements and preparing your documentation, you can navigate the process more smoothly. Remember to work with professionals who can provide guidance and support throughout your homebuying journey.

For more information on FHA loans and homebuying tips, consider exploring the following resources: - National Association of Realtors - First-Time Homebuyer Guide - HUD.gov - Buying a Home