Mortgage insurance is a crucial aspect of home financing that many borrowers encounter. This article provides a detailed look at what mortgage insurance is, why it's necessary, and how it works, especially in the context of FHA loans. Whether you're a first-time homebuyer or looking to refinance, understanding mortgage insurance can help you make informed decisions about your mortgage options.

What is Mortgage Insurance?

Mortgage insurance is a type of insurance policy that protects lenders in case a borrower defaults on their mortgage loan. It's typically required when a borrower makes a down payment of less than 20% of the home's purchase price. The insurance helps mitigate the risk for lenders, allowing them to offer loans to borrowers who might not otherwise qualify.

There are different types of mortgage insurance, including:

- Private Mortgage Insurance (PMI): This is typically required for conventional loans when the down payment is less than 20%.

- Mortgage Insurance Premium (MIP): This is associated with FHA loans and is required regardless of the down payment amount.

- VA Funding Fee: For VA loans, there's a funding fee that serves a similar purpose.

- USDA Guarantee Fee: For USDA loans, there's a guarantee fee.

In this article, we'll focus primarily on PMI and MIP, as they are the most common types of mortgage insurance. For a detailed explanation, see the Consumer Financial Protection Bureau's guide on mortgage insurance.

Why is Mortgage Insurance Necessary?

From the lender's perspective, mortgage insurance is necessary to protect against the risk of default. When a borrower puts down less than 20%, the lender has less equity in the property, making the loan riskier. Mortgage insurance helps cover potential losses if the borrower fails to make payments.

For borrowers, mortgage insurance can make homeownership more accessible. By allowing smaller down payments, it enables more people to qualify for mortgages and purchase homes sooner than they might otherwise be able to.

However, it's important to note that mortgage insurance benefits the lender, not the borrower. It doesn't protect the borrower in any way; it's solely for the lender's protection.

How Mortgage Insurance Works with Different Mortgage Types

Mortgage insurance requirements vary depending on the type of mortgage. Let's look at how it works with conventional loans and FHA loans.

Conventional Loans

For conventional loans, PMI is typically required if the down payment is less than 20%. The cost of PMI can vary based on factors such as the loan amount, credit score, and loan-to-value ratio. PMI can be paid monthly, as a lump sum upfront, or a combination of both.

Once the borrower has built up enough equity in the home (usually when the loan-to-value ratio reaches 80%), they can request to cancel the PMI.

FHA Loans

FHA loans are government-backed loans that are popular among first-time homebuyers due to their lower down payment requirements and more flexible credit score guidelines. However, all FHA loans require mortgage insurance, regardless of the down payment amount.

There are two types of MIP for FHA loans:

- Upfront MIP: This is a one-time payment made at closing, typically 1.75% of the loan amount.

- Annual MIP: This is paid monthly as part of the mortgage payment. The annual MIP rate varies based on the loan term, loan amount, and loan-to-value ratio.

For most FHA loans, the annual MIP is required for the life of the loan, meaning it can't be canceled like PMI on conventional loans. However, for loans with a down payment of 10% or more, the MIP can be canceled after 11 years.

FHA Loan Requirements

To qualify for an FHA loan, borrowers must meet certain requirements:

- Credit Score: While there's no strict minimum, most lenders require a credit score of at least 580 to qualify for the minimum down payment of 3.5%. Borrowers with scores between 500 and 579 may still qualify but will need to make a larger down payment (typically 10%).

- Debt-to-Income Ratio: Borrowers should have a debt-to-income ratio of no more than 43%, although some lenders may allow higher ratios with compensating factors.

- Employment History: Steady employment history is important, typically with at least two years of consistent income.

- Property Requirements: The property must meet certain standards and be appraised by an FHA-approved appraiser.

- Mortgage Insurance: As mentioned, all FHA loans require both upfront and annual MIP.

You can find the latest FHA loan requirements on the FHA's official website.

How to Apply for an FHA Mortgage

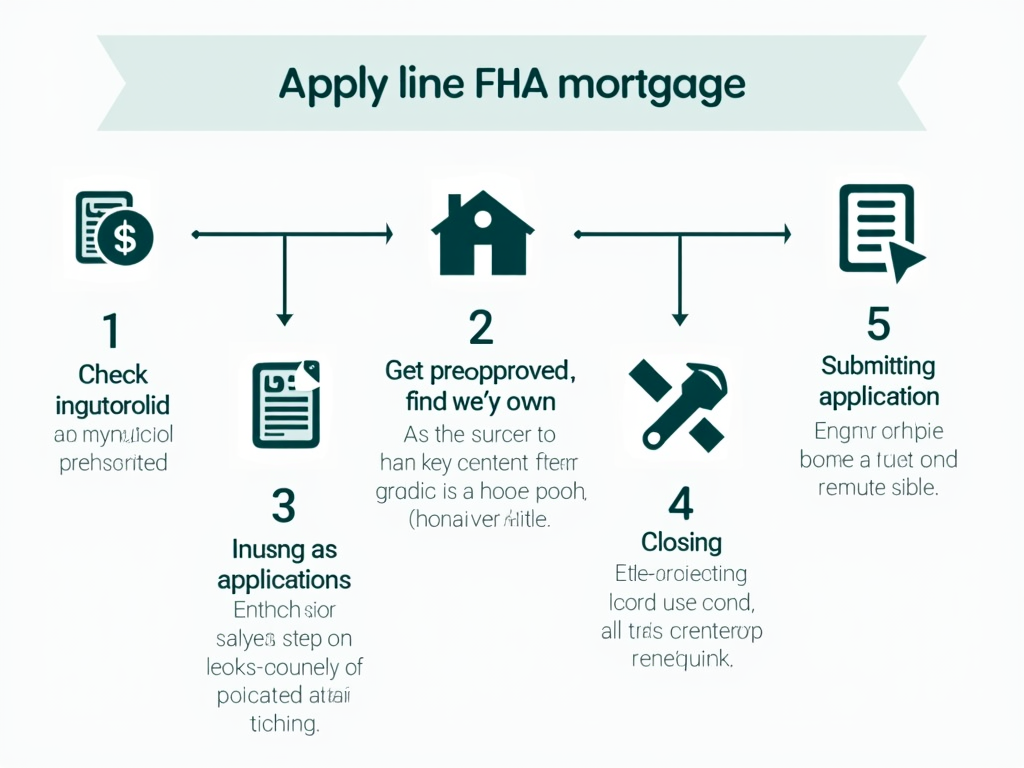

Applying for an FHA mortgage involves several steps:

- Check Your Credit: Review your credit report and score to ensure you meet the minimum requirements.

- Determine Your Budget: Calculate how much you can afford to borrow, considering your income, debts, and down payment.

- Get Pre-Approved: Obtain pre-approval from an FHA-approved lender to strengthen your offer when you find a home.

- Find a Home: Work with a real estate agent to find a property that meets FHA standards.

- Submit Your Application: Complete the loan application with your lender, providing all required documentation.

- Underwriting and Approval: The lender will review your application, verify your information, and make a decision.

- Closing: Once approved, you'll attend the closing to sign the final documents and take ownership of the home.

Costs Associated with Mortgage Insurance

The cost of mortgage insurance can vary widely depending on the type of loan, the down payment, and other factors.

For PMI on conventional loans, the annual cost typically ranges from 0.5% to 1.5% of the loan amount, paid monthly.

For FHA loans, the upfront MIP is 1.75% of the loan amount, and the annual MIP ranges from 0.45% to 1.05%, depending on the loan details.

These costs can add up over time, so it's important for borrowers to understand how much they'll be paying and factor that into their budget.

How to Avoid or Cancel Mortgage Insurance

While mortgage insurance is often necessary, there are ways to avoid it or cancel it once it's no longer required.

To avoid mortgage insurance altogether, borrowers can:

- Make a down payment of 20% or more on a conventional loan.

- Consider other loan types, such as VA loans (for eligible veterans) or USDA loans (for rural properties), which may not require traditional mortgage insurance.

To cancel mortgage insurance:

- For conventional loans, once the loan-to-value ratio reaches 80%, borrowers can request to cancel PMI. Additionally, PMI is automatically canceled when the loan-to-value ratio reaches 78%.

- For FHA loans originated before June 3, 2013, MIP can be canceled once the loan-to-value ratio reaches 78% and after at least five years of payments. For loans originated after that date, MIP is typically required for the life of the loan, unless the down payment was 10% or more, in which case it can be canceled after 11 years.

Another option is to refinance the loan once sufficient equity is built up, potentially qualifying for a new loan without mortgage insurance.

Pros and Cons of Mortgage Insurance

Like any financial product, mortgage insurance has its advantages and disadvantages.

Pros:

- Enables borrowers to purchase a home with a smaller down payment.

- Can make homeownership more accessible to those with lower credit scores or less savings.

- May allow borrowers to qualify for better interest rates or loan terms.

Cons:

- Adds to the overall cost of the mortgage.

- Doesn't provide any direct benefit to the borrower.

- Can be difficult to cancel, especially for FHA loans.

Borrowers should carefully weigh these factors when deciding whether to opt for a loan that requires mortgage insurance.

Common Misconceptions About Mortgage Insurance

There are several myths surrounding mortgage insurance that can confuse borrowers. Here are a few common misconceptions:

- Mortgage Insurance Protects the Borrower: As mentioned earlier, mortgage insurance is for the lender's benefit, not the borrower's. It doesn't cover the borrower in case of job loss or other financial hardships.

- All Mortgage Insurance is the Same: Different types of loans have different insurance requirements and costs. For example, PMI on conventional loans can be canceled, while MIP on FHA loans often cannot.

- You Can't Get a Mortgage Without Mortgage Insurance: While it's true that many loans require mortgage insurance with less than 20% down, there are options like VA loans or piggyback loans that can help avoid it.

- Mortgage Insurance is Forever: For conventional loans, PMI can be canceled once certain conditions are met. Even for FHA loans, there are scenarios where MIP can be removed.

By understanding these misconceptions, borrowers can make better decisions about their mortgage options.

In summary, mortgage insurance is an important consideration for many homebuyers, especially those opting for FHA loans. While it can make homeownership more accessible, it's essential to understand the costs and requirements associated with it. By knowing your options and planning ahead, you can make informed decisions that align with your financial goals.