Overview

An adjustable-rate mortgage (ARM) is a home loan where the interest rate can change over time based on market conditions. This can offer lower initial rates compared to fixed-rate mortgages but also carries the risk of rates increasing in the future.

What is an Adjustable-Rate Mortgage?

An adjustable-rate mortgage, or ARM, is a type of mortgage where the interest rate is not fixed for the entire term of the loan. Instead, it starts with an initial fixed-rate period, after which the rate adjusts periodically based on a specified index plus a margin. For example, a 5/1 ARM has a fixed rate for the first five years and then adjusts every year thereafter.

According to the Consumer Financial Protection Bureau, ARMs can be complex, and it's important to understand how they work before choosing one.

How Does an ARM Work?

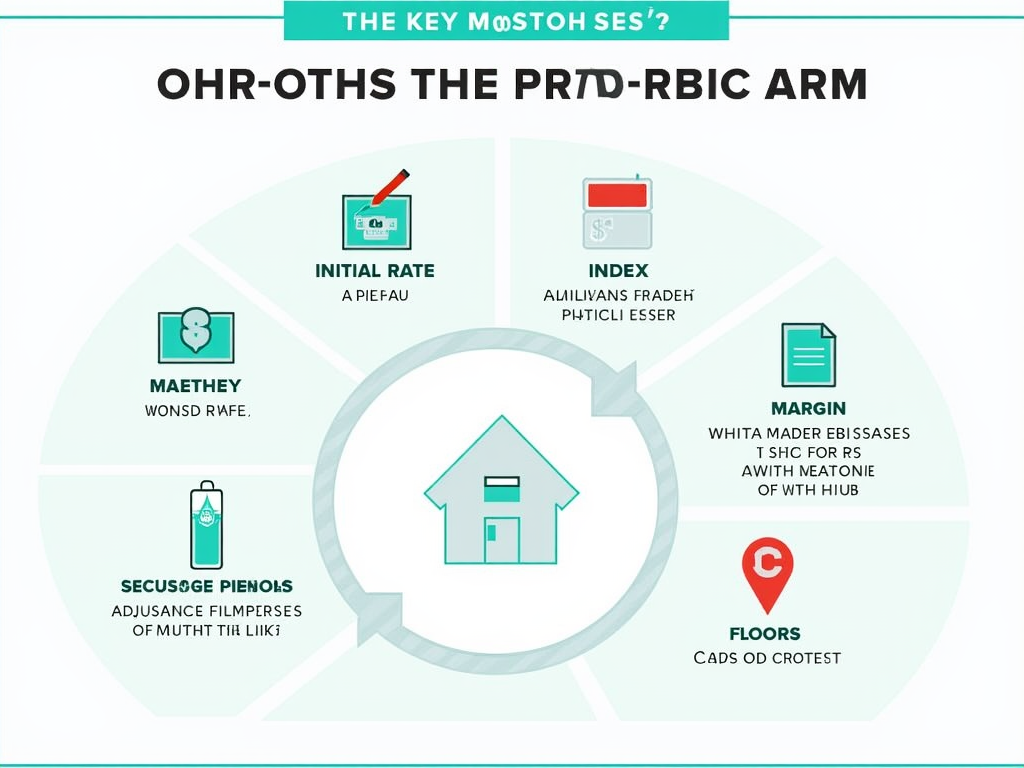

To understand how an ARM works, you need to know its key components:

- Initial Rate: The interest rate at the start of the loan, which is fixed for a certain period.

- Adjustment Period: How often the rate adjusts after the initial period.

- Index: A benchmark interest rate that the ARM's rate is tied to, such as the LIBOR or Treasury index.

- Margin: A fixed percentage added to the index to determine the new interest rate.

- Caps: Limits on how much the interest rate can increase or decrease at each adjustment and over the life of the loan.

- Floors: The minimum interest rate the loan can have.

When the adjustment period arrives, the new interest rate is calculated by adding the margin to the current index value, subject to the caps and floors.

For current information on mortgage rates and indices, you can refer to Freddie Mac's Primary Mortgage Market Survey.

Benefits of an ARM

- Lower Initial Rates: ARMs often have lower starting rates than fixed-rate mortgages, making them more affordable initially.

- Potential for Rate Decreases: If market rates fall, your interest rate could decrease, lowering your payments.

- Flexibility: ARMs can be beneficial if you plan to sell or refinance before the rate adjusts.

Risks of an ARM

- Rate Increases: If market rates rise, your interest rate and monthly payments could increase significantly.

- Uncertainty: Future payments are unpredictable, which can make budgeting challenging.

- Complexity: ARMs are more complicated than fixed-rate mortgages, requiring careful consideration of terms.

Who Should Consider an ARM?

ARMs might be suitable for:

- Borrowers who plan to move or refinance within the initial fixed-rate period.

- Those expecting their income to increase, allowing them to handle potential payment increases.

- Borrowers who believe interest rates will remain stable or decrease.

However, they may not be ideal for those who prefer payment stability or plan to stay in their home long-term.

Example Scenario

Suppose you take out a 5/1 ARM with an initial rate of 3.5%, a margin of 2%, and caps of 2% per adjustment and 5% lifetime. If the index is 4% at the first adjustment, your new rate would be 6% (4% index + 2% margin). However, with a 2% cap, if your initial rate was 3.5%, the maximum rate at the first adjustment would be 5.5%.

This example shows how caps can protect you from sharp rate increases.

Personal Insight

As a financial advisor, I've seen clients benefit from ARMs when they align with their plans. For instance, a client who knew they would relocate in a few years chose a 7/1 ARM to take advantage of the lower initial rate. However, it's crucial to have a contingency plan in case circumstances change.

Comparing ARMs to Fixed-Rate Mortgages

Fixed-rate mortgages offer stability with unchanging interest rates and payments throughout the loan term. In contrast, ARMs provide lower initial rates but with the potential for future increases. The choice depends on your financial goals, risk tolerance, and how long you plan to stay in the home.

Mortgage Terms for Different Loan Types

The mortgage term is the length of time you have to repay the loan, typically 15, 20, or 30 years. For ARMs, the term includes both the initial fixed period and the adjustable period. For example, a 30-year 5/1 ARM has a 30-year term with the first five years at a fixed rate and the remaining 25 years with adjustable rates.

Understanding Mortgage Terms

Key mortgage terms include:

- Principal: The amount borrowed.

- Interest: The cost of borrowing.

- Amortization: The process of paying off the loan through regular payments.

- Escrow: An account for property taxes and insurance.

For more on mortgage basics, see the University of Illinois Extension's mortgage resources.

Summary

Adjustable-rate mortgages can be a valuable tool for certain borrowers, offering lower initial rates and flexibility. However, they come with risks, including potential rate increases and payment uncertainty. By understanding how ARMs work and carefully considering your financial situation, you can make an informed decision about whether an ARM is right for you.