Buying a home ranks among life's biggest steps. Getting a mortgage plays a central role in making that dream real. One key part often surprises first-time buyers: the home appraisal. This independent check ensures the property's worth matches the loan amount. It protects everyone involved. In this guide, we explore the role of home appraisals in the mortgage process and why it matters so much.

What Is a Home Appraisal?

A home appraisal gives an unbiased estimate of a property's market value. A licensed appraiser visits the home, checks its condition, size, features, and location. They compare it to similar recent sales, known as comparables or 'comps.'

Unlike a home inspection that looks for problems, an appraisal focuses purely on value. Lenders rely on this number to decide how much money they can safely lend.

Why Appraisals Matter in the Mortgage Process

Mortgage lenders want protection. The home serves as collateral. If you can't repay the loan, the lender sells the property to recover funds.

If the appraisal shows the home worth less than the loan, the lender faces risk. That's why almost every conventional mortgage requires an appraisal. It keeps the loan-to-value ratio (LTV) safe. A strong appraisal can even lead to better loan terms in some cases.

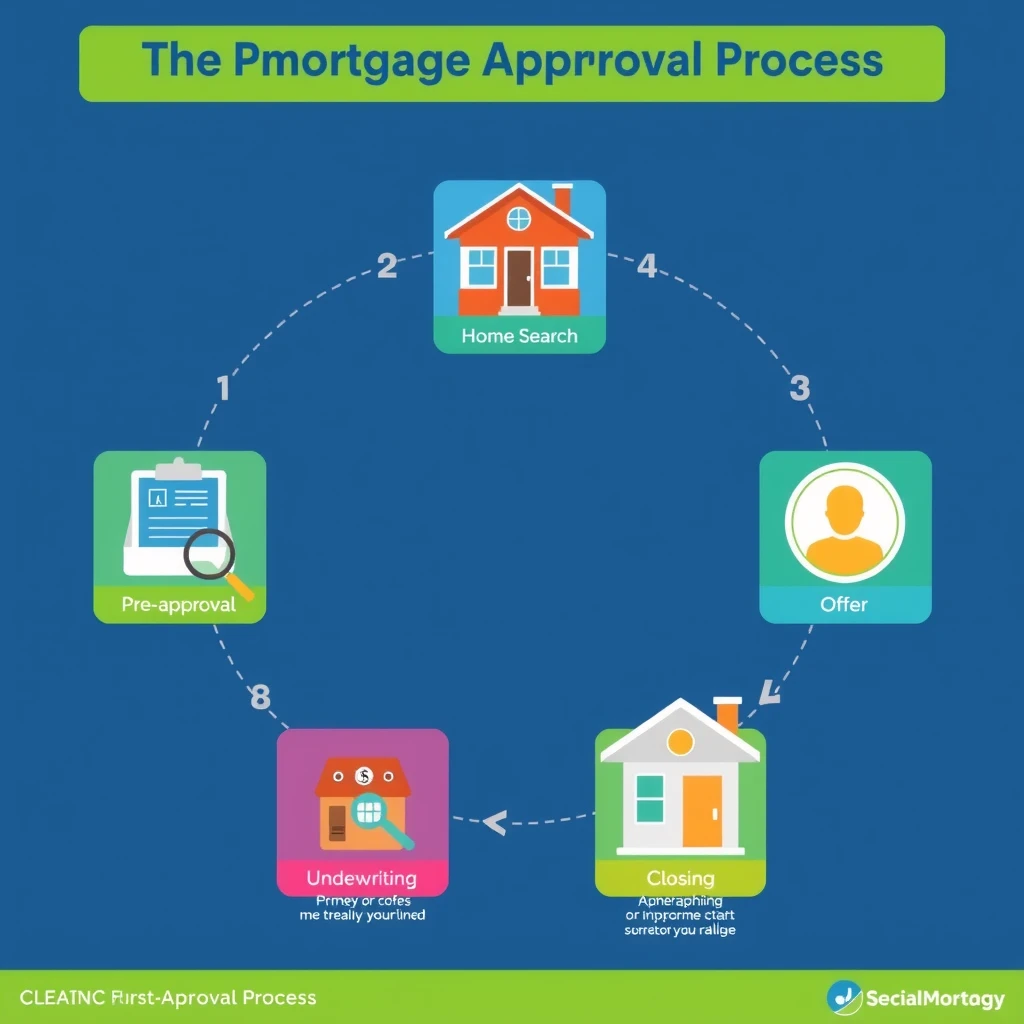

The Mortgage Application Process Step by Step

Understanding where the appraisal fits helps reduce stress. Here's a clear breakdown:

- Pre-approval — You submit financial info to a mortgage lender for a pre-approval letter.

- Find a home — You shop and make an offer.

- Offer accepted — Both parties sign the purchase agreement.

- Loan application — You formally apply with your mortgage lender.

- Appraisal ordered — The lender selects an independent appraiser (you usually pay $300–$600).

- Appraiser visits — They inspect inside and out, take photos, and note details.

- Report completed — The appraiser delivers a report with the value estimate.

- Underwriting — The lender reviews everything, including the appraisal.

- Closing — If approved, you sign papers and get the keys!

This step-by-step flow shows the appraisal as a critical checkpoint after your offer gets accepted but before final approval.

What Happens During the Appraisal Visit?

The visit usually lasts 30–60 minutes. The appraiser checks:

- Square footage

- Number of bedrooms and bathrooms

- Overall condition

- Upgrades like new kitchen or roof

- Exterior features (yard, garage)

- Neighborhood factors

They snap photos and leave. No need to follow them around or point things out — they know what to look for. Clean and tidy helps, but don't stress over perfection.

What If the Appraisal Comes in Low?

A low appraisal happens in about 10–20% of cases. When it does, options include:

- Negotiate with the seller — Ask them to lower the price to match the appraisal.

- Pay the difference — Bring extra cash to cover the gap (on top of your down payment).

- Challenge the appraisal — Provide evidence of errors or missed comps to the lender for review.

- Walk away — If you have an appraisal contingency, exit without losing your deposit.

In my experience helping friends through buys, negotiation works most often when sellers really want to close.

Tips to Prepare for a Smooth Appraisal

As a buyer, you have little control, but sellers can help:

- Fix obvious issues (leaky faucets, broken windows)

- Make minor cosmetic updates

- Provide receipts for recent improvements

- Ensure easy access to all areas

Buyers: Share any special features with your lender early. A well-prepared home often appraises at or above expectations.

Final Thoughts

The home appraisal serves as a safety net in the mortgage process. It confirms fair value, protects your investment, and gives lenders confidence. While it can feel like one more hurdle, it often saves buyers from overpaying and helps everyone move forward with clarity.

Approach it as a helpful step, not a scary one. With good preparation and realistic expectations, most appraisals go smoothly and lead to happy closings.