Your credit score can shape your financial life. A higher score means better loan terms and more opportunities. This guide explains how to improve your credit score with clear, actionable steps. Let’s dive into what it takes to build a stronger financial foundation.

What Is a Credit Score?

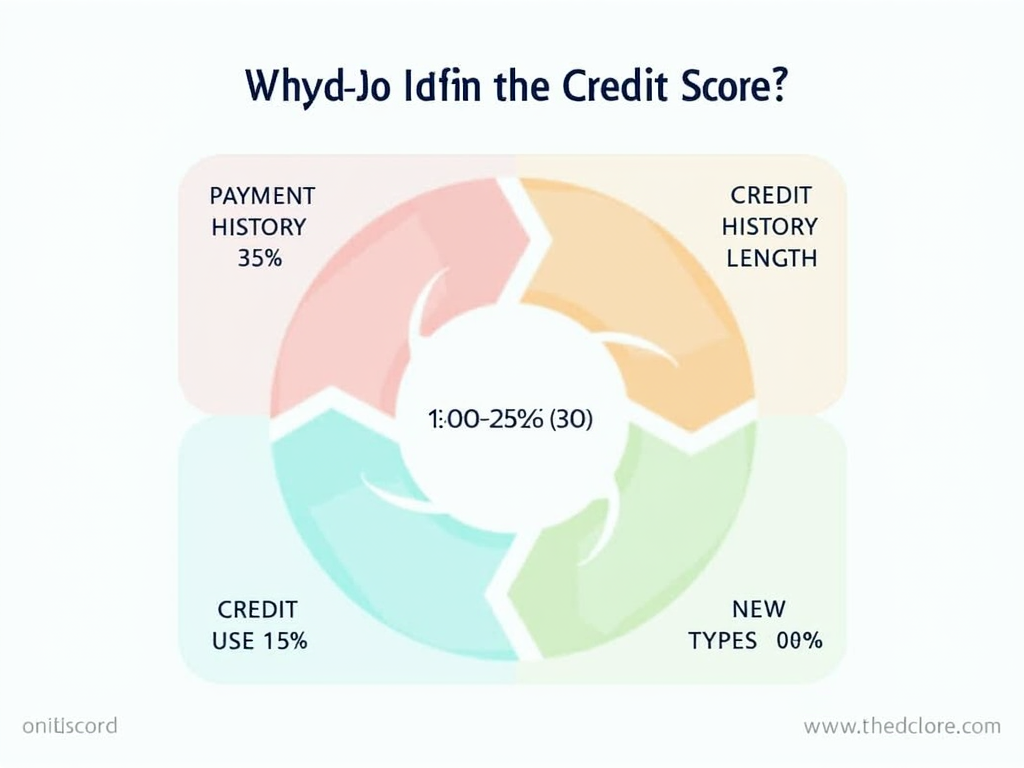

Your credit score is a number that shows how well you handle money. It’s based on your past with loans, credit cards, and bill payments. Lenders look at it to decide if they’ll give you money and at what rate.

Payment history tracks if you pay bills on time. Credit use compares your debt to your credit limits. History length counts how long you’ve had credit. Credit types look at variety, like cards or loans. New credit checks recent applications.

Why Does Your Credit Score Matter?

A good score can save you thousands. For example, it can lower your interest rate on a mortgage. It also helps with renting, jobs, or insurance. A low score? You’ll pay more or miss out.

How to Check Your Credit Score

You don’t need to guess your score. Many banks and credit card apps show it for free. You can also visit AnnualCreditReport.com for a free report from all three credit bureaus—Equifax, Experian, and TransUnion—once a year.

Checking your report helps you spot mistakes. I once found an old bill marked unpaid that I’d settled. Fixing it bumped my score up 20 points. It’s worth the effort.

5 Key Steps to Improve Your Credit Score

Boosting your score isn’t magic—it’s about habits. Here’s what works:

- Pay Bills on Time: Late payments hurt most. Set reminders or auto-pay.

- Lower Your Debt: Pay off credit cards. Keep balances under 30% of your limit.

- Keep Old Cards Open: Older accounts boost your history length.

- Limit New Credit: Too many applications look risky. Apply only when needed.

- Mix Your Credit: A blend of cards and loans can help, if managed well.

I learned this the hard way. Years ago, I closed an old card thinking it’d simplify things. My score dropped because my credit history shrank. Now, I keep them open and unused.

Tools to Help You

Apps like Credit Karma or Mint track your score and suggest moves. They’re free and easy. Your bank might offer tools too. Use them to stay on top of changes.

Mistakes That Hurt Your Score

Avoid these traps:

- Closing Old Accounts: It shortens your history.

- Applying Everywhere: Each hit dings your score a little.

- Skipping Report Checks: Errors slip through. Fix them fast.

How Long Does It Take?

Improvement isn’t instant. Small changes, like paying on time, show up in a month. Big fixes, like clearing debt, take six months or more. Patience pays off—I saw my score climb 80 points in a year.

A Real Example

When I started, my score was 620. I couldn’t qualify for a decent mortgage. I paid off two cards, disputed an error, and waited. A year later, at 700, I got a great rate. It felt like a win.

Credit Scores and Home Buying

A solid score ties into big goals, like buying a home. Curious about mortgages? How to Choose the Right Mortgage for You can guide your options. The Step-by-Step Home Buying Guide breaks it down further.

If you’re eyeing an FHA loan, your score matters less—580 can work. The FHA Loan Application Process is straightforward but needs prep. Start with your score now to ease that FHA loan application later.

Quick Tips Table

Here’s a snapshot of what helps:

| Action | Impact |

|---|---|

| Pay on Time | High (+50) |

| Reduce Debt | Medium (+30) |

| Keep Accounts Open | Low (+20) |

| Limit Applications | Low (+10) |

Start with the big wins.

When to Get Help

If it’s overwhelming, credit counselors can step in. Look for nonprofits via NFCC.org. They’ve helped friends of mine untangle messes without judgment.

Summary

Improving your credit score takes effort, but it’s worth it. Pay on time, cut debt, and check your report. Over time, you’ll unlock better rates and options. Start today—your future self will thank you.