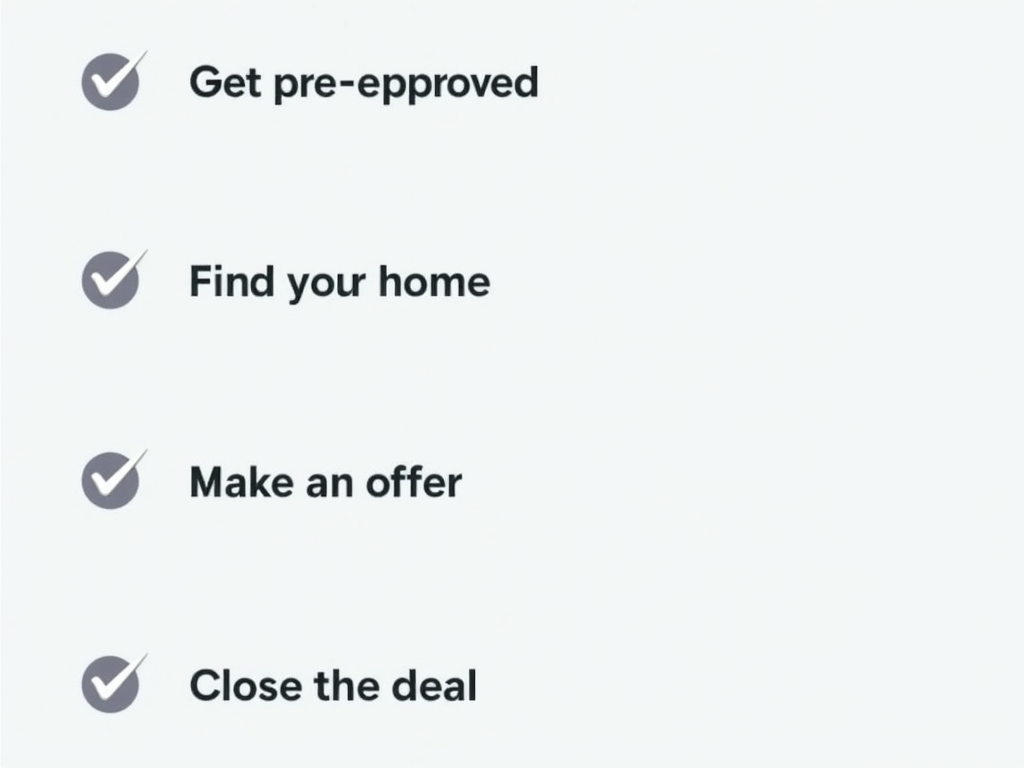

Buying a home is a significant milestone, but the process can be overwhelming. This guide breaks down the homebuying journey into manageable steps, providing expert advice and practical tips to help you navigate the process with confidence. From assessing your financial readiness to closing the deal, we'll cover everything you need to know to turn your dream of homeownership into a reality.

Step 1: Assessing Your Financial Readiness

Before you start house hunting, it's crucial to evaluate your financial situation. This step involves budgeting, checking your credit score, and saving for a down payment. A solid financial foundation will not only make you a more attractive buyer but also ensure that you can comfortably afford your new home.

- Budgeting: Determine how much you can afford to spend on a home by considering your income, expenses, and future financial goals.

- Credit Score: Your credit score plays a significant role in securing a mortgage. Aim for a score of at least 620 for Conventional loans and 580 for FHA loans.

- Down Payment: While Conventional loans typically require a 20% down payment, FHA loans offer options as low as 3.5%.

| Feature | Conventional Loan | FHA Loan |

|---|---|---|

| Down Payment | 20% | 3.5% |

| Credit Score | 620+ | 580+ |

| Mortgage Insurance | Required if down payment <20% | Required |

Step 2: Choosing the Right Loan

Selecting the right loan is a critical step in the homebuying process. Conventional and FHA loans are two popular options, each with its own set of benefits and requirements.

- Conventional Loans: These loans are not insured by the government and typically require a higher credit score and down payment. However, they offer more flexibility in terms of property types and loan terms.

- FHA Loans: Backed by the Federal Housing Administration, FHA loans are designed for first-time homebuyers and those with lower credit scores. They require a smaller down payment but come with mortgage insurance premiums.

When choosing between Conventional and FHA loans, consider your financial situation, credit score, and long-term goals. Consulting with a mortgage lender can help you determine the best option for your needs.

Step 3: Finding Your Dream Home

Once you've secured financing, it's time to start searching for your dream home. Working with a real estate agent can streamline the process and provide valuable insights into the local market.

- Working with an Agent: A good agent will listen to your needs, provide expert advice, and negotiate on your behalf.

- Evaluating Properties: Consider factors such as location, size, condition, and potential for appreciation when assessing homes.

Factors to Consider When Evaluating Homes: - Location (proximity to work, schools, amenities) - Size and layout - Condition and age of the property - Potential for future value appreciation - Neighborhood safety and community vibe

Step 4: Making an Offer and Negotiating

When you find a home you love, it's time to make an offer. This step involves submitting a purchase agreement and negotiating terms with the seller.

- Making an Offer: Your offer should include the purchase price, contingencies, and closing date.

- Negotiating: Be prepared to negotiate on price, repairs, and other terms. Your agent can help you navigate this process.

Sharing a personal anecdote here: When I bought my first home, I was nervous about making an offer. My agent reassured me and helped me craft a competitive yet reasonable offer. After some back-and-forth, we reached an agreement that worked for both parties.

Step 5: Securing Financing and Closing the Deal

The final step in the homebuying process is securing financing and closing the deal. This involves obtaining mortgage pre-approval, completing inspections, and finalizing the paperwork.

- Mortgage Pre-Approval: Getting pre-approved for a mortgage shows sellers that you're a serious buyer and can afford the home.

- Closing Process: During closing, you'll sign the final paperwork, pay closing costs, and receive the keys to your new home.

Tips for a smooth closing: - Review all documents carefully. - Ask questions if anything is unclear. - Bring a cashier's check for closing costs.

Buying a home is a complex process, but with the right preparation and guidance, it can be a rewarding experience. Remember to assess your financial readiness, choose the right loan, find your dream home, make a strong offer, and navigate the closing process with confidence.