Applying for an FHA mortgage in 2024 involves several key steps, but the benefits, such as lower down payments and more flexible credit requirements, make it a popular choice for many homebuyers. This guide will walk you through the entire process, from understanding what an FHA loan is to closing on your new home.

Understanding FHA Loans and Their Benefits

An FHA loan is a mortgage insured by the Federal Housing Administration (FHA), designed to make homeownership more accessible, especially for first-time buyers. One of the biggest advantages is the low down payment requirement—as little as 3.5% for those with a credit score of 580 or higher. Additionally, FHA loans are more lenient with credit scores compared to conventional loans, making them a great option for those with less-than-perfect credit.

Another benefit is the ability to include closing costs in the loan, reducing upfront expenses. FHA loans also allow for higher debt-to-income ratios, meaning you can qualify even if you have existing debts. These features make FHA loans particularly attractive in 2024, as housing prices continue to rise.

FHA Loan Benefits at a Glance

- Low Down Payment: As little as 3.5% for qualified borrowers.

- Flexible Credit Requirements: Minimum credit score of 500, with most lenders preferring 580.

- Higher Debt-to-Income Tolerance: Up to 43% DTI ratio.

- Closing Costs Assistance: Option to roll closing costs into the loan.

- Assumable Loans: Future buyers can take over your loan, potentially making your home easier to sell.

Eligibility Requirements for an FHA Mortgage

Before applying, it's crucial to understand the eligibility criteria. While FHA loans are more accessible, there are still requirements you must meet:

-

Credit Score: The minimum credit score is 500, but to qualify for the 3.5% down payment, you'll need at least 580. If your score is between 500 and 579, you may still qualify but will need a 10% down payment.

-

Debt-to-Income Ratio (DTI): Your DTI should be below 43%. This means your monthly debt payments (including the mortgage) shouldn't exceed 43% of your gross monthly income. For example, if you earn $5,000 per month, your total debt payments should be less than $2,150.

-

Employment History: Lenders typically look for at least two years of steady employment. Gaps in employment can be explained, but consistency is key.

-

Down Payment: As mentioned, 3.5% for credit scores of 580+, and 10% for scores between 500-579. You can use gift funds or down payment assistance programs to cover this.

-

Property Requirements: The home must be your primary residence and meet certain safety and livability standards set by the FHA.

Meeting these requirements is the first step toward securing an FHA mortgage. If you're unsure about your eligibility, consider speaking with an FHA-approved lender who can assess your situation and provide guidance.

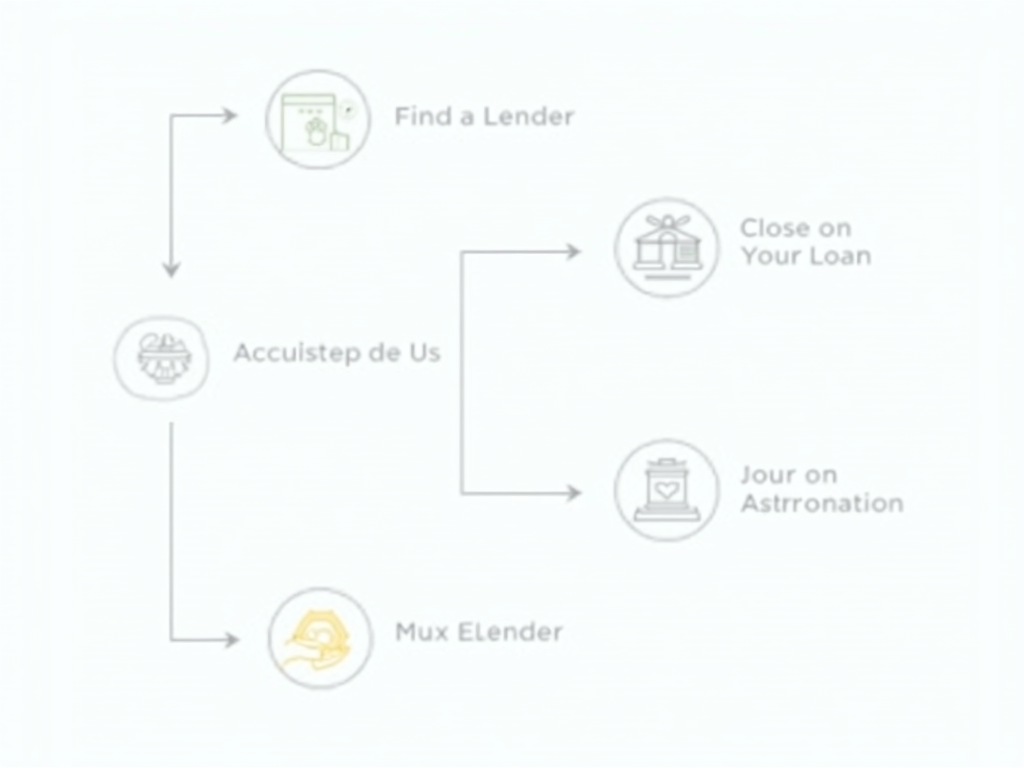

The Application Process: Step-by-Step

Once you've confirmed your eligibility, it's time to start the application process. Here's a detailed breakdown:

-

Find an FHA-Approved Lender: Not all lenders offer FHA loans, so make sure to choose one that is FHA-approved. You can search for lenders on the HUD website.

-

Get Pre-Approved: Pre-approval gives you an idea of how much you can borrow and shows sellers you're a serious buyer. You'll need to provide basic financial information, such as income, debts, and credit history.

-

Gather Documentation: Be prepared to submit documents like pay stubs, tax returns, bank statements, and identification. Having these ready can speed up the process.

-

Submit Your Application: Once you've found a home and made an offer, you'll complete the full loan application. Your lender will guide you through this step.

-

Underwriting Process: The lender will verify your information and assess the property to ensure it meets FHA standards. This can take a few weeks.

-

Close on Your Loan: If approved, you'll attend the closing, sign the paperwork, and officially become a homeowner.

Throughout this process, communication with your lender is key. Don't hesitate to ask questions or seek clarification on any part of the application.

Tips for a Successful FHA Mortgage Application

To increase your chances of approval and make the process smoother, consider these tips:

- Improve Your Credit Score: Pay down debts and avoid new credit inquiries before applying.

- Save for a Larger Down Payment: While 3.5% is the minimum, a larger down payment can reduce your monthly payments and show lenders you're financially responsible.

- Shop Around for Lenders: Different lenders may offer varying rates and fees, so compare options to find the best deal.

- Get Pre-Approved Early: This can give you a competitive edge in a hot housing market.

- Be Transparent: Disclose all financial information honestly to avoid delays or denials.

Remember, the FHA loan process is designed to be accessible, but preparation is still essential. By following these tips, you can navigate the application with confidence.

Summary

Applying for an FHA mortgage in 2024 is a straightforward process that offers numerous benefits, especially for first-time homebuyers. With lower down payment requirements, flexible credit guidelines, and the ability to finance closing costs, FHA loans make homeownership more attainable. By understanding the eligibility requirements, preparing your documentation, and working with an FHA-approved lender, you can successfully navigate the application process and achieve your dream of owning a home.