Navigating the mortgage application process can be daunting, especially for first-time homebuyers. This guide breaks down what to expect, from initial steps to closing, and offers tips to make the journey smoother.

Preparing for the Application

Before you even start looking at homes, it's crucial to get your financial house in order. This means understanding your current financial situation, checking your credit score, and saving for the down payment and closing costs.

Understanding Your Financial Situation Take a close look at your income, expenses, and debts. Lenders will want to see that you have a stable income and can manage your debts responsibly. Calculate your debt-to-income ratio (DTI), which is your monthly debt payments divided by your gross monthly income. A lower DTI is better, as it shows you have more room in your budget for a mortgage payment.

Checking Your Credit Score Your credit score plays a significant role in determining your mortgage eligibility and interest rate. Obtain a free credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) and check for any errors or areas for improvement. If your score is lower than you'd like, take steps to improve it, such as paying down debts or correcting inaccuracies.

Saving for Down Payment and Closing Costs While some loans allow for low down payments, having a larger down payment can reduce your monthly payments and possibly eliminate the need for private mortgage insurance (PMI). Additionally, closing costs can range from 2% to 5% of the loan amount, so it's wise to save for these expenses in advance.

Choosing the Right Mortgage

With your finances in order, it's time to explore your mortgage options. There are several types of mortgages, each with its own benefits and drawbacks.

Types of Mortgages - Fixed-Rate Mortgage: Offers a stable interest rate and predictable monthly payments for the life of the loan. - Adjustable-Rate Mortgage (ARM): Starts with a lower interest rate that can change over time, potentially leading to higher payments. - FHA Loan: Backed by the Federal Housing Administration, these loans often have lower down payment requirements and are suitable for first-time buyers. - VA Loan: Available to veterans and active-duty military personnel, offering competitive rates and no down payment options.

Comparing Lenders and Rates Don't settle for the first lender you come across. Shop around and compare interest rates, fees, and customer service. Consider getting pre-approved by multiple lenders to see who offers the best terms. Remember, even a small difference in interest rates can save you thousands over the life of the loan.

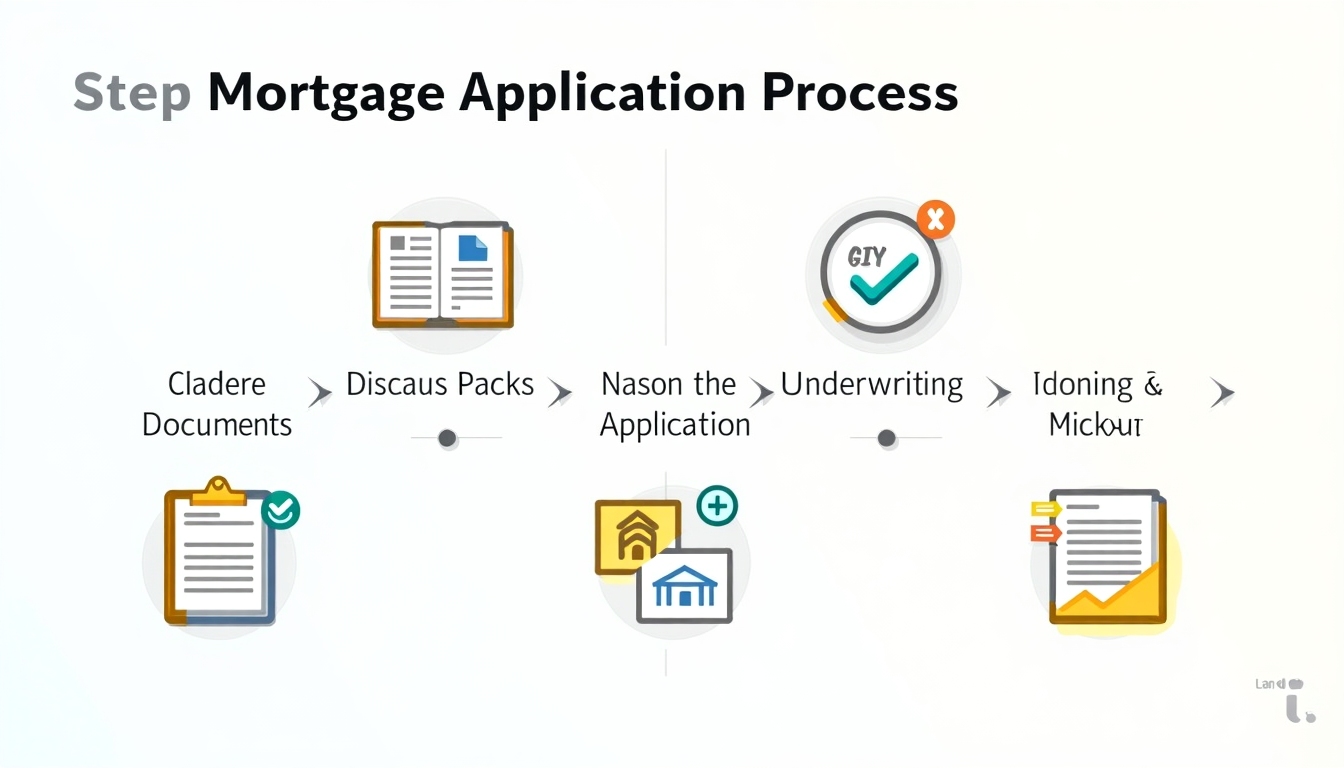

The Application Process

Once you've chosen a lender, it's time to start the application. This involves gathering necessary documents, filling out the application form, and understanding the associated fees.

Gathering Necessary Documents Lenders will require various documents to verify your financial information, including: - Proof of income (pay stubs, tax returns) - Employment verification - Bank statements - Identification (driver's license, Social Security number) - Credit report

Filling Out the Application The mortgage application form, also known as the Uniform Residential Loan Application, asks for detailed information about your finances, employment, and the property you wish to purchase. Be thorough and accurate to avoid delays.

Understanding Mortgage Application Fees Applying for a mortgage isn't free. You may encounter fees such as: - Application fee: Covers the cost of processing your application. - Appraisal fee: Pays for a professional appraisal of the property's value. - Credit report fee: Covers the cost of obtaining your credit report.

Ask your lender for a Loan Estimate, which outlines all the fees associated with your mortgage.

Underwriting and Approval

After submitting your application, it goes through underwriting, where the lender assesses your creditworthiness and the property's value.

What Happens During Underwriting The underwriter reviews your financial documents, credit history, and the appraisal report to determine if you qualify for the loan. This process can take anywhere from a few days to a few weeks.

Common Reasons for Delays or Denials - Incomplete or inaccurate information on the application - Insufficient income or high debt levels - Issues with the property appraisal - Changes in employment or credit status during the process

To avoid delays, respond promptly to any requests for additional information and avoid making large purchases or changing jobs during this time.

Closing the Loan

If your application is approved, you'll move to the closing stage, where you finalize the loan and take ownership of the property.

What to Expect at Closing At closing, you'll sign a stack of documents, including the promissory note, mortgage deed, and various disclosures. You'll also pay any remaining closing costs and the down payment.

Final Steps and Paperwork Before closing, review the Closing Disclosure, which details the final loan terms and costs. Make sure everything matches what you expected. After signing, the lender will fund the loan, and you'll receive the keys to your new home.

Applying for a mortgage is a significant step in homeownership. By understanding the process, preparing thoroughly, and seeking professional advice when needed, you can navigate it successfully. Remember, every journey starts with a single step—take yours today.