Overview

FHA loans help many buy homes with lower down payments and easier credit rules. But there’s a catch: FHA loan limits by county cap how much you can borrow. These limits change by area and affect your homebuying plans. Let’s break it down.

What Are FHA Loan Limits?

FHA loan limits by county are the maximum amounts the Federal Housing Administration (FHA) will back for a mortgage in a specific area. They’re tied to local home prices, so they differ across the U.S. The goal? Keep FHA loans focused on affordable homes.

In pricey places like Los Angeles, limits are higher. In rural spots, they’re lower. Knowing your county’s limit helps you shop smart.

How FHA Loan Limits Are Set

The FHA bases its limits on the national conforming loan limit, set by the Federal Housing Finance Agency. Here’s the breakdown:

- Floor Limit: Low-cost areas get 65% of the conforming limit—$472,030 for a single-family home in 2023.

- Ceiling Limit: High-cost areas can hit 150%, or $1,089,300 in places like New York.

Limits adjust yearly as home prices shift. Check the latest figures before you plan.

Finding FHA Loan Limits by County

Want to know your county’s limit? It’s easy. The U.S. Department of Housing and Urban Development (HUD) has a free online tool. Visit the HUD FHA Mortgage Limits page, pick your state and county, and see the numbers for one- to four-unit homes.

Your lender can also help. Knowing this upfront keeps your home search on track.

Tips for First-Time Homebuyers: Navigating FHA Mortgages

First-time buyers love FHA loans for their flexibility. Here’s how to make them work for you:

- Set a Budget: The loan limit isn’t your budget. Factor in your income and bills.

- Boost Your Credit: A 580 score gets you a 3.5% down payment. Below that, it’s 10%.

- Save Early: Even 3.5% takes time to gather. Start now.

- Find a Lender: A good one explains everything and speeds things up.

- Learn the Process: You’ll need pay stubs, tax returns, and more. Stay organized.

- Look for Help: Many states offer down payment aid. Ask your lender.

I once helped a friend buy her first home with an FHA loan. She didn’t realize her county’s limit capped her dream house—until we checked.

FHA Mortgage Closing Costs Breakdown

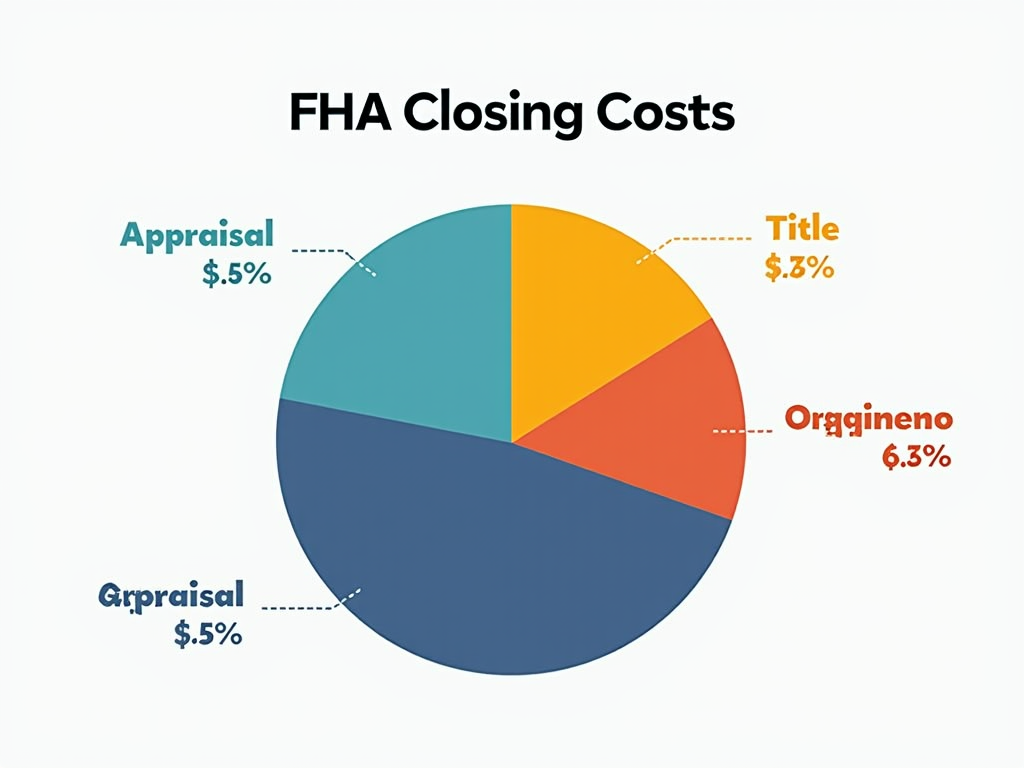

Closing costs hit at the end of your loan process. For an FHA mortgage, expect:

- Appraisal Fee: $300-$500 to value the home.

- Title Insurance: $500-$1,000 to protect ownership.

- Origination Fee: 1% of the loan for lender work.

- Prepaids: Taxes and insurance, often $1,000+.

Total costs? Usually 2%-5% of the home price. Sellers might cover some if you negotiate. Check the Consumer Financial Protection Bureau’s guide for details.

FHA Mortgage Guidelines

Qualifying for an FHA mortgage isn’t hard, but there are rules:

- Credit Score: 580+ for 3.5% down; 500-579 for 10%.

- Debt-to-Income: Keep debts under 43% of income.

- Down Payment: Starts at 3.5%.

- Mortgage Insurance: Pay upfront (1.75%) and monthly.

- Property Rules: Must be your main home and pass safety checks.

The FHA appraisal ensures the home’s safe—no broken roofs or bad wiring. See the FHA Handbook for more.

FHA Loan Limits and Refinancing

Already have an FHA loan? Refinancing depends on limits too. A streamline refinance sticks to your original loan amount. A standard refinance can go up to your county’s current limit—great if home values rose. Check your options.

Summary

FHA loan limits by county shape how much you can borrow with an FHA mortgage. They vary by area, so check your county’s cap. For first-time buyers, these loans open doors—but know the costs and rules. Research limits, talk to a lender, and plan ahead.