Overview

Learn how to calculate your FHA mortgage payments with this detailed guide. We’ll walk you through the steps, highlight what affects your payments, and share practical tips to manage your FHA loan with confidence.

What is an FHA Mortgage?

An FHA mortgage is a home loan backed by the Federal Housing Administration. It’s designed to help people, especially first-time buyers or those with lower credit scores, get into a home with easier terms than traditional loans.

Why Choose an FHA Loan?

FHA loans stand out because they require just a 3.5% down payment and are more forgiving on credit history. This makes them a go-to choice for many looking to buy a home without a big upfront cost.

Breaking Down FHA Mortgage Payments

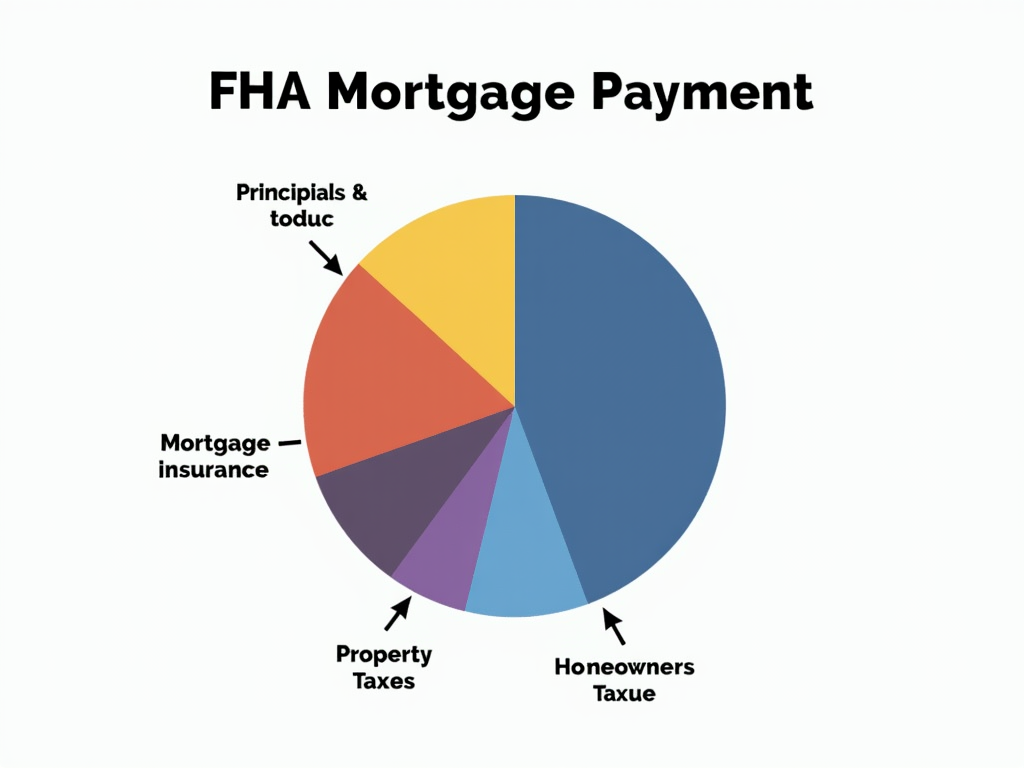

When calculating FHA mortgage payments, you’re looking at four main parts: principal and interest (P&I), mortgage insurance premium (MIP), property taxes, and homeowners insurance. Together, these make up what you pay each month.

Step 1: Calculating Principal and Interest (P&I)

The P&I is the amount you pay toward the loan itself and the interest the lender charges. You can calculate it using this formula:

Monthly Payment = Loan Amount × [Monthly Interest Rate × (1 + Monthly Interest Rate)^Number of Payments] / [(1 + Monthly Interest Rate)^Number of Payments - 1].

P&I Example

Say you borrow $200,000 at 4% interest for 30 years. The monthly interest rate is 0.003333 (4% ÷ 12), and there are 360 payments (30 × 12). Plugging in the numbers, your P&I comes out to about $954.83 per month.

Step 2: Mortgage Insurance Premium (MIP)

FHA loans require MIP to protect lenders if you can’t pay. There’s an upfront cost (usually 1.75% of the loan) and an annual fee (often 0.85%), split into monthly payments. For a $200,000 loan, that’s roughly $141.67 monthly.

Step 3: Property Taxes and Insurance

These depend on where you live and your home’s value. For example, if taxes are $2,400 a year and insurance is $1,200, that’s $200 and $100 per month, respectively. Your lender often collects these in an escrow account.

Step 4: Total Monthly Payment

Add it all up: $954.83 (P&I) + $141.67 (MIP) + $200 (taxes) + $100 (insurance) = $1,396.50. That’s your total monthly FHA mortgage payment for this example.

How Down Payment Affects Payments

With an FHA loan, the minimum down payment is 3.5%. Putting down more lowers your loan amount—and your monthly payment. For instance, a $10,000 down payment on a $210,000 home drops the loan to $200,000.

Interest Rates Matter

Even a small rate change can make a big difference. Here’s a quick look:

| Loan Amount | Rate | Term | Monthly P&I |

|-------------|------|------|-------------|

| $200,000 | 3.5% | 30 yrs | $898.09 |

| $200,000 | 4.0% | 30 yrs | $954.83 |

| $200,000 | 4.5% | 30 yrs | $1,013.37 |

The FHA Appraisal Factor

Every FHA loan needs an FHA appraisal to check the home’s value and condition. If the appraisal comes in lower than the sale price, you might need a bigger down payment, which tweaks your loan amount and payment.

A Real Story: Sarah’s Journey

Sarah, a teacher from Ohio, used an FHA loan for her first home. With a tight budget, the 3.5% down payment worked perfectly. She calculated her payments ahead of time and felt ready to take the leap.

Loan Limits to Know

FHA loans cap how much you can borrow, depending on your county. In 2023, limits range from $472,030 to $1,089,300 in high-cost areas (source: HUD.gov). If your home costs more, you’ll cover the difference.

Tips to Manage Your FHA Mortgage

- Pay a little extra toward the principal when you can—it cuts interest over time.

- Check your budget monthly to stay on track.

- Look into refinancing if rates drop; FHA offers streamlined options.

Why Calculating FHA Mortgage Payments Helps

Knowing your payment upfront lets you plan better. It’s not just numbers—it’s about making sure homeownership fits your life without stress.

Summary

Calculating FHA mortgage payments means adding up principal and interest, mortgage insurance, taxes, and insurance. By understanding these pieces and how things like down payments or rates play in, you’re set to handle your FHA loan like a pro.