Overview

FHA loans are a popular choice for first-time homebuyers because they require smaller down payments and are easier to qualify for than other loans. But there’s a catch: FHA loan limits cap how much you can borrow. These limits change depending on where you live and directly affect your buying power. In this article, we’ll break down what these limits are, how they work, and how they shape your homebuying options. Plus, we’ll share tips to get the most out of an FHA mortgage.

What Are FHA Loans?

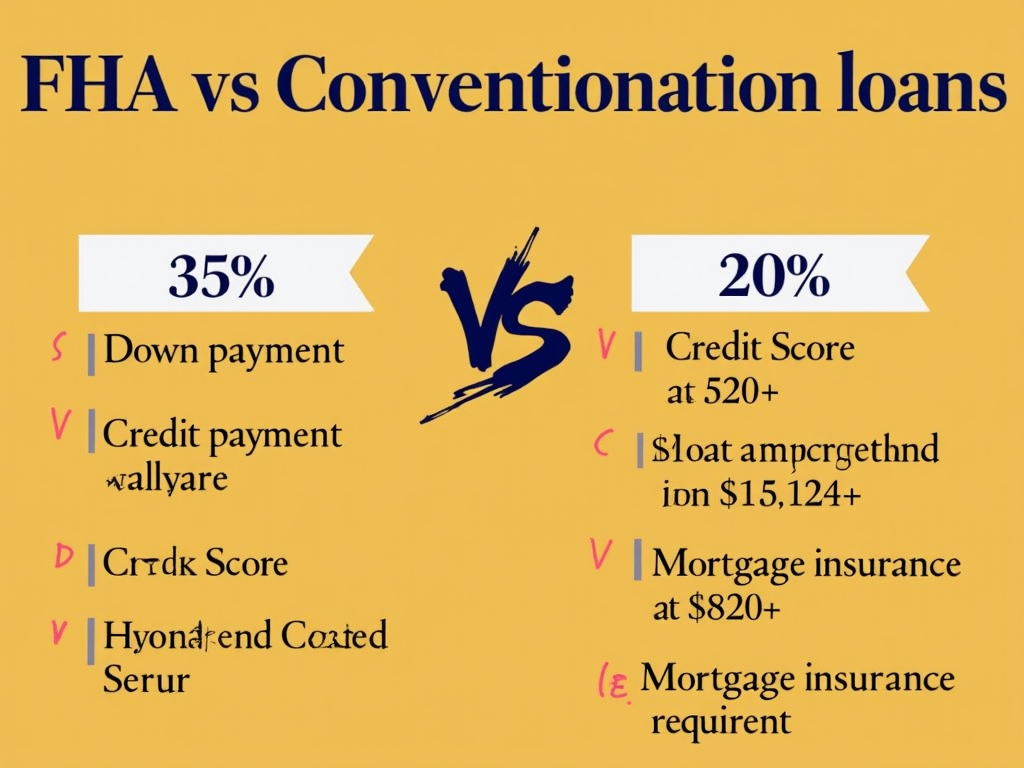

FHA loans are mortgages backed by the Federal Housing Administration (FHA), part of the U.S. government. They’re designed to help people who might not qualify for regular loans, like first-time buyers or those with lower credit scores. With an FHA mortgage, you can put down as little as 3.5% of the home’s price, compared to 20% for many traditional loans. You can also qualify with a credit score as low as 580.

The trade-off? You’ll pay mortgage insurance premiums to protect the lender if you can’t make payments. This makes FHA loans a lifeline for many, but the limits can change the game.

What Are FHA Loan Limits?

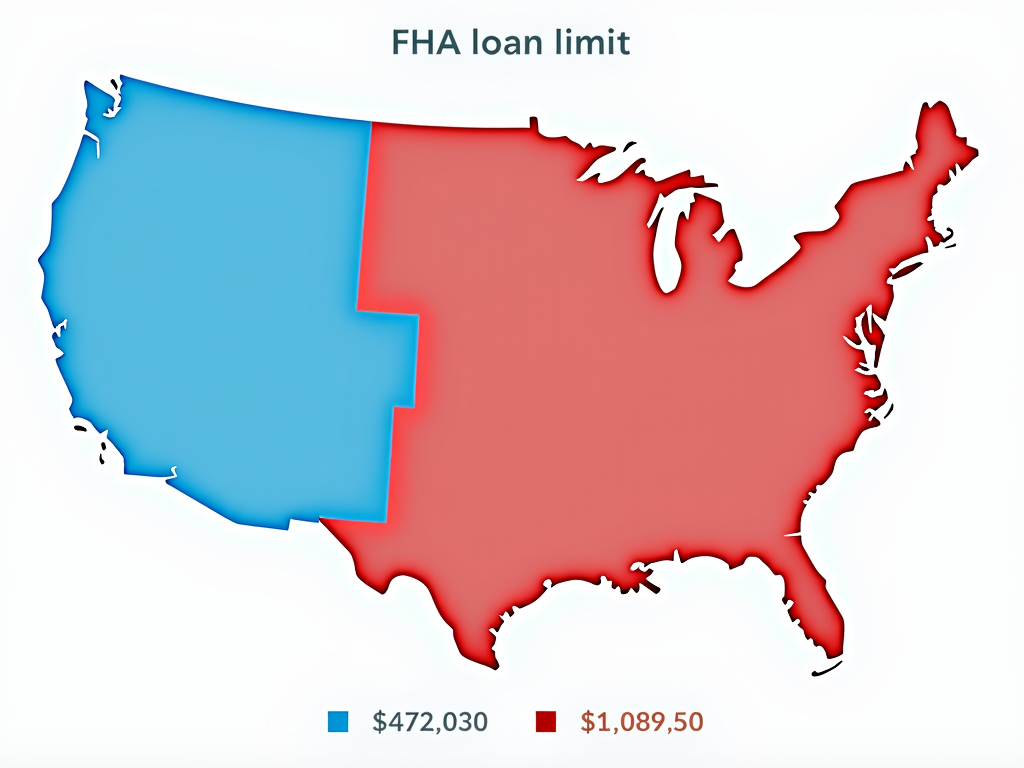

FHA loan limits are the maximum amount you can borrow with an FHA mortgage in your area. These limits aren’t the same everywhere—they depend on local home prices. In 2023, the basic limit for a single-family home is $472,030 in most places. But in expensive areas like San Francisco or New York, it jumps to $1,089,300.

Why does this matter? If a home costs more than the limit, you’ll need to cover the difference yourself or find another loan type. It’s a key part of understanding FHA loan limits and how they affect your buying power.

How Are FHA Loan Limits Determined?

The FHA sets these limits every year based on average home prices in each county. They take 115% of the median price, then cap it between a minimum (the 'floor') and a maximum (the 'ceiling'). For 2023, the floor is $472,030, and the ceiling is $1,089,300 in high-cost areas. Places like Alaska or Hawaii can go even higher, up to $1,633,950.

The FHA uses housing data to keep these limits in line with the market. That way, they stay fair no matter where you’re buying.

How Do FHA Loan Limits Affect Buying Power?

Your buying power is how much home you can afford, and FHA loan limits play a big role. The limit sets the max loan you can get, and your down payment adds to that. For example, with a $472,030 limit and a 3.5% down payment, you could buy a home up to $489,000.

But if homes in your area cost $600,000, you’d need an extra $128,000 upfront—or a different loan. Plus, FHA guidelines require the home to be your main residence and meet safety standards, which can narrow your options.

Here’s a quick example: - Limit: $500,000 - Down Payment: 5% ($26,316) - Max Home Price: $526,316 This shows how the limit shapes what you can buy.

Examples of FHA Loan Limits in Different Areas

Loan limits vary widely across the U.S. Here are some real examples for 2023: - Los Angeles County, CA: $1,089,300 - Cook County, IL (Chicago): $472,030 - Miami-Dade County, FL: $557,750 - King County, WA (Seattle): $1,089,300 - Denver County, CO: $856,750

Check your local limit on the HUD website to see what you’re working with. It’s a simple step that can save you time when house hunting.

Tips for Maximizing Buying Power With FHA Loans

You can stretch your FHA loan further with these ideas: 1. Save More Upfront: A 10% down payment beats 3.5%, letting you afford a pricier home. 2. Boost Your Credit: A better score means better rates and possibly a bigger loan. 3. Shop Smarter: Look in nearby areas with higher limits if your spot is too low. 4. Team Up: A co-borrower with good income can increase what you qualify for. 5. Negotiate: Ask sellers to lower the price—I once got a deal by offering a fast close!

These steps can make a big difference in what you bring home.

Common Misconceptions About FHA Loan Limits

People often get these wrong: - Myth: Limits are the same everywhere. - Truth: They change by location. - Myth: You can’t buy above the limit. - Truth: You can, with a bigger down payment. - Myth: FHA loans are just for newbies. - Truth: Anyone who qualifies can use them. - Myth: Limits never change. - Truth: They’re updated yearly.

Knowing the facts helps you plan better.

Conclusion

Understanding FHA loan limits is a must if you’re eyeing an FHA mortgage. They set the ceiling on what you can borrow, shaping your buying power and home choices. Get familiar with your area’s limit, and use smart strategies to maximize it. Talk to a lender who knows FHA guidelines—they’ll help you navigate the process and find the right fit.