Your credit score is a crucial factor in determining the interest rate you'll pay on your mortgage. In this article, we'll explore what credit scores are, how they're calculated, and how they impact mortgage rates. We'll also provide tips on how to improve your credit score to secure better loan terms.

What is a Credit Score?

A credit score is a numerical representation of your creditworthiness, based on your credit history. It's calculated using information from your credit reports, which are maintained by the three major credit bureaus: Equifax, Experian, and TransUnion. The most common credit score model is the FICO score, which ranges from 300 to 850.

How is a Credit Score Calculated?

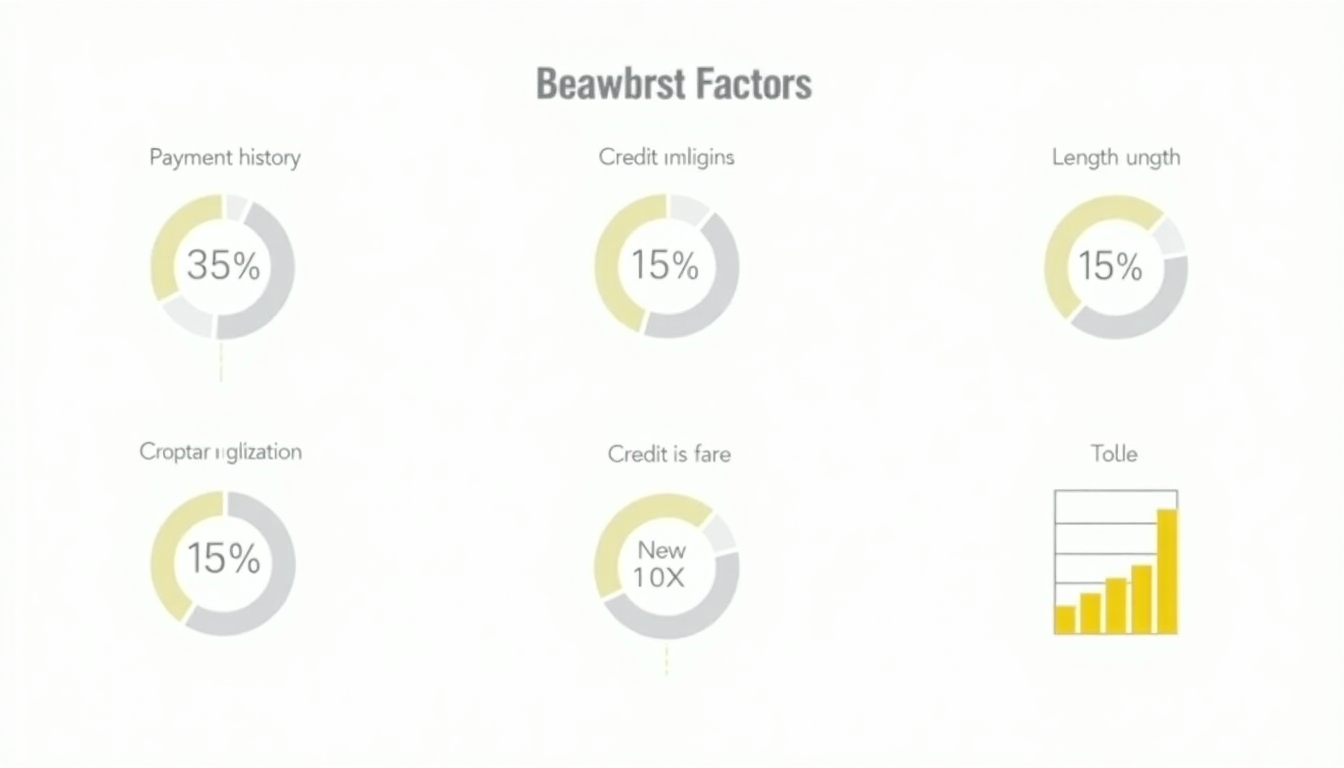

Your credit score is determined by several factors, including:

- Payment history (35%): This is the most significant factor and reflects whether you've paid your bills on time.

- Credit utilization (30%): This measures how much of your available credit you're using.

- Length of credit history (15%): A longer credit history generally leads to a higher score.

- Credit mix (10%): Having a variety of credit types, such as credit cards, installment loans, and mortgages, can positively impact your score.

- New credit (10%): Opening multiple new credit accounts in a short period can lower your score.

How Do Credit Scores Affect Mortgage Rates?

Lenders use credit scores to assess the risk of lending money to borrowers. A higher credit score indicates lower risk, which can lead to lower mortgage rates. Conversely, a lower credit score suggests higher risk, resulting in higher rates or even loan denial.

For example, let's say two individuals are applying for a 30-year fixed-rate mortgage of $300,000. Person A has a credit score of 760, while Person B has a score of 620. Person A might qualify for an interest rate of 3.5%, resulting in a monthly payment of $1,347. Person B, on the other hand, might be offered a rate of 5.5%, leading to a monthly payment of $1,703. Over the life of the loan, Person B would pay significantly more in interest.

Tips for Improving Your Credit Score

If your credit score isn't where you'd like it to be, there are steps you can take to improve it:

- Pay your bills on time: Set up automatic payments or reminders to ensure you never miss a due date.

- Reduce your credit card balances: Aim to keep your credit utilization below 30%.

- Avoid opening new credit accounts: Only apply for credit when necessary, and space out your applications.

- Check your credit reports: Review your reports for errors and dispute any inaccuracies.

- Consider a credit-builder loan: These loans are designed to help you establish or improve your credit history.

Exploring Home Loan Options for First-Time Buyers

First-time homebuyers often have unique needs and may qualify for special loan programs. Some options to consider include:

- FHA loans: These government-backed loans require a lower down payment and have more flexible credit requirements.

- VA loans: Available to eligible veterans and service members, VA loans offer competitive rates and no down payment.

- USDA loans: These loans are designed for rural homebuyers and offer low-interest rates and no down payment.

When exploring home loan options, it's essential to consider the mortgage term length. Common options include 15-year and 30-year terms. A shorter term typically results in lower interest rates but higher monthly payments, while a longer term offers lower monthly payments but higher overall interest costs.

Summary:

Understanding your credit score and its impact on mortgage rates is crucial when applying for a home loan. By knowing how credit scores are calculated and taking steps to improve your score, you can secure better loan terms and save money over the life of your mortgage. Remember to explore all available home loan options, especially if you're a first-time buyer, and consider the mortgage term length that best fits your financial situation.