Overview

Managing your debt well can change your financial future. It can boost your credit score, get you better mortgage rates, and help you qualify for an FHA loan. This article dives into Debt Management for Better Credit, offering practical steps and real insights to guide you toward homeownership.

Understanding Debt Management

Debt management is all about taking charge of what you owe. It means making a plan to pay off debts—like credit cards or loans—in a smart way. You might use the debt snowball method, tackling small debts first, or the debt avalanche method, hitting high-interest debts. Some folks work with credit counseling agencies. These experts can lower your interest rates or set up a payment plan. Debt Management for Better Credit starts here—getting organized and staying consistent.

How Debt Management Affects Your Credit Score

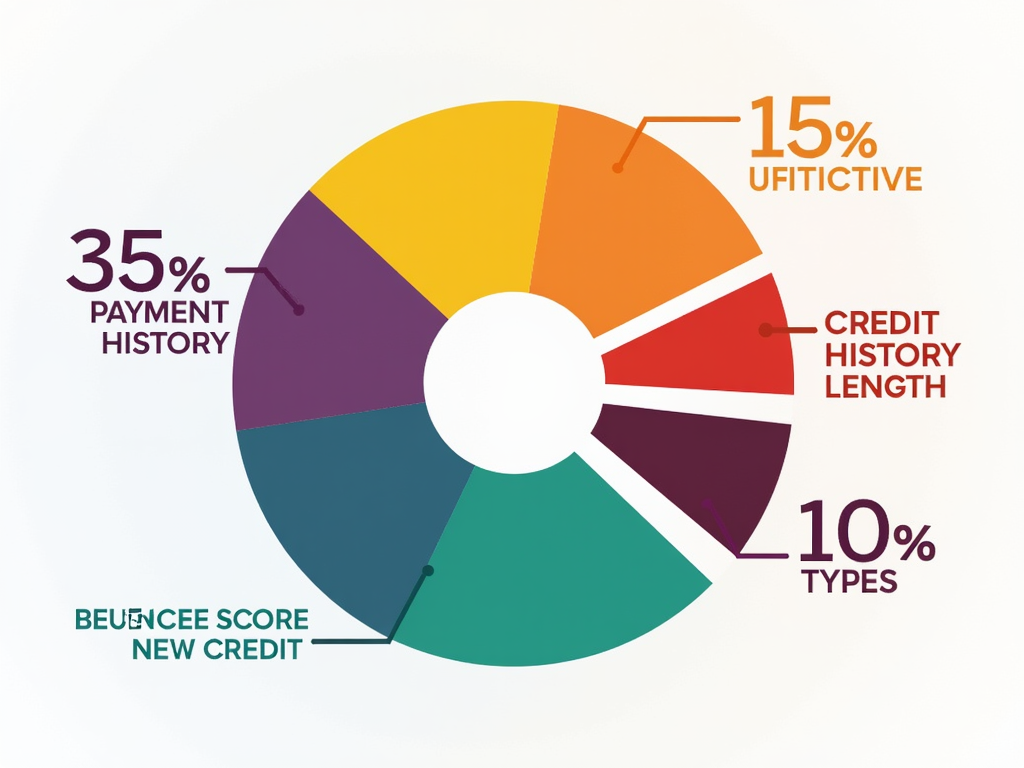

Your credit score depends on a few key things: paying bills on time (35%), how much of your credit you’re using (30%), and a few other factors like how long you’ve had credit. Good debt management helps by keeping payments on track and credit card balances low. For example, if your credit limit is $10,000, try to keep your balance under $3,000. Over time, this builds a stronger score, which lenders love to see.

Improving Your Credit Score for Better Mortgage Rates

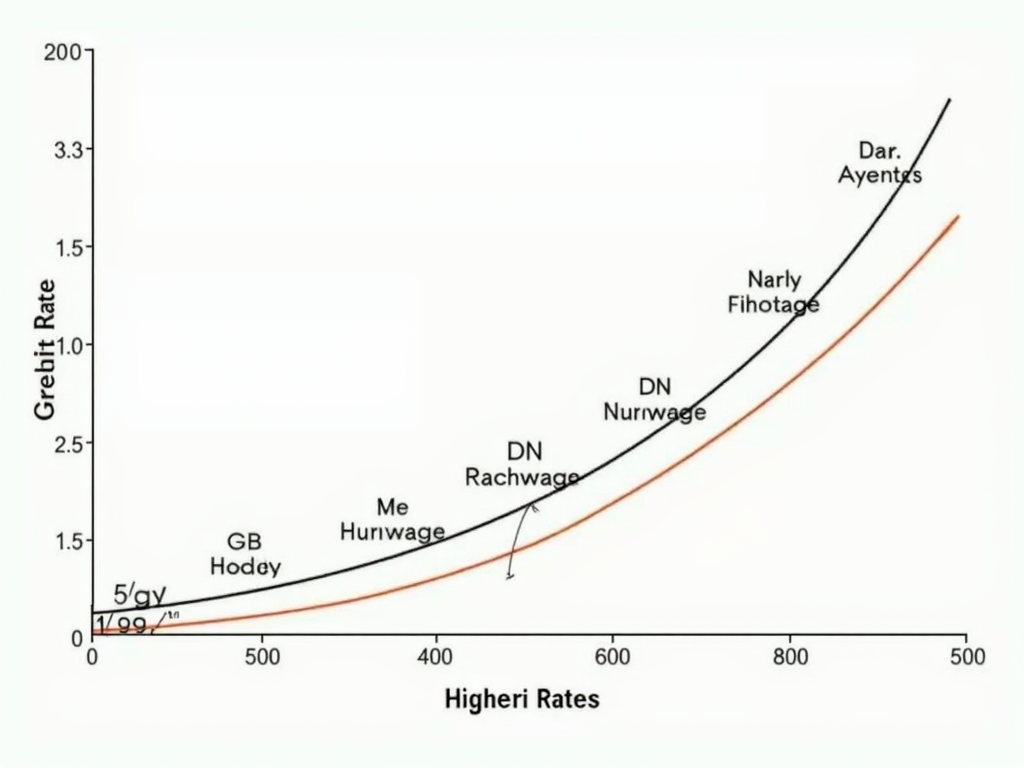

A higher credit score can save you thousands on a mortgage. How to Improve Your Credit Score for a Better Mortgage Rate starts with managing debt well. Lenders offer the best rates to people with scores above 760. If your score is below 620, you might pay more—or struggle to get approved. For instance, FICO data shows that a 720 score could get you a 3.5% rate, while a 650 might mean 4.5%. That’s a big difference over 30 years!

Navigating FHA Loan Requirements

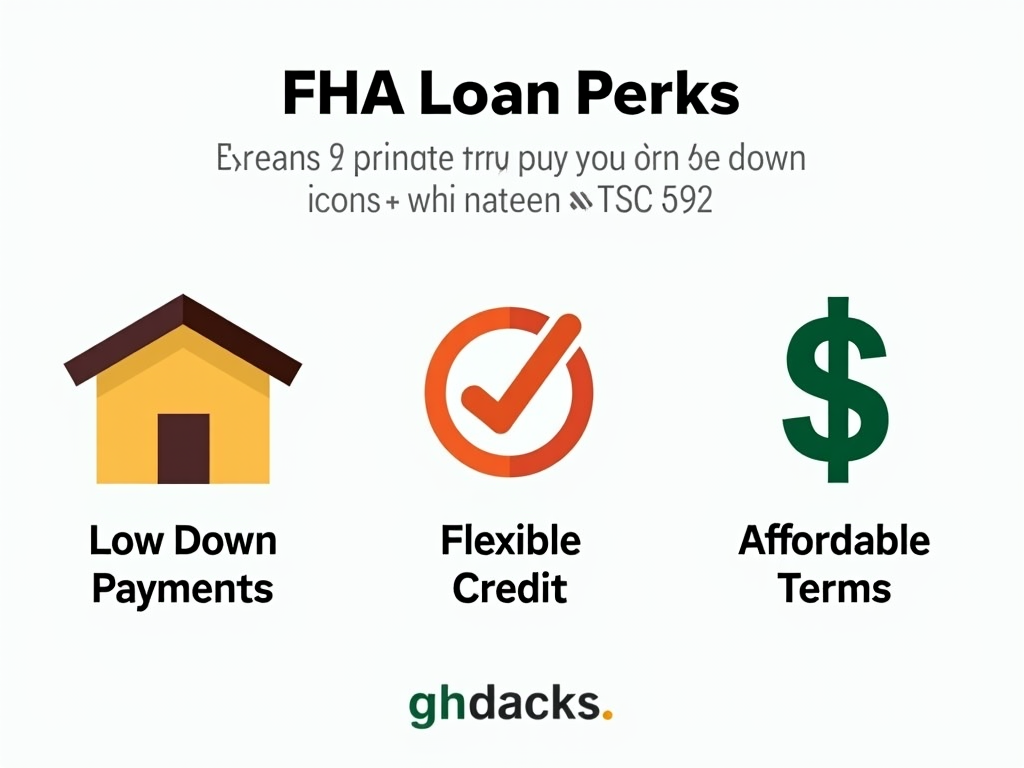

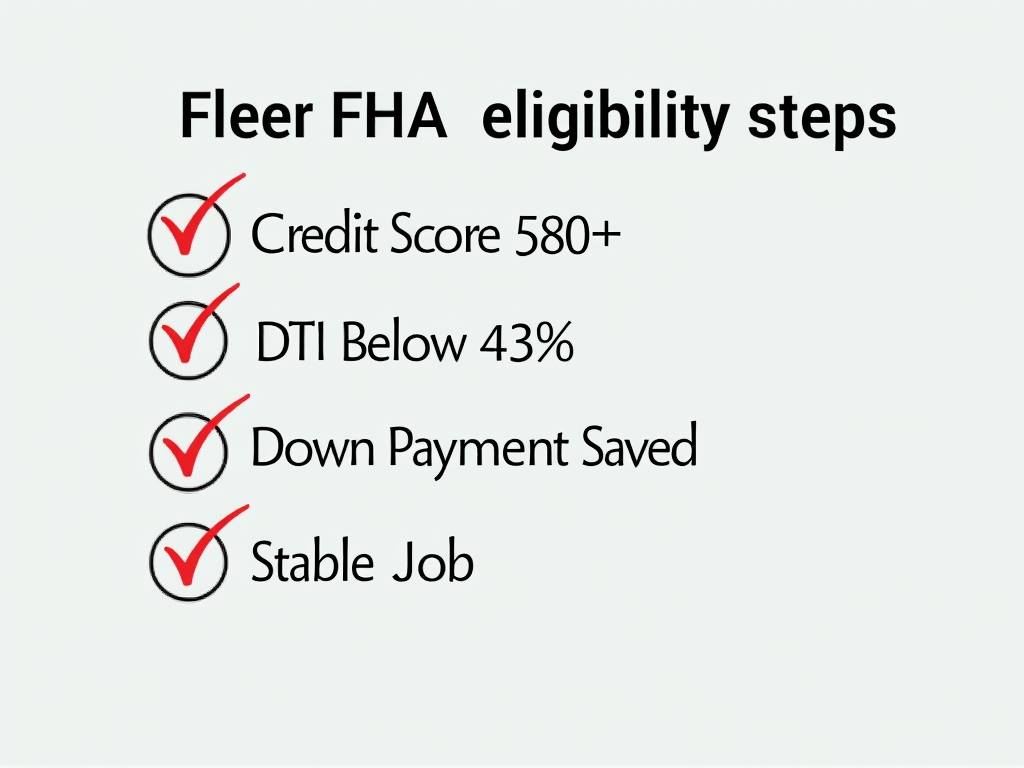

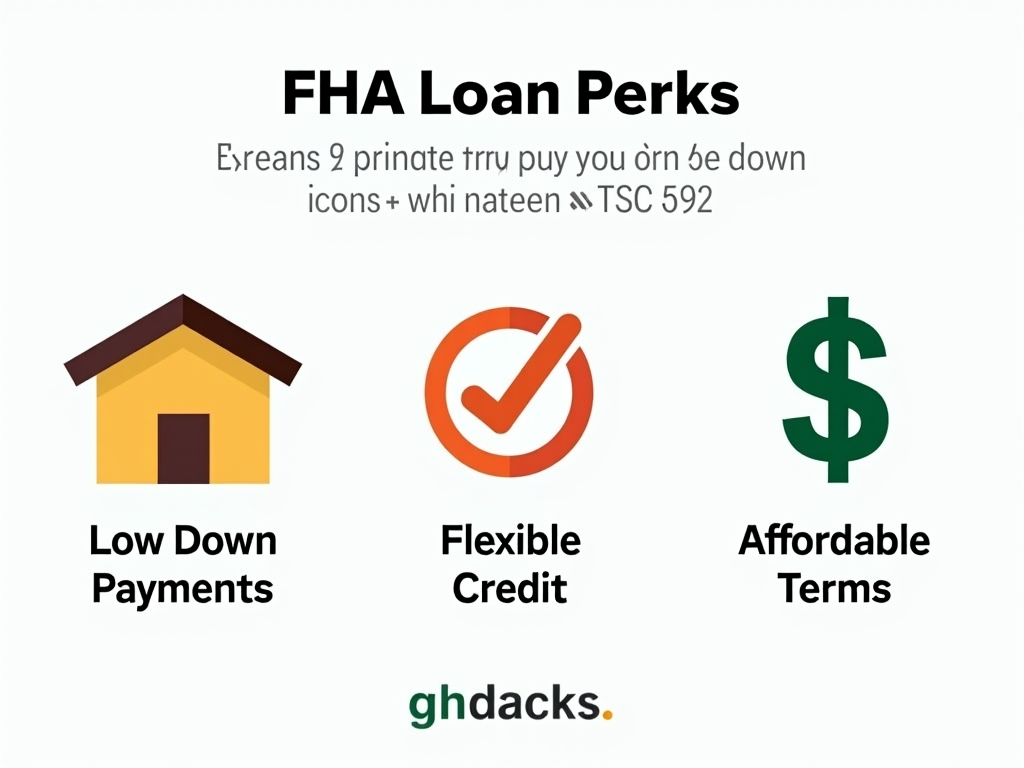

FHA loans, backed by the Federal Housing Administration, are great for first-time buyers. They need smaller down payments—like 3.5% if your credit score is 580 or higher. If it’s between 500 and 579, you’ll need 10%. Navigating FHA Loan Requirements also means keeping your debt-to-income ratio (DTI) under 43%. That’s your monthly debt payments divided by your income. Plus, you’ll pay mortgage insurance, but it’s a trade-off for easier approval.

Tips for Qualifying for an FHA Mortgage

Want to know How to Qualify for an FHA Mortgage? Here’s how:

- Check your credit: Get your score above 580 for the best terms.

- Cut debt: Pay down cards or loans to lower your DTI.

- Save up: Even 3.5% of a $200,000 home is $7,000.

- Stay employed: Lenders want two years of steady work.

I’ve seen friends turn things around by setting up auto-payments and catching up on late bills. Small steps add up!

Real Stories, Real Results

Take Sarah, a teacher I know. She had $15,000 in credit card debt and a 610 score. She joined a debt management program, paid off her cards in three years, and hit a 700 score. That got her an FHA loan with just 3.5% down. Stories like hers show that FHA Loan Eligibility is within reach if you stick to a plan.

Summary

Good debt management can transform your credit score, unlock better mortgage rates, and make FHA loans possible. It’s about paying on time, keeping balances low, and understanding FHA Loan Eligibility. With effort, you can own a home—and enjoy the peace of mind that comes with it.