Applying for a mortgage is a significant financial step. It's not just about finding your dream home; it's about ensuring you can afford it without compromising your financial stability. In this article, we'll guide you through the essential steps to manage your finances before you apply for a mortgage. From checking your credit score to saving for a down payment, these tips will help you prepare for a successful mortgage application.

Checking and Improving Your Credit Score

Your credit score is one of the first things lenders look at when you apply for a mortgage. It tells them how reliable you are at paying back debts. A higher credit score can get you better interest rates, which means lower monthly payments. So, how do you check and improve your credit score?

First, get a copy of your credit report from a trusted source. Look for any errors or outdated information that might be dragging your score down. If you find mistakes, dispute them with the credit bureau. Next, focus on paying your bills on time. Late payments can hurt your score, so set up reminders or automatic payments to stay on track. Also, try to pay down any existing debt, especially on credit cards. Keeping your credit card balances low shows lenders you're not overextended.

Here's a quick look at how credit scores can affect your mortgage rates:

| Credit Score Range | Likely Interest Rate |

|---|---|

| 760+ | Best rates |

| 700-759 | Good rates |

| 650-699 | Average rates |

| 600-649 | Higher rates |

| Below 600 | May not qualify |

Improving your credit score takes time, so start this process early—ideally, at least six months before you plan to apply for a mortgage.

Saving for a Down Payment

A down payment is the upfront cash you pay when buying a home. The more you can put down, the less you'll need to borrow, which can lower your monthly payments and help you avoid private mortgage insurance (PMI). But how do you save enough for a down payment?

Start by setting a savings goal. For example, if you're aiming for a 20% down payment on a $300,000 home, you'll need $60,000. Break this down into smaller, manageable amounts. Maybe you save $500 a month for 10 years, or $1,000 a month for 5 years. Open a separate savings account just for your down payment to keep it organized and avoid dipping into it for other expenses.

Here are some strategies to boost your savings: - Cut unnecessary expenses: Skip that daily coffee or cancel subscriptions you don't use. - Automate your savings: Set up automatic transfers to your down payment account each payday. - Look for extra income: Consider a side gig or selling items you no longer need.

Remember, while 20% is ideal, there are mortgage options that require less. However, putting down less than 20% usually means you'll have to pay PMI, which adds to your monthly costs.

Reducing Existing Debt

Lenders don't just look at your credit score; they also consider your debt-to-income (DTI) ratio. This is the percentage of your monthly income that goes toward paying debts. A lower DTI ratio shows lenders you have room in your budget for a mortgage payment.

To reduce your DTI ratio, focus on paying off high-interest debts first, like credit cards. You might also consider consolidating your debts into a single loan with a lower interest rate. Avoid taking on new debt in the months leading up to your mortgage application. Even a small increase in debt can affect your DTI ratio and your ability to qualify for a mortgage.

Let me share a quick story. A friend of mine was ready to apply for a mortgage but had a car loan and some credit card debt. By focusing on paying off the credit card first, she lowered her DTI ratio and qualified for a better interest rate. It took discipline, but it paid off in the long run.

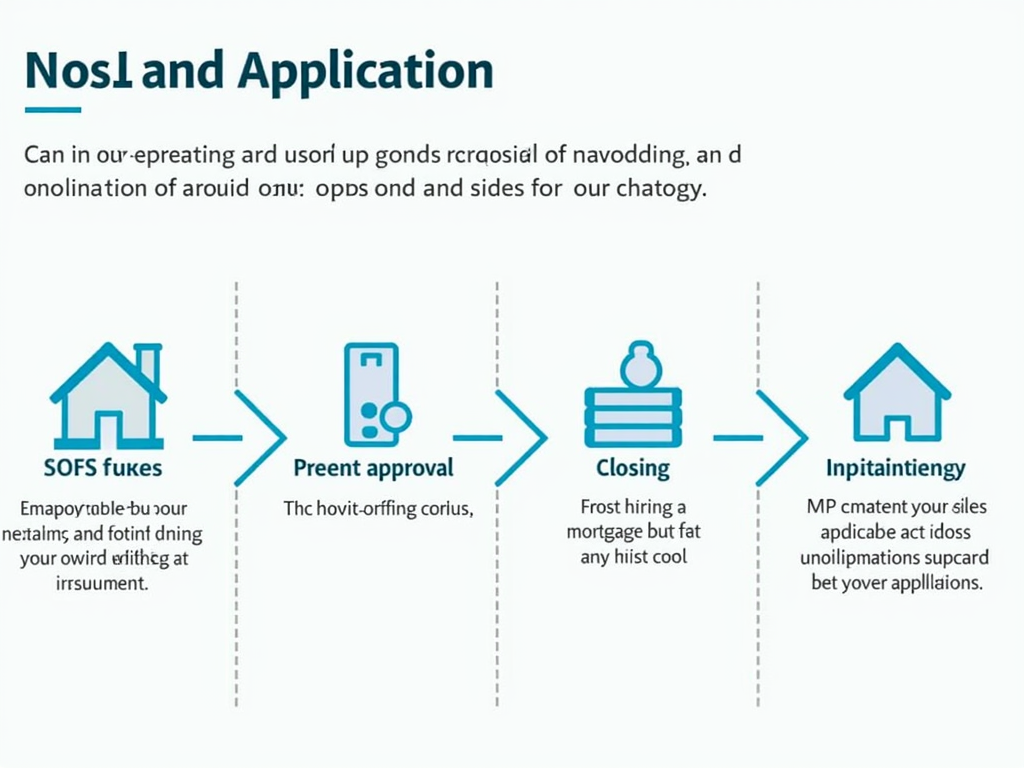

Understanding the Mortgage Application Process

Knowing what to expect during the mortgage application process can make it less stressful. Here's a simplified overview:

- Pre-approval: This is an initial assessment where the lender checks your credit and finances to give you an idea of how much you can borrow.

- House hunting: With pre-approval in hand, you can shop for homes within your budget.

- Formal application: Once you find a home, you'll submit a formal mortgage application, providing detailed financial information.

- Underwriting: The lender verifies your information and assesses the risk of lending to you.

- Closing: If approved, you'll sign the final paperwork and get the keys to your new home.

To make this process smoother, gather all necessary documents ahead of time. These typically include: - Proof of income (pay stubs, tax returns) - Bank statements - Identification - Details about the property you're buying

Having these documents ready can speed up the application process and show lenders you're organized and serious about buying a home.

Budgeting for Mortgage Payments

Before you apply for a mortgage, it's crucial to understand how much you can afford to pay each month. A common rule of thumb is that your monthly housing costs (mortgage, property taxes, insurance) shouldn't exceed 28% of your gross monthly income.

For example, if you earn $5,000 a month, your housing costs should be no more than $1,400. But don't forget to factor in other expenses like utilities, maintenance, and any homeowners association fees.

To get a clear picture, create a detailed budget. List all your income and expenses, and see how a mortgage payment fits in. There are plenty of online tools and apps that can help with this. By budgeting carefully, you can avoid the stress of being 'house poor'—where your mortgage takes up so much of your income that you struggle to cover other expenses.

In summary, managing your finances before applying for a mortgage is all about preparation. By checking and improving your credit score, saving for a down payment, reducing debt, understanding the application process, and budgeting carefully, you'll be in a strong position to secure a mortgage that fits your financial situation. Take these steps seriously, and you'll be well on your way to homeownership without the financial strain.