Buying your first home is a big step—exciting, but also a little scary. For many, figuring out how to pay for it is the hardest part. That’s where FHA loans come in. This guide explains everything you need to know about Understanding FHA Loans for First-Time Homebuyers, including how they work, their pros and cons, and how an FHA refinance can save you money later. Let’s dive in and make this journey easier for you!

What Are FHA Loans, Anyway?

An FHA loan is a mortgage backed by the Federal Housing Administration, a government group that helps people buy homes. Unlike regular loans from banks, FHA loans are insured by the government. This means if you can’t pay, the lender still gets their money. Because of this safety net, lenders can take a chance on people who might not qualify for other loans—like first-time buyers with lower credit scores or less cash for a down payment.

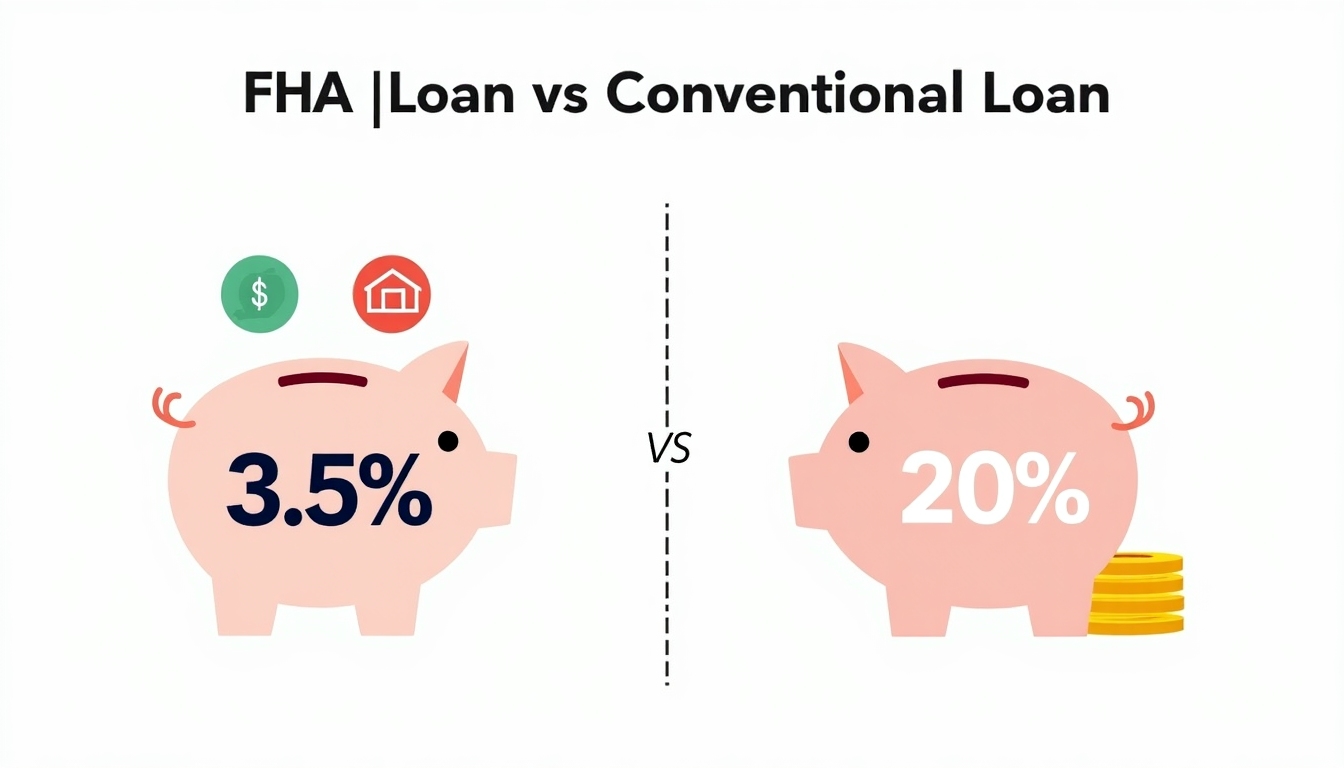

Here’s the best part: you only need 3.5% of the home’s price for a down payment. Compare that to the 20% some other loans ask for! Plus, you can get approved with a credit score as low as 580, or even 500 if you can put down 10%. That’s why FHA mortgages are so popular with new buyers.

Why FHA Loans Work for First-Time Buyers

FHA loans have some big wins that make them a go-to for people like you. Here’s what stands out:

-

Small Down Payment: Only 3.5% down means you don’t need years to save up. For a $200,000 house, that’s just $7,000!

-

Easier Credit Rules: Got a credit score of 580? You’re in. Even with a 500, you’ve got a shot—just bring more cash upfront.

-

Lower Rates: Since the government backs these loans, interest rates are often better than what you’d get elsewhere.

-

Fixer-Upper Help: With a 203(k) FHA loan, you can borrow extra to fix up a home that needs work. Perfect if you’re eyeing a diamond in the rough.

I remember my friend Sarah, a single mom, who thought she’d never own a home. Her credit wasn’t perfect, and she had just $5,000 saved. An FHA loan got her into a cute fixer-upper, and she’s been building equity ever since.

The Downsides You Should Know

No loan is perfect, and FHA loans have some catches. Here’s what to watch for:

-

Extra Insurance Costs: You’ll pay a fee upfront (about 1.75% of the loan) and a yearly fee (0.45% to 1.05%). These stick around unless you switch to a different loan later.

-

Picky House Rules: The home has to pass safety checks. If it’s too run-down, you might need that 203(k) loan or look elsewhere.

-

Loan Caps: There’s a limit to how much you can borrow, based on where you live. In pricey areas, this can feel tight.

-

Seller Hesitation: Some sellers shy away from FHA buyers, thinking the process is trickier. A good real estate agent can help with this.

These aren’t dealbreakers, but they’re worth thinking about. Weigh them against how much you need that lower down payment.

FHA Streamline Refinance Explained

Got an FHA loan already? The FHA streamline refinance could save you cash. It’s a simple way to tweak your loan without the usual hassle. Here’s the scoop:

-

No Home Check: Most times, you skip the appraisal. That’s less stress and fewer fees.

-

Less Paperwork: No need to prove your income again. If you’ve paid on time, you’re likely good to go.

-

Better Rates: If rates drop, this locks in savings. My cousin refinanced his FHA mortgage and cut his payment by $150 a month!

You need to have paid for six months and not be behind. The catch? You can’t pull cash out—it’s just for lowering payments or changing the loan term. Still, it’s a sweet deal if rates fall.

Tips to Make FHA Loans Work for You

Ready to jump in? These tips will help you get the most out of an FHA loan:

-

Boost Your Credit: Even if 580 works, a higher score means better rates. Pay off small debts or fix credit report mistakes.

-

Save Smart: Aim for that 3.5% down, plus some extra for closing costs—usually 2-5% of the price.

-

Get Pre-Approved: This shows sellers you mean business and helps you know your budget before you fall for a house.

-

Plan for Insurance: Those extra fees add up. Budget $100-$200 more a month, depending on your loan size.

-

Find a Pro: Work with a lender who knows FHA loans inside out. They’ll spot issues early and keep things smooth.

When I helped my brother buy his first place, pre-approval made all the difference. He found a home fast because sellers trusted his offer.

Wrapping It Up

FHA loans open doors for first-time homebuyers like you. With a low down payment, easier credit rules, and options like the FHA streamline refinance explained here, they’re a solid choice. Sure, there are extra costs and rules, but for many, the chance to own a home outweighs that. Take your time, talk to a lender, and see if an FHA mortgage fits your dreams. You’ve got this!