How to Choose the Right Mortgage for You

Choosing the right mortgage can be overwhelming, but understanding your options, especially FHA loans, can make the process smoother. This guide will walk you through the steps to find the best mortgage for your needs.

Understanding Your Mortgage Options

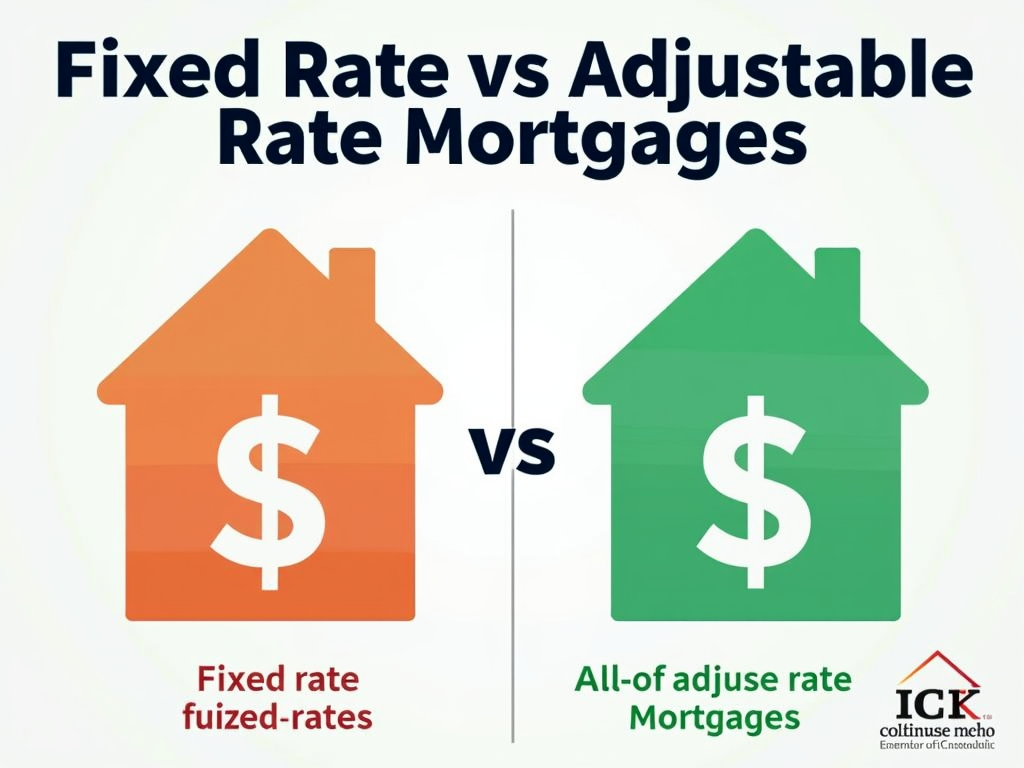

When considering a mortgage, it's essential to explore the various types available. From fixed-rate to adjustable-rate mortgages (ARMs), each option comes with its own set of advantages and disadvantages.

Fixed-Rate Mortgages: These loans maintain the same interest rate throughout the loan's term, making your monthly payments predictable. Ideal for buyers who plan to stay in their homes long-term.

Adjustable-Rate Mortgages (ARMs): These loans start with a lower interest rate that may adjust after a specified period, leading to potentially lower initial payments. Suitable for buyers who might sell or refinance before the rate adjusts.

Why Consider an FHA Loan?

FHA loans are particularly appealing for first-time homebuyers due to their lower down payment requirements and lenient credit score criteria.

Advantages of FHA Loans: - Lower Down Payment: As little as 3.5% down, making it accessible for more buyers. - Flexible Credit Requirements: FHA loans are available for those with lower credit scores, increasing your chances of approval. - Assumable Mortgage: If you sell your home, the buyer can take over your FHA loan, potentially at a lower rate than current market rates.

Step-by-Step Guide to Applying for an FHA Loan

- Check Your Eligibility: Determine if you meet the FHA's guidelines, including credit scores above 580 or a down payment of at least 3.5%.

- Gather Required Documents: Typical documents include tax returns, proof of income, bank statements, and a credit report.

- Choose a Lender: Research and compare lenders who offer FHA loans, as rates and fees can vary significantly.

- Complete the Application: Submit your application along with the required documents. Ensure that all information is accurate to avoid delays.

- Wait for Approval: Lenders will assess your financial situation and will inform you of their decision. This process can take several days to weeks, depending on the lender.

- Home Appraisal: An FHA-approved appraiser will evaluate the property to ensure it meets minimum standards and is worth the amount you're borrowing.

Tips for Choosing the Right Mortgage

- Assess Your Financial Situation: Before choosing a mortgage, evaluate your financial health, including credit score, income stability, and debts.

- Consider Future Plans: Think about how long you plan to stay in the home. If it’s a long-term commitment, a fixed-rate mortgage may be best.

- Consult with Professionals: Talk to mortgage advisors or financial planners who can provide personalized advice based on your circumstances.

Common Mistakes to Avoid

- Ignoring Additional Costs: Don't forget about property taxes, insurance, and maintenance when budgeting for your home.

- Focusing Solely on Interest Rates: While important, also consider loan terms and fees.

Conclusion

Choosing the right mortgage is a crucial step in the homebuying process. By understanding your options and considering an FHA loan, you can find a mortgage that fits your needs and budget. Remember to consult with a mortgage professional to explore all your options.