Choosing the Right Mortgage for Your Future

Choosing between a fixed-rate and an adjustable-rate mortgage is a crucial decision for homebuyers. This article will help you understand the differences, benefits, and potential risks of each type, so you can make an informed choice that aligns with your financial goals.

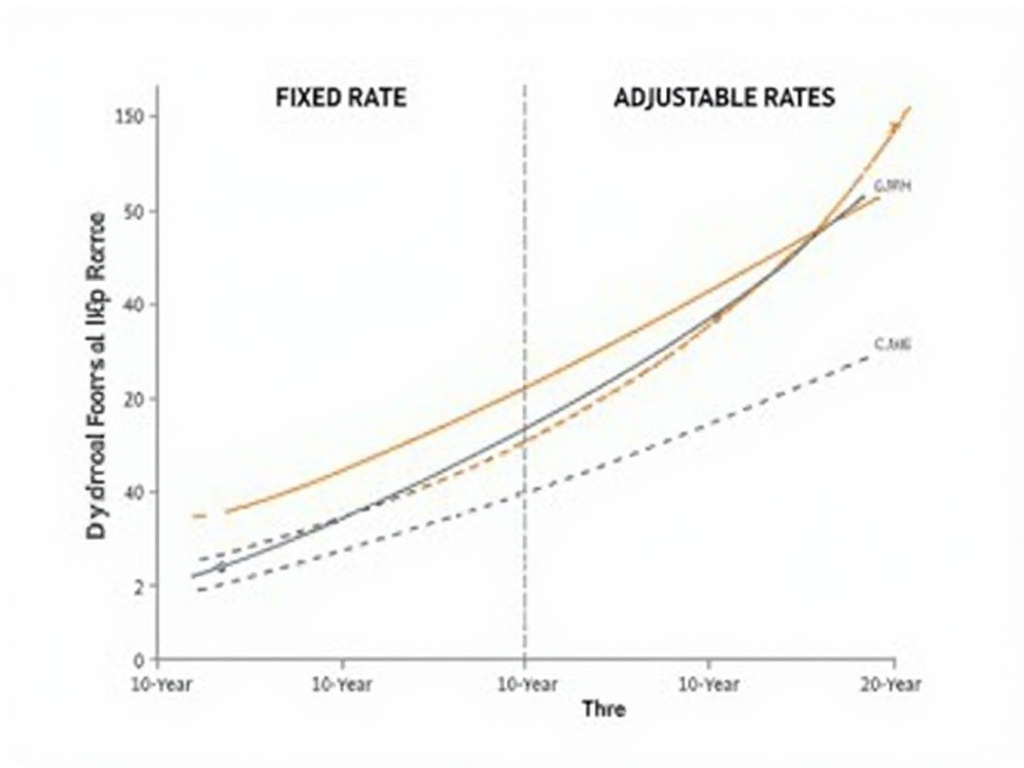

Understanding Fixed-Rate Mortgages

Fixed-rate mortgages have a constant interest rate throughout the loan term. This characteristic provides predictability in your monthly payments, which can be essential for budgeting. With a fixed-rate mortgage, you know exactly how much you'll pay every month for the entire term of the loan, regardless of market fluctuations.

The Pros and Cons of Fixed-Rate Mortgages

Pros:

- Stable Payments: Your payment amount won't change.

- Protection Against Rising Rates: If interest rates rise in the future, you’ll remain unaffected.

Cons:

- Higher Initial Rates: Fixed-rate mortgages generally start with a higher interest rate than adjustable-rate mortgages (ARMs).

Understanding Adjustable-Rate Mortgages (ARMs)

Adjustable-rate mortgages have interest rates that fluctuate based on market conditions. Typically, ARMs start with a lower initial rate that can increase or decrease at specific intervals over the term of the loan.

The Pros and Cons of Adjustable-Rate Mortgages

Pros:

- Lower Initial Rates: You can benefit from lower payments at the beginning of the loan.

- Potential Savings: If interest rates decrease, your payments can adjust downward.

Cons:

- Risk of Rate Increases: Your interest rate and monthly payments can go up, which could lead to affordability issues in the future.

- Payment Uncertainty: Monthly payments can be unpredictable, making long-term financial planning more difficult.

Personal Insights on Mortgage Choices

Imagine you're planning to stay in your home for many years. A fixed-rate mortgage might be more appealing because you can lock in a rate and not worry about future increases. On the other hand, if you think you might move in a few years, an ARM could save you money initially.

Choosing the Right Mortgage Lender

Selecting a mortgage lender is as important as choosing the right mortgage type. Consider the following factors: interest rates, fees, customer service, and lender reputation. Compare multiple lenders and think about your long-term financial plans.

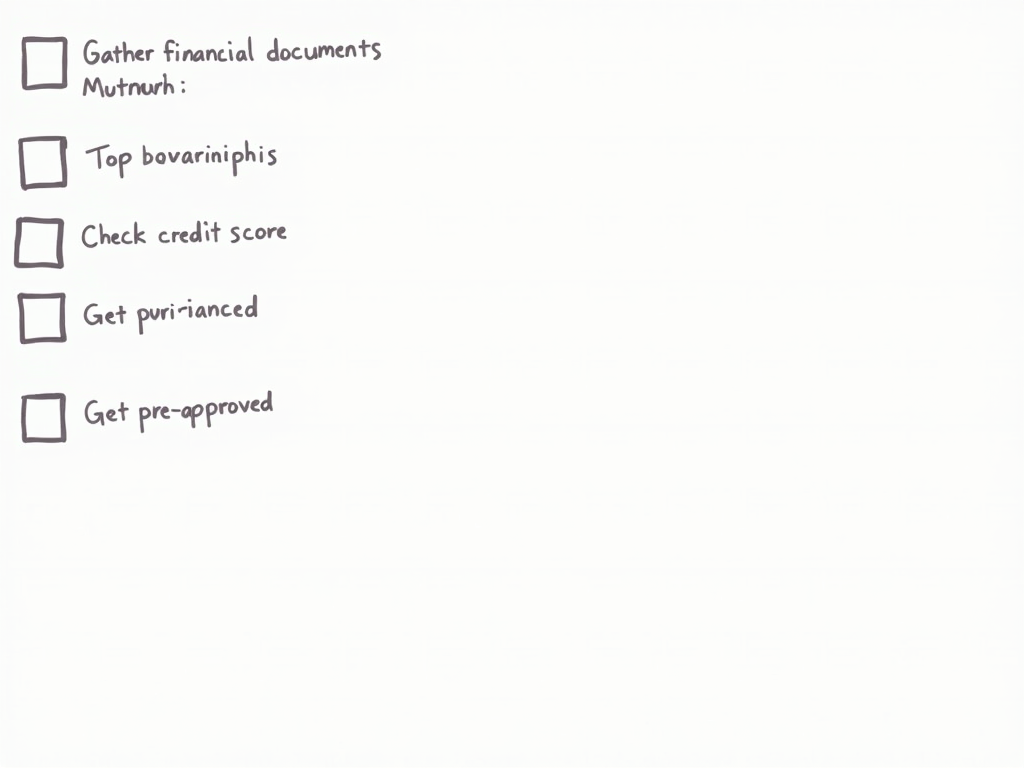

Mortgage Application Checklist

Here's a simple checklist to prepare for your mortgage application: 1. Gather financial statements (pay stubs, bank statements). 2. Check your credit score. 3. Get pre-approved to understand your budget.

Conclusion: Making an Informed Decision

In summary, understanding the differences between fixed-rate and adjustable-rate mortgages is crucial. Consider your personal financial situation and goals when choosing between them, and prepare thoroughly for the mortgage application process. Consulting with a financial advisor or mortgage professional can also provide personalized advice.