Overview

Buying a home is exciting, but the mortgage process can feel overwhelming. Don’t stress! This guide explains essential mortgage terms in simple language, helping you understand your loan and work with your mortgage lender like a pro. Let’s get started.

Why Mortgage Terms Matter

When I helped my sister buy her first home, we faced a wall of confusing words. Principal? Escrow? It was a lot. Understanding these terms made all the difference. They’re the building blocks of your mortgage, and knowing them empowers you to make smart choices.

What Is a Mortgage?

A mortgage is a loan you get to buy a home. You borrow money from a mortgage lender—like a bank—and pay it back over time with interest. The house is collateral, meaning the lender can take it if you miss payments.

It’s not just a loan, though. It’s a commitment. My neighbor once told me his mortgage felt like a marathon—long but worth it. Let’s break down the key terms so you can run your own race confidently.

1. Down Payment

Your down payment is the cash you pay upfront for your home. It’s a percentage of the price—like 10% of a $200,000 house, which is $20,000. The rest you borrow.

A bigger down payment can lower your monthly bill. When I saved for mine, I skipped fancy coffees for a year. It paid off—I avoided extra fees like PMI, which we’ll cover soon.

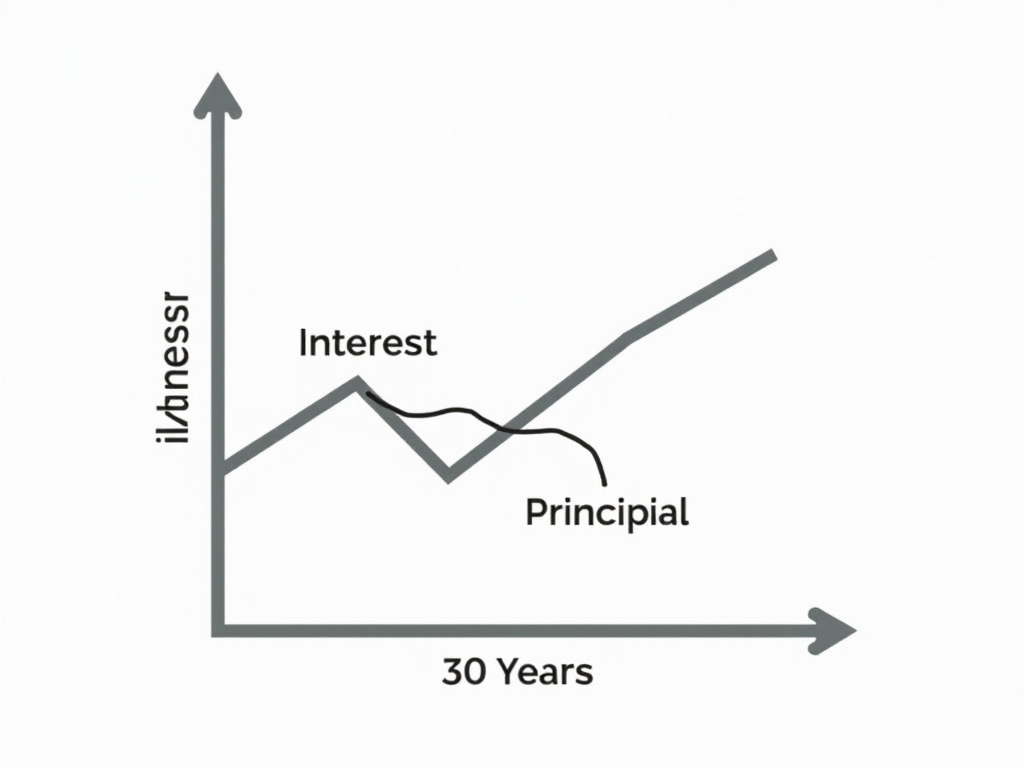

2. Principal

The principal is the amount you borrow. If your home costs $200,000 and you put down $20,000, your principal is $180,000. You’ll pay this back over time.

Think of it as the heart of your mortgage. Every payment chips away at it, bringing you closer to owning your home outright.

3. Interest

Interest is what you pay the lender for borrowing money. It’s a percentage of the principal. A 5% rate on $180,000 means you pay $9,000 in interest yearly—at first.

Early on, most of your payment goes to interest. Over time, that flips. I remember checking my first statement—shocking how little went to the principal! But it gets better.

4. Amortization

Amortization is how your loan gets paid off through regular payments. Most mortgages last 15 or 30 years. Each payment covers interest and principal, slowly reducing your debt.

I once made an extra payment and shaved months off my loan. An amortization schedule shows you this magic—ask your lender for one!

5. Escrow

Escrow is an account your lender manages to pay taxes and insurance. Part of your monthly payment goes there, and they handle the bills when due.

It’s like having a helper. My escrow caught a tax hike I’d have missed—saved me a headache!

6. Private Mortgage Insurance (PMI)

If your down payment is under 20%, you might need PMI. It protects the lender if you can’t pay. It’s an extra monthly cost—maybe $50-$100.

Once you own 20% of your home, you can ditch PMI. My friend did this after two years of extra payments—huge relief!

7. Closing Costs

Closing costs are fees you pay when you seal the deal—think appraisals or legal stuff. They’re usually 2-5% of the home price, so $4,000-$10,000 on a $200,000 house.

Budget for these! I didn’t at first and scrambled at closing. Some lenders let you roll them into the loan, but you’ll pay interest on that.

8. Mortgage Lender Requirements for Approval

Getting a mortgage means meeting your mortgage lender’s rules. Here’s what they check:

- Credit Score: Aim for 620 or higher. It shows you handle debt well.

- Debt-to-Income Ratio (DTI): Keep debt under 43% of your income.

- Job History: Two years steady work looks good.

- Down Payment: More is better.

- Appraisal: The home must match the loan amount.

I got pre-approved before shopping—it was like having a golden ticket. It tells sellers you’re serious and helps you set a budget.

Real-Life Tips

Here’s what I’ve learned navigating mortgages:

- Compare Lenders: Rates vary. I saved $1,000 yearly by shopping around.

- Ask Questions: My lender explained escrow when I was clueless—huge help.

- Check Details: Read every paper before signing.

- Plan Ahead: A 30-year loan fit my budget better than 15.

When my sister bought her house, she haggled closing costs down. Little moves like that add up!

Summary

Mastering essential mortgage terms explained here—like down payments, interest, and escrow—sets you up for success. You’ll talk to your mortgage lender with confidence and understand their requirements for approval. Homeownership is a big step, but you’ve got this!

Take it slow, ask for help, and enjoy the ride. Your dream home is closer than you think. Check out the readings below for more tips!