FHA loans are a popular choice for first-time homebuyers and those with less-than-perfect credit. These loans are insured by the Federal Housing Administration (FHA), which allows lenders to offer more favorable terms to borrowers. However, like any mortgage, FHA loans come with various costs that borrowers need to be aware of. In this article, we'll break down the different costs associated with FHA loans, including mortgage insurance premiums and closing costs, and provide tips on how to manage these expenses effectively.

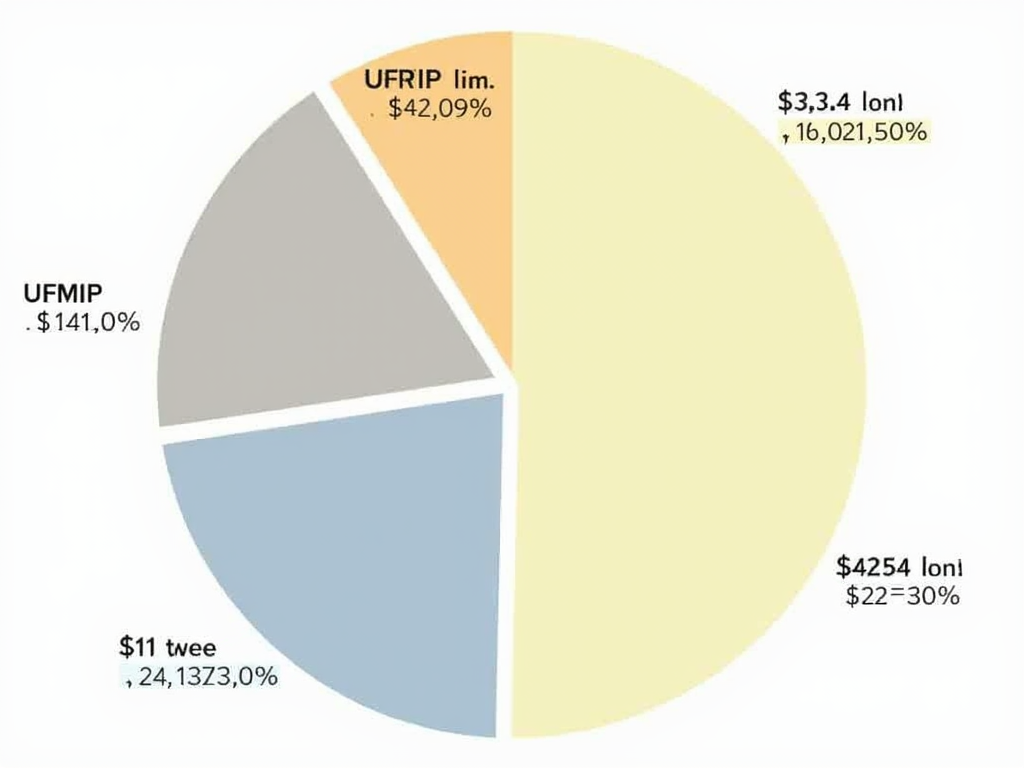

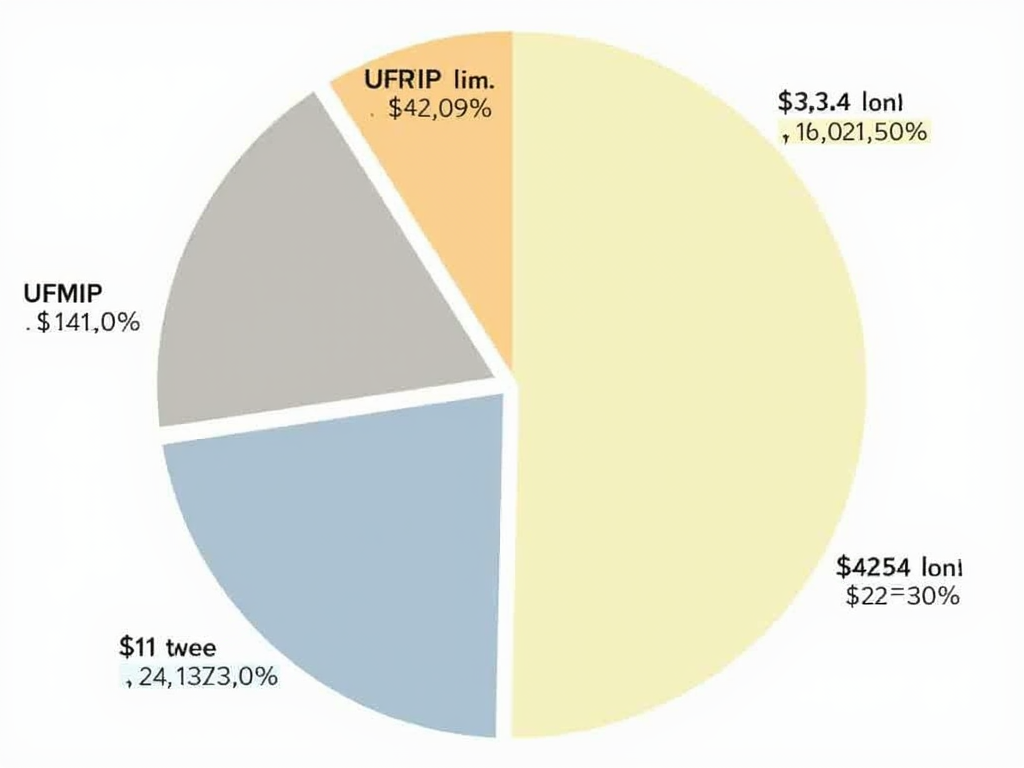

One of the key costs associated with FHA loans is the upfront mortgage insurance premium (UFMIP). This is a one-time fee that borrowers pay at closing to insure the loan. The UFMIP is typically 1.75% of the loan amount and can be financed into the mortgage or paid in cash at closing.

Another significant cost is the annual mortgage insurance premium (MIP), which is paid monthly as part of the mortgage payment. The MIP varies based on the loan amount, loan term, and loan-to-value ratio. For most FHA loans, the MIP ranges from 0.45% to 1.05% of the loan amount per year.

In addition to mortgage insurance premiums, borrowers also need to consider closing costs when obtaining an FHA loan. Closing costs can include appraisal fees, title insurance, origination fees, and other expenses. These costs can vary depending on the lender and the location of the property.

To manage the costs associated with FHA loans, borrowers can take several steps. First, they can shop around for lenders to find the best rates and fees. Borrowers can also consider paying the UFMIP in cash at closing to avoid financing it into the mortgage, which can save on interest over the life of the loan. Additionally, borrowers can work on improving their credit scores to qualify for lower MIP rates.

For borrowers who already have an FHA loan, refinancing can be a way to reduce costs. The FHA streamline refinance program allows borrowers to refinance their existing FHA loan with minimal documentation and underwriting. This can help borrowers take advantage of lower interest rates and reduce their monthly mortgage payments.

However, it's important to note that refinancing also comes with costs, such as closing costs and potentially a new UFMIP. Borrowers should carefully consider whether the potential savings from refinancing outweigh the costs involved.

In conclusion, understanding the costs associated with FHA loans is crucial for borrowers to make informed decisions about their mortgage options. By being aware of the various costs involved and taking steps to manage them effectively, borrowers can save money and achieve their homeownership goals.