Overview:

FHA loans, insured by the Federal Housing Administration, offer a pathway to homeownership for many who might not qualify for conventional loans. With lower down payments and more lenient credit requirements, these loans are particularly beneficial for first-time buyers or those with limited savings. This article explores the advantages of FHA loans, focusing on how lower down payments can make buying a home more accessible.

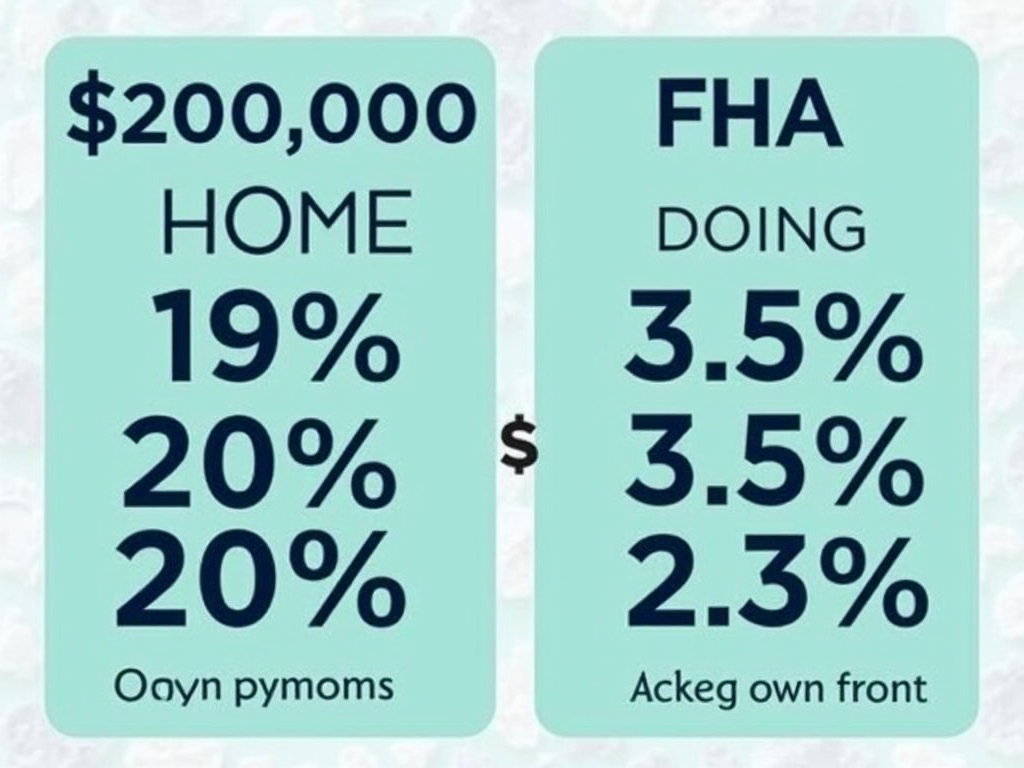

Homeownership is a dream for many, but saving for a big down payment can feel like climbing a mountain. Traditional loans often demand 20% down, which could mean years of saving. That’s where FHA loans shine. With a down payment as low as 3.5%, these loans open the door to owning a home sooner and with less cash upfront.

What is an FHA Loan?

An FHA loan is a mortgage backed by the Federal Housing Administration. This government insurance gives lenders confidence to offer better terms, like lower down payments. These loans are a favorite among first-time buyers because they’re easier to qualify for than conventional loans, especially if your credit isn’t perfect or your savings are slim.

Benefits of Lower Down Payments

The standout feature of FHA loans is the lower down payment. Here’s why that’s a big deal:

- More Affordable: You only need 3.5% of the home’s price, making it easier to get started.

- Quicker Ownership: No need to save for a decade—you can buy now instead of later.

- Extra Cash: With less money tied up in the down payment, you’ve got funds for moving, repairs, or emergencies.

Imagine a $200,000 home. A conventional loan might ask for $40,000 down. With an FHA loan, you’re looking at just $7,000. That’s a huge gap—money you can use elsewhere instead of locking it all into the house right away.

FHA Loan Requirements 2024

To get an FHA loan in 2024, you’ll need to meet a few standards:

- Credit Score: At least 500, but 580 or higher gets you the 3.5% down payment.

- Debt-to-Income Ratio: Your debts shouldn’t eat up more than 43% of your monthly income.

- Job History: Two years of steady work usually does the trick.

- Home Standards: The property has to be safe and solid.

Compared to conventional loans, these rules are pretty relaxed, giving more people a shot at owning a home.

My Own Experience

When I bought my first place, I didn’t have a pile of cash sitting around. A 20% down payment felt impossible. Then I found out about FHA loans. With just 3.5% down, I got into my home way faster than I expected. Plus, I had some money left for furniture and fixes. It was a relief knowing I wasn’t starting from zero.

More Perks of FHA Loans

Lower down payments aren’t the only win with FHA loans. Check these out:

- Credit Flexibility: A bumpy credit history won’t automatically shut you out.

- Property Options: Buy a single-family home, a small apartment building (up to four units), or even a manufactured home.

- Future Selling Point: These loans can be passed on to a buyer later, which might make your home more appealing.

The numbers back this up. The U.S. Department of Housing and Urban Development says FHA loans have helped millions since 1934. In 2023 alone, over 800,000 were issued—proof they’re still a go-to for homebuyers.

Is an FHA Loan for You?

FHA loans aren’t perfect for everyone. Here’s what to think about:

- Insurance Costs: You’ll pay mortgage insurance premiums, which add to your monthly bill.

- Borrowing Caps: There’s a limit to how much you can borrow, depending on where you live.

- Home Rules: The property has to pass certain checks, which might narrow your choices.

Balance these against the benefits to see if it fits your needs.

Wrapping Up

FHA loans break down barriers to homeownership with lower down payments and easier qualification rules. They’re a lifeline for first-timers or anyone short on savings, letting you buy a home without draining your bank account. If you’re ready to take that step, look into FHA loan programs to see if they’re your ticket to a new front door.