Mortgage rates can feel like a mystery, but they’re shaped by clear factors like the economy, inflation, and your credit score. Knowing what drives these rates helps you plan better when getting a mortgage.

How the Economy Moves Mortgage Rates

The economy is a big player in setting mortgage rates. When things are booming—think low unemployment and lots of shopping—lenders raise rates. More people want loans, so they can charge more. But when the economy slows down, with fewer jobs and less spending, rates drop. Lenders lower them to tempt borrowers. I’ve seen this myself: during tough times, friends locked in lower rates, saving thousands.

Inflation’s Role in Your Mortgage

Inflation affects how much your money is worth. When prices climb fast, lenders push mortgage rates up. They need to make up for money losing value over time. Low inflation, though? Rates stay friendlier. Back when I was house-hunting, inflation was steady, and I snagged a solid rate—proof this stuff matters.

The Federal Reserve’s Influence

The Federal Reserve, or the Fed, tweaks interest rates to guide the economy. When they hike rates, banks pay more to borrow, so mortgage rates climb. When they cut rates, borrowing gets cheaper, and mortgage rates often fall. Curious about the Fed? Check out their official site for the full scoop.

Why Your Credit Score Counts

Your credit score tells lenders how risky you are. A high score—like 750 or above—can get you a lower mortgage rate. Lenders trust you’ll pay on time. A lower score? Rates go up, or you might not qualify. I boosted my score 50 points before applying for my mortgage—it made a real difference. Learn more from Experian’s guide.

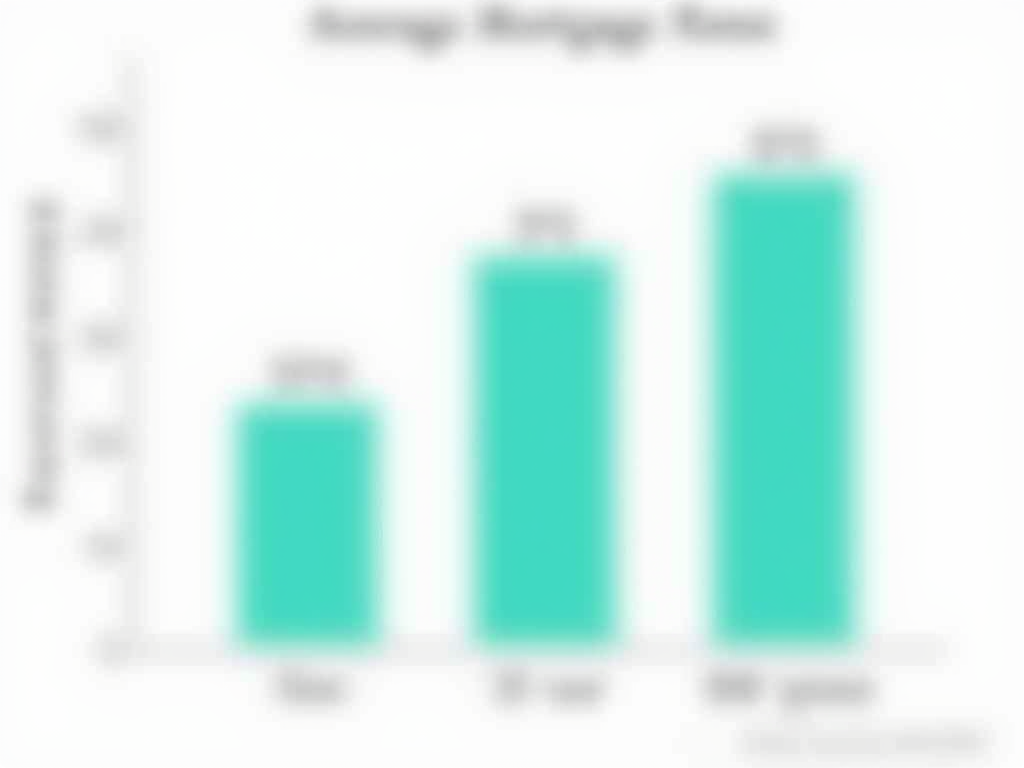

Loan Term: Short vs. Long

How long your mortgage lasts changes the rate. Shorter loans, like 15 years, usually have lower rates. Lenders risk less since you pay faster. Longer ones, like 30 years, come with higher rates but smaller monthly payments. I went with 30 years to keep my budget flexible, even though the rate was a bit higher.

Down Payment Size Matters

A bigger down payment can lower your mortgage rate. It shows lenders you’re serious and cuts their risk—you own more of the home upfront. Saving 20% instead of 10% once got me a better deal. Even 5% more can help.

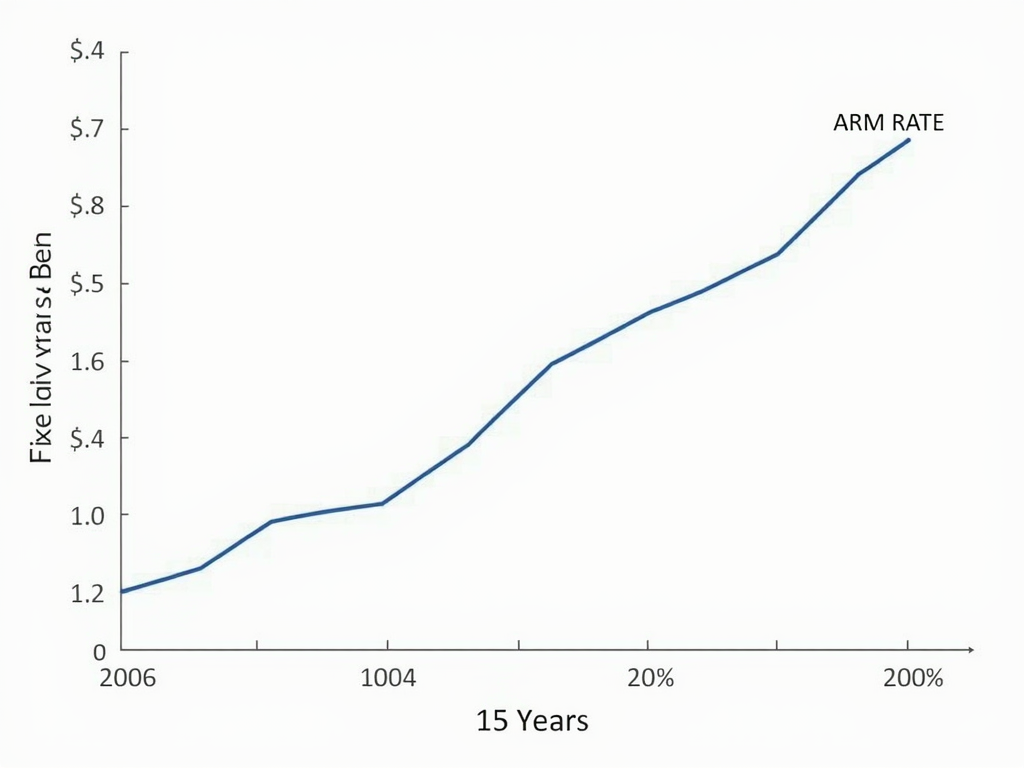

Fixed or Adjustable: Loan Type Impact

The type of mortgage you pick affects the rate. Fixed-rate mortgages start higher but stay steady—great for planning. Adjustable-rate mortgages (ARMs) begin lower but can rise later. I chose fixed for peace of mind, though ARMs tempt with early savings. Here’s a solid breakdown from Freddie Mac on rate trends.

Tips to Navigate Mortgage Rates

You can’t control the economy, but you can act smart. Boost your credit score by paying bills on time. Save for a bigger down payment. Compare loan types and terms. Shop around—lenders offer different rates. I saved half a percent by checking three banks.

Putting It All Together

Mortgage rates hinge on the economy, inflation, Fed moves, your credit, loan term, down payment, and loan type. Understanding these factors that affect mortgage rates lets you time your move or tweak your plan. It’s not just numbers—it’s your future home.