Understanding FHA Mortgages

Applying for a Federal Housing Administration (FHA) mortgage can be a straightforward process if you are prepared. This guide will help you understand the FHA mortgage application process, the requirements, and how to increase your chances for approval.

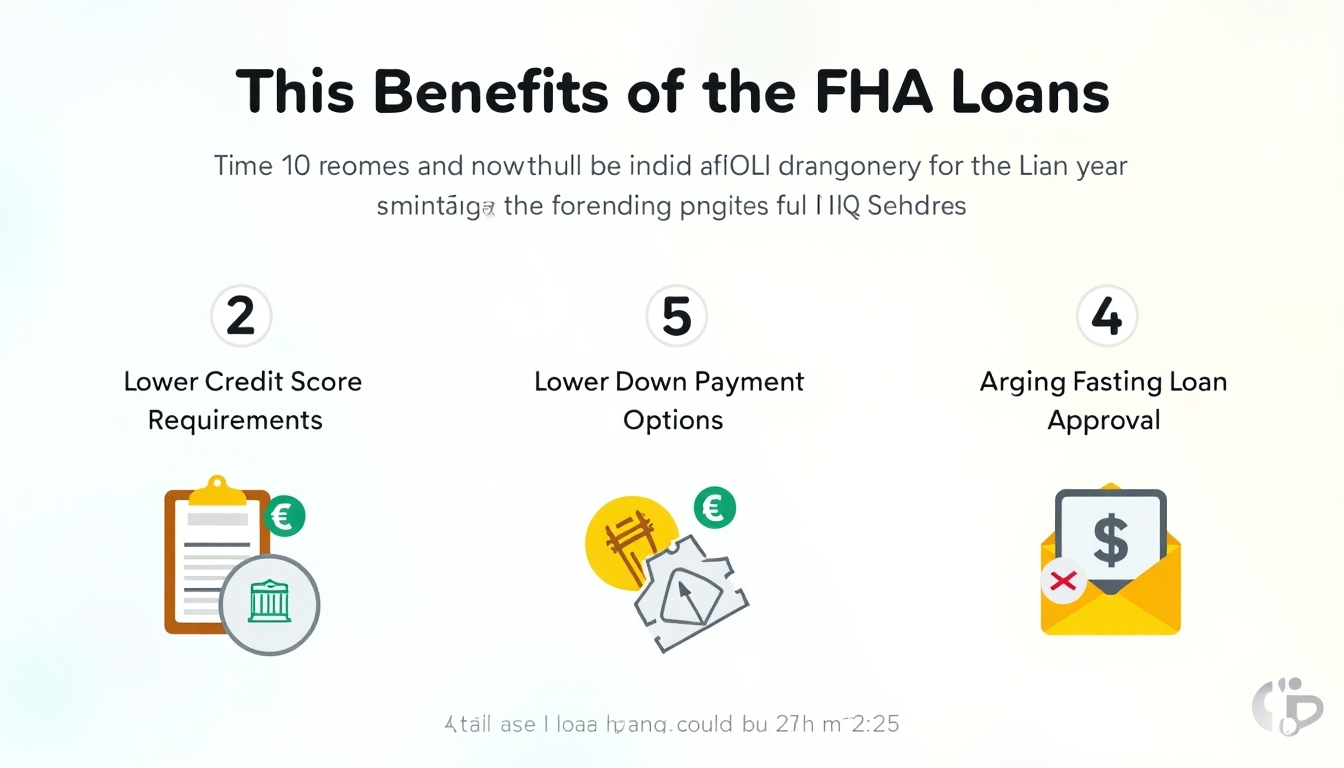

FHA mortgages are government-backed loans designed to help low-to-moderate income borrowers purchase homes. Unlike conventional loans, FHA loans are easier to qualify for, making homeownership accessible to more people.

Key Benefits of FHA Mortgages

- Lower Credit Requirements: Often, a credit score of 580 or higher is sufficient.

- Smaller Down Payments: You can pay as little as 3.5% down.

- Flexible Qualifications: Accepts higher debt-to-income ratios compared to many conventional loans.

Understanding these benefits is crucial for navigating how to apply for an FHA mortgage successfully.

How to Apply for an FHA Mortgage

The process of applying for an FHA mortgage involves several steps and gathering specific documents. Start by assessing whether you meet the basic FHA loan requirements:

- Credit Score: Typically, a minimum score of 580 is needed for the low down payment option. Those with scores between 500 and 579 might still qualify, but with a larger down payment.

- Down Payment: As little as 3.5% for those meeting the credit score threshold.

- Debt-to-Income Ratio: Ideally, below 43%, though sometimes lenders accept higher.

- Employment History: Consistent income for at least two years.

- Property Standards: The home must meet FHA loan property requirements and undergo appraisals.

Step-by-Step Application Guide

1. Pre-approval: Start by getting pre-approved. This involves a credit check and offering preliminary financial information.

2. Assemble Financial Documents: Gather pay stubs, tax returns, and recent bank statements. Precision and accuracy are crucial.

3. Shop for Lenders: While FHA loans are governed by federal guidelines, different lenders offer varied terms. Compare and contrast interest rates, fees, and flexible terms.

4. Submit Your Application: Once you've chosen a lender, submit your formal application along with all required documents.

5. Appraisal and Inspection: The chosen property must undergo an FHA appraisal to ensure it meets requirements. If necessary, attend to any repairs to bring the property up to standard.

6. Final Loan Approval: After the appraisal and underwriting process is finished, await final approval.

7. Closing: If approved, proceed with the closing, completing paperwork, and paying any closing costs due.

Personal Insights on Applying for an FHA Mortgage

Having navigated the FHA mortgage process myself, I learned that patience and preparedness are key. One challenge was ensuring all documents were accurate and complete—a lesson in its own right. Additionally, I recommend working closely with your loan officer, who can provide invaluable advice and help streamline the application process.

Conclusion

Applying for an FHA mortgage is a feasible path for first-time homebuyers and those with limited funds for a down payment. By understanding the process and FHA loan requirements, you can better prepare to own a home.

Taking action and engaging with professionals can make this seemingly complex process more manageable. Stay informed, and happy home buying!