Buying your first home is a big step, and home insurance is a key part of the process. This guide, Understanding Home Insurance: A Guide for First-Time Buyers, explains what you need to know in simple terms. From coverage types to costs, we’ll help you protect your new home without the stress.

Why Home Insurance Matters for First-Time Buyers

Home insurance protects your house and belongings from unexpected problems like fires or theft. It also covers you if someone gets hurt on your property. Most mortgage lenders require it, but even if they didn’t, it’s a smart way to safeguard your investment. I learned this the hard way when a storm damaged my roof a year after buying my first home—insurance saved me thousands.

Types of Home Insurance Policies

Not all home insurance policies are the same. Here’s a quick breakdown:

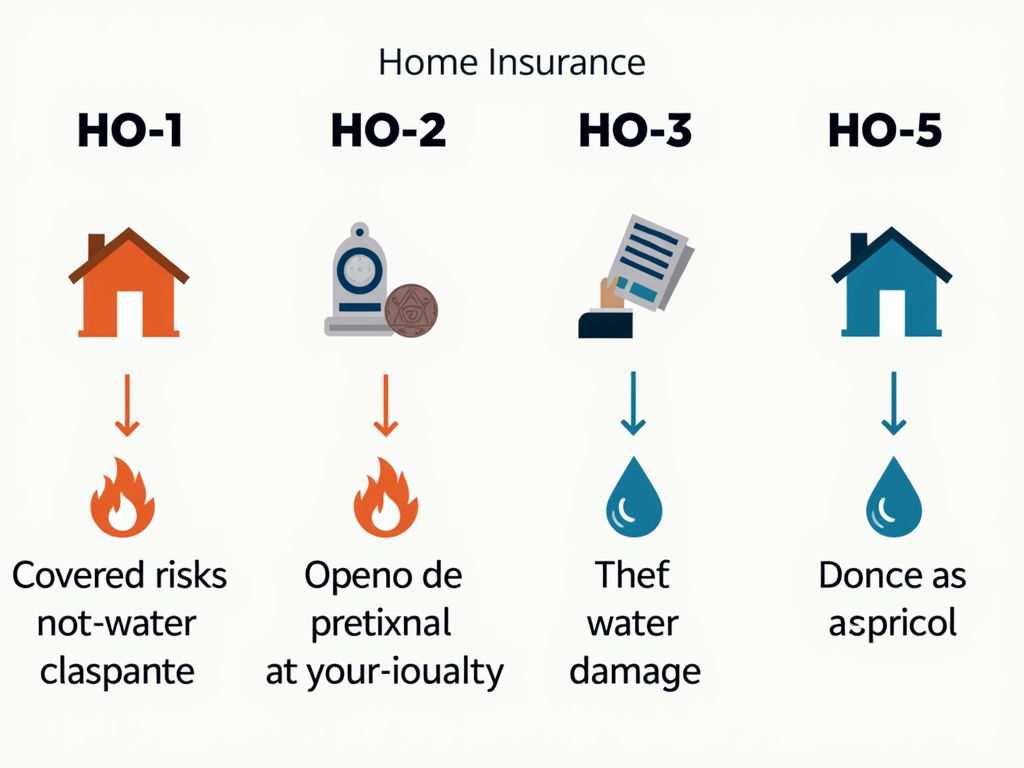

- HO-1 (Basic): Covers basic risks like fire, theft, and lightning. It’s cheap but limited.

- HO-2 (Broad): Adds coverage for things like water damage or falling objects.

- HO-3 (Special): The most common choice, covering most risks except specific exclusions like floods.

- HO-5 (Comprehensive): Protects your home and belongings with the widest coverage.

For most first-time buyers, an HO-3 policy works well. Check out this guide from the Insurance Information Institute for more details.

How to Pick the Right Policy

Choosing insurance can feel tricky, but it doesn’t have to be. Start by figuring out what you need—think about your home’s value and the risks in your area. Next, get quotes from at least three companies. Look for discounts, like ones for smoke alarms or bundling with car insurance. Finally, read the policy carefully. I once picked a cheap plan that didn’t cover water damage—big mistake when my basement flooded!

Credit Scores and Insurance Rates

Your credit score affects more than just loans—it can change your insurance costs too. Insurers use it to guess how likely you are to file a claim. A higher score often means lower rates. To boost your score, pay bills on time, cut down debt, and check your credit report for mistakes. The Federal Trade Commission explains credit scores and how they work—worth a read.

Steps to Improving Your Credit Score for Home Loans

Here’s a simple plan: 1. Pay on Time: Set reminders for bills. 2. Lower Debt: Pay off credit cards bit by bit. 3. Fix Errors: Dispute wrong info on your report. Improving my score took six months, but it cut my insurance rates by 15% when I bought my house.

FHA Loans: A First-Time Buyer’s Friend

If saving for a down payment feels impossible, look into FHA loan programs. These government-backed loans need as little as 3.5% down if your credit score is 580 or higher. For 2024, FHA loan requirements include a debt-to-income ratio under 43% and mortgage insurance payments. The catch? That insurance adds to your costs. Still, it helped me buy my first home when cash was tight.

FHA Loan Requirements for 2024

Here’s what you’ll need:

| Requirement | Details |

|---|---|

| Credit Score | 580+ for 3.5% down; 500-579 for 10% |

| Down Payment | 3.5% or 10% based on score |

| Debt-to-Income | 43% or less |

| Mortgage Insurance | Upfront and annual premiums |

Learn more at HUD’s official FHA page.

Essential Tips for First-Time Homebuyers

Navigating insurance doesn’t have to be hard. Here are some essential tips for first-time homebuyers: - Shop Early: Start looking before you close on the house. - Ask Questions: Don’t sign until you understand everything. - Bundle Policies: Save money by combining home and auto insurance. - Review Yearly: Update your coverage as your needs change.

When I bought my place, I waited too long and rushed into a policy. Take your time—it’s worth it.

Common Mistakes to Avoid

First-time buyers often trip up. Don’t underinsure—cheap policies might not cover enough. Avoid skipping flood insurance if you’re in a risky area; standard policies don’t include it. And don’t assume your belongings are fully protected—check limits on things like jewelry. A friend lost a pricey necklace in a theft and got almost nothing back because of this.

How Much Does Home Insurance Cost?

Costs vary by location, home size, and coverage. The average is about $1,200 a year, says the National Association of Insurance Commissioners. In my state, I pay $1,000 annually for an HO-3 policy, but my neighbor in a flood zone pays $1,500 with extra coverage. Shop around to find what fits your budget.

Summary

Home insurance is a must for first-time buyers—it protects your home, meets lender rules, and gives you peace of mind. Understand your options, like HO-3 policies or FHA loans, and take steps to get the best rates. With the right plan, you’ll settle into your new home worry-free. Check out the readings below for more help!