The Federal Housing Administration (FHA) mortgage program is a popular choice for first-time homebuyers and those with less-than-perfect credit. FHA loans are insured by the government, which allows lenders to offer more lenient requirements compared to conventional loans. This guide will help you understand the key requirements for obtaining an FHA mortgage, including credit score, down payment, debt-to-income ratio, and property eligibility.

What is an FHA Mortgage?

An FHA mortgage is a home loan insured by the Federal Housing Administration. This insurance protects lenders against losses if borrowers default on their loans, allowing lenders to offer more favorable terms. FHA loans are particularly attractive to first-time homebuyers because they require lower down payments and have more flexible credit requirements than conventional loans.

Key FHA Mortgage Requirements

To qualify for an FHA mortgage, borrowers must meet several requirements. These include:

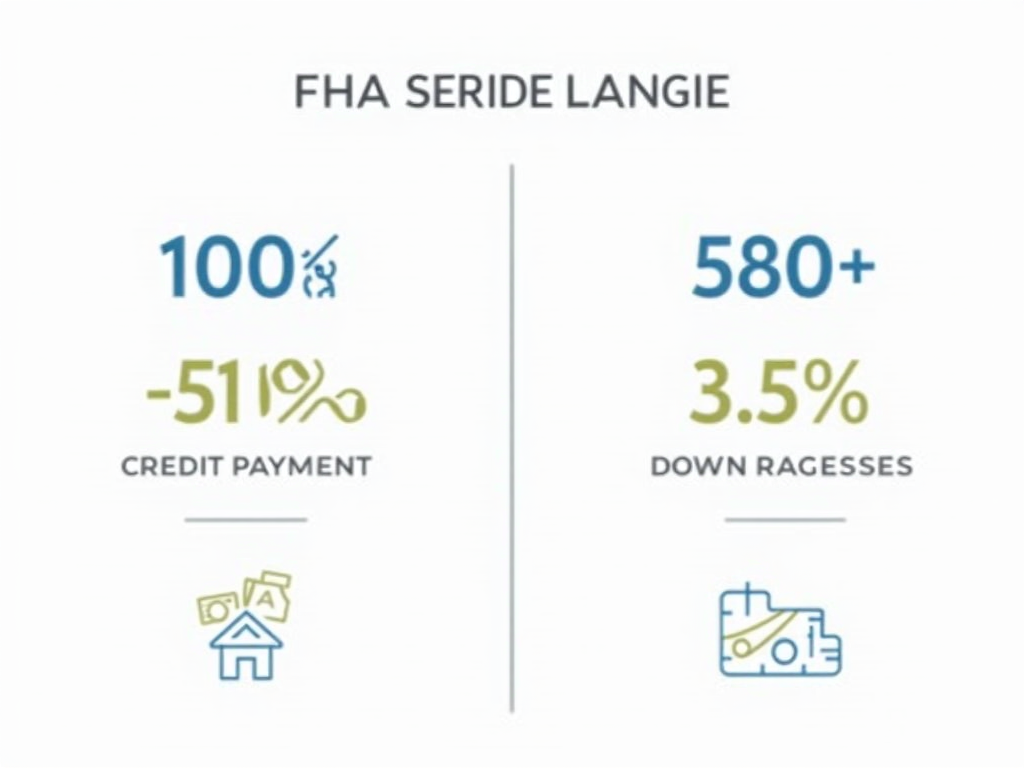

- Credit Score: A minimum credit score of 500 is required, but to qualify for the lowest down payment, a score of at least 580 is needed.

- Down Payment: Borrowers with a credit score of 580 or higher can make a down payment as low as 3.5%. Those with scores between 500 and 579 must put down at least 10%.

- Debt-to-Income Ratio (DTI): The maximum DTI is typically 43%, but this can be higher in certain cases.

- Property Eligibility: The property must be a primary residence and meet certain standards set by the FHA.

Credit Score Requirements

Your credit score plays a significant role in determining your eligibility for an FHA loan and the terms you'll receive. Here's how it works:

- 500-579: You can qualify for an FHA loan with a credit score as low as 500, but you'll need to make a down payment of at least 10%.

- 580 and above: With a credit score of 580 or higher, you can qualify for a down payment as low as 3.5%.

For example, if you're buying a $200,000 home: - With a credit score of 580, your down payment would be $7,000 (3.5%). - With a credit score of 550, your down payment would be $20,000 (10%).

Improving your credit score can save you thousands of dollars on your down payment, so it's worth taking steps to boost your score before applying for a mortgage.

Down Payment Requirements

One of the biggest advantages of FHA loans is the low down payment requirement. Here's what you need to know:

- 3.5% Down Payment: Available to borrowers with a credit score of 580 or higher.

- 10% Down Payment: Required for borrowers with a credit score between 500 and 579.

Additionally, the down payment can come from various sources, including savings, gifts from family members, or down payment assistance programs. This flexibility makes homeownership more accessible to those who may not have substantial savings.

Debt-to-Income Ratio (DTI)

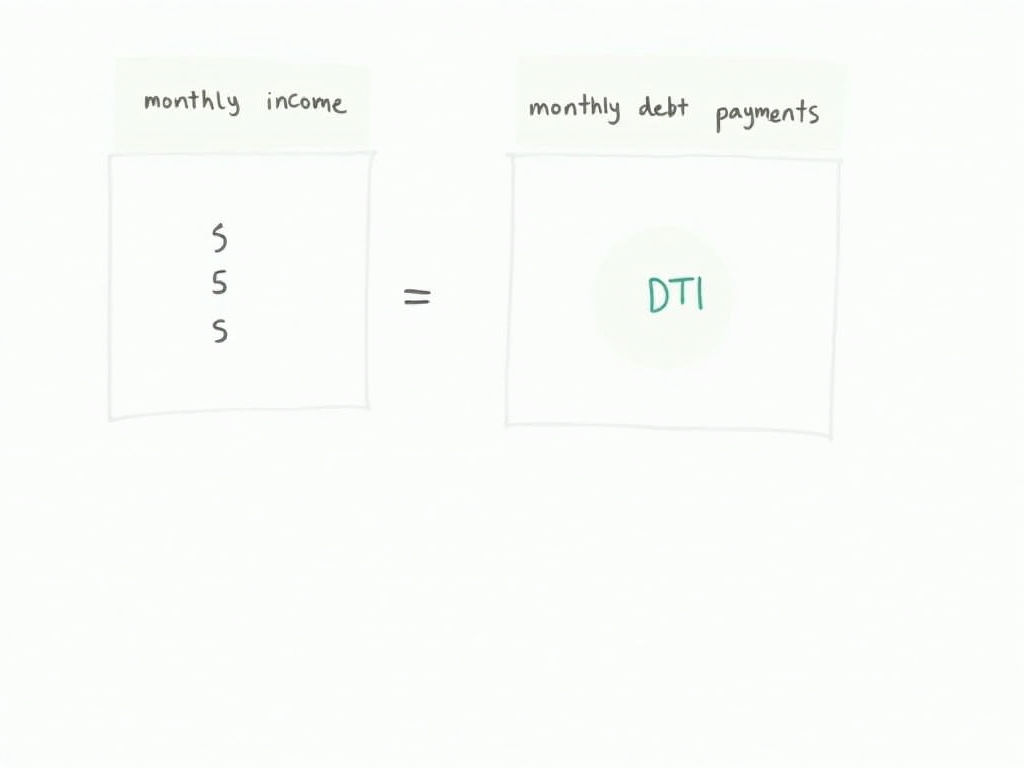

Your debt-to-income ratio is a measure of your ability to manage monthly payments. It's calculated by dividing your total monthly debt payments by your gross monthly income. For FHA loans:

- Maximum DTI: Typically 43%, but can be higher with compensating factors like a higher credit score or larger down payment.

For example, if your gross monthly income is $5,000 and your total monthly debt payments (including the proposed mortgage payment) are $2,000, your DTI would be 40% ($2,000 / $5,000 = 0.4 or 40%). This would be within the acceptable range for an FHA loan.

Property Eligibility

FHA loans can only be used to purchase certain types of properties, and the property must meet specific standards:

- Property Type: Must be a primary residence, such as a single-family home, a 2-4 unit property, or an FHA-approved condominium.

- Property Standards: The property must meet minimum safety, security, and soundness standards as determined by an FHA appraisal.

For instance, if you're buying a fixer-upper, it may not qualify for an FHA loan unless the necessary repairs are made before closing. However, the FHA does offer a special loan program called the 203(k) loan, which allows borrowers to finance both the purchase and renovation of a home.

Personal Insights: Why FHA Loans Matter

As someone who has worked with many first-time homebuyers, I've seen firsthand how FHA loans can make the dream of homeownership a reality. For example, I once helped a young couple with credit scores in the low 600s secure an FHA loan with a 3.5% down payment. They were able to buy a home that fit their budget and start building equity, something they thought was out of reach with a conventional loan.

FHA loans aren't just for those with low credit scores, though. They're also a great option for buyers who want to minimize their down payment or who are purchasing in areas where property values are rising quickly. The key is to understand the requirements and ensure that an FHA loan aligns with your financial goals.

Summary

Understanding FHA mortgage requirements is essential for anyone considering this type of loan. With lower credit score and down payment requirements, FHA loans offer a path to homeownership for many who might not qualify for conventional financing. However, it's important to weigh the benefits against the costs, such as mortgage insurance premiums, and to ensure that the property you want to buy meets FHA standards.

If you're ready to take the next step, consider speaking with a mortgage lender who specializes in FHA loans. They can help you determine if you meet the requirements and guide you through the application process.