Overview

Buying your first home marks a thrilling milestone. This guide walks you through every step, from budgeting to closing the deal. Whether you're dreaming of a family-friendly spot or navigating loans, you'll find clear advice to make smart choices. (38 words)

Imagine the day you turn the key to your own front door. That sense of stability and joy? It's within reach. As a first-time buyer, the process can feel overwhelming, but it doesn't have to. I've walked this path myself—nervous about finances one minute, elated the next. This guide shares what I learned, plus expert tips, to help you build a solid foundation.

We'll cover everything from setting a budget to picking the perfect spot. And yes, we'll dive into financing options that make homeownership accessible. Ready to start?

Assess Your Finances First

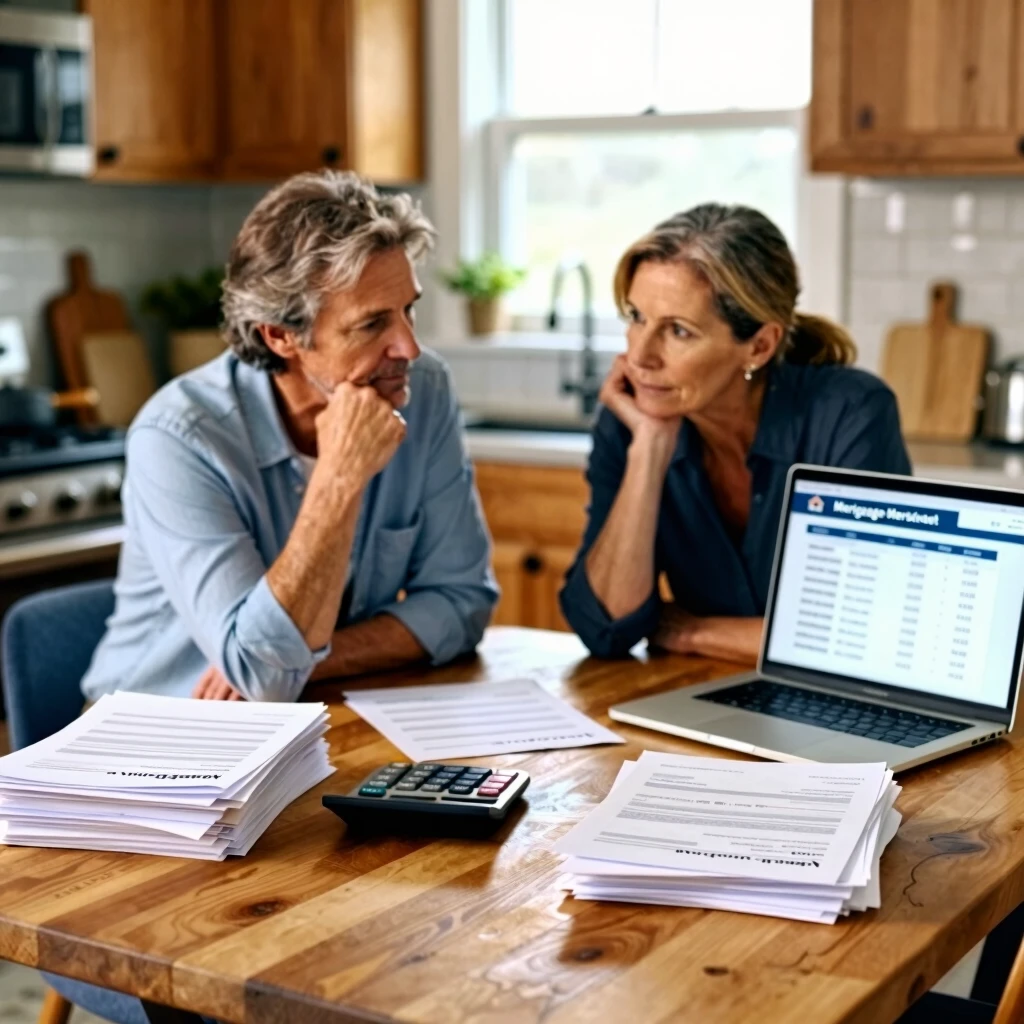

Before you fall in love with granite countertops, get real about your money. Start by calculating your income, debts, and savings. Aim to keep housing costs under 28% of your gross monthly income—this is the golden rule lenders follow.

When I bought my first place, I underestimated utility bills. Don't make that mistake. Track your expenses for a month using a simple app. Then, factor in a 20% down payment (or less with certain loans) and closing costs, which can hit 2-5% of the home price.

Here's a quick budget checklist:

- Monthly income: After taxes.

- Debts: Student loans, car payments.

- Emergency fund: At least three months' expenses.

- Down payment savings: Target 3-20%.

Pro tip: Use a free online affordability calculator. It paints a clear picture.

| Budget Item | Estimated Cost | Notes |

|---|---|---|

| Down Payment | 3-20% of home price | Lower with FHA loans |

| Closing Costs | 2-5% | Includes appraisal, title fees |

| Moving Expenses | $500-2,000 | DIY to save |

| Initial Repairs | 1% of price | Buffer for surprises |

This table helped me stay grounded. Adjust based on your situation.

Step-by-Step Guide to Home Buying

The home buying process boils down to clear stages. Follow this roadmap, and you'll move forward with confidence. I remember my first open house—heart racing, notebook in hand. It was chaotic but rewarding.

Step 1: Get Pre-Approved for a Mortgage

Shop lenders early. A pre-approval letter shows sellers you're serious and helps you know your price range. Compare rates from banks, credit unions, and online lenders. It took me two weeks to nail this down—worth every call.

Step 2: Hire a Real Estate Agent

Find an agent who knows your area like the back of their hand. They negotiate on your behalf and spot red flags. Interview a few; chemistry matters. Mine saved me thousands by catching a leaky roof issue.

Step 3: Start House Hunting

Make a must-have list: bedrooms, yard size, commute time. Attend open houses and drive by at different times to gauge traffic. I toured 15 homes before finding 'the one.' Patience pays off.

Step 4: Make an Offer

Your agent crunches comps—recent sales of similar homes. Bid slightly below if the market cools, or match asking in hot areas. Include contingencies for inspection and appraisal.

Step 5: Home Inspection and Appraisal

Never skip the inspection; it's your safety net. Expect to spend $300-500. The appraisal, ordered by your lender, ensures the home's worth the loan amount. Mine revealed wiring updates needed—glad I knew.

Step 6: Close the Deal

Review the closing disclosure 48 hours before signing. Bring ID, cashier's check, and excitement. Walk out with keys in hand.

For more on these phases, check the detailed steps from the U.S. Department of Housing and Urban Development.

How to Choose the Right Neighborhood for Your Family

Your home is more than walls—it's the community around it. Picking the right neighborhood sets the stage for family memories. Think schools, parks, and safety first. When my partner and I hunted for our spot, we prioritized walkable streets for our kids' bike rides.

Start with these factors:

- Schools and Education: Research ratings on GreatSchools.org. Visit during pickup to feel the vibe.

- Safety: Check crime maps from local police sites. Talk to residents for unfiltered views.

- Amenities: Proximity to grocery stores, playgrounds, and public transit. We loved our area's weekend farmers market.

- Future Growth: Look for planned developments that could boost or burden values.

- Community Feel: Attend a block party or chat with neighbors. It reveals the heart of the place.

Drive through at night and weekends to see the real rhythm. For deeper insights, explore tips for building strong neighborhood connections from Michigan State University Extension.

Remember, no perfect spot exists, but the right one feels like home.

Explore Financing: Focus on FHA Loan Programs

Financing is the engine of your purchase. If your savings are modest, government-backed loans open doors. FHA loans shine for first-timers—they require just 3.5% down and accept credit scores as low as 580.

FHA loan programs, insured by the Federal Housing Administration, protect lenders if you default, so they offer flexible terms. Ideal for fixer-uppers too, with options like 203(k) for rehab costs.

I used an FHA loan for my starter home. The lower down payment let me afford a better kitchen remodel right away.

How to Apply for an FHA Loan

Applying is straightforward but requires prep. Here's how:

- Check Eligibility: Steady income, debt-to-income ratio under 43%, and U.S. citizenship or residency.

- Gather Documents: Pay stubs, tax returns, bank statements—two years' worth.

- Shop Lenders: FHA-approved ones only. Compare interest rates and fees.

- Submit Application: Online or in-person. Expect questions on your finances.

- Underwriting Review: They verify everything; this takes 30-45 days.

- Appraisal and Closing: Home must meet FHA standards.

Boost your odds by paying down debt first. Learn more about FHA loan requirements explained by the Consumer Financial Protection Bureau.

Other paths? Conventional loans for strong credit, or VA/USDA for vets and rural buyers. Weigh pros like lower rates against cons like mortgage insurance.

Negotiate and Inspect Like a Pro

Once you find a gem, negotiate smartly. If the inspection flags issues, ask for repairs or credits. I pushed back on a faulty HVAC—seller covered half.

Also, budget for ongoing costs: HOA fees, property taxes, insurance. Use this list to stay ahead:

- Property taxes: 1-2% of value annually.

- Homeowners insurance: $1,000-2,000/year.

- Maintenance: Set aside 1% of home value yearly.

These keep surprises at bay.

Personal Insights: Lessons from My First Buy

Looking back, my biggest win was patience. We almost jumped on a flashy listing, but waiting uncovered a better fit. Trust your gut, but back it with facts.

Talk to mentors—friends who've bought recently shared negotiation hacks I missed. And celebrate small victories, like that pre-approval. It builds momentum.

One pitfall? Overlooking resale value. Choose timeless features over trends. Your home should grow with you.

Wrapping Up: Your Path to Homeownership

You've got the tools now—from budgets to bids, neighborhoods to loans. Buying your first home transforms lives, creating roots for tomorrow. Take it one step at a time, lean on pros, and soon you'll toast in your new space. The reward? Priceless security and stories for years. Start today—what's your first move?