If you're a first-time homebuyer or someone with a less-than-perfect credit score, an FHA loan might be the perfect solution for you. FHA loans, backed by the Federal Housing Administration, offer more flexible requirements than conventional loans, making homeownership accessible to more people. In this guide, we'll walk you through the entire FHA loan process, step by step, so you can feel confident and prepared. From understanding what an FHA loan is to closing on your dream home, we've got you covered.

What is an FHA Loan?

An FHA loan is a mortgage insured by the Federal Housing Administration. This means that if you default on your loan, the FHA will cover the lender's losses. Because of this insurance, lenders are more willing to offer loans to borrowers who might not qualify for conventional mortgages. FHA loans are especially popular among first-time homebuyers because they require lower down payments and have more lenient credit score requirements.

Why Choose an FHA Loan?

There are several reasons why an FHA loan might be the right choice for you:

- Lower Down Payment: You can put down as little as 3.5% of the home's purchase price.

- Flexible Credit Requirements: FHA loans are available to borrowers with credit scores as low as 580.

- Competitive Interest Rates: Because the loan is insured, lenders can offer lower interest rates.

- Assistance for Low-to-Moderate Income Buyers: FHA loans are designed to help those who might not otherwise qualify for a mortgage.

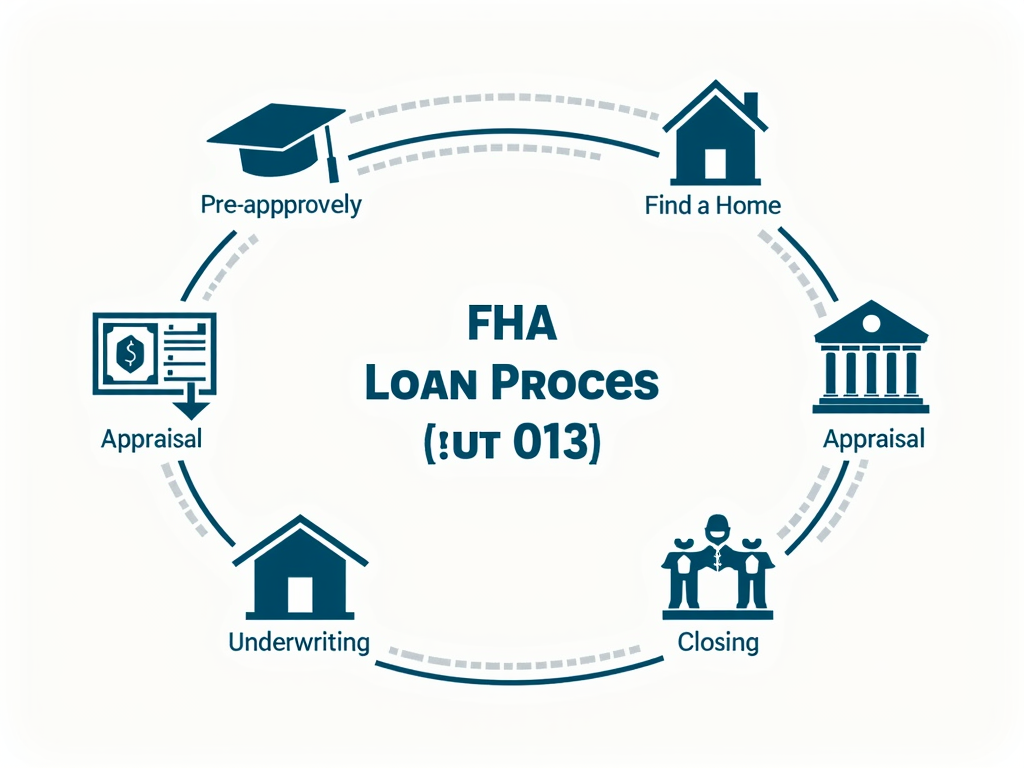

Step 1: Get Pre-Approved for an FHA Loan

Before you start house hunting, it's crucial to get pre-approved for an FHA loan. Pre-approval shows sellers that you're a serious buyer and gives you a clear idea of how much you can afford. Here's how to get pre-approved:

- Find an FHA-Approved Lender: Not all lenders offer FHA loans, so make sure to choose one that is approved by the FHA.

- Submit Your Application: You'll need to provide financial documents, such as pay stubs, tax returns, and bank statements.

- Credit Check: The lender will check your credit score and history.

- Receive Pre-Approval Letter: If you qualify, the lender will give you a pre-approval letter stating the loan amount you're eligible for.

Step 2: Find Your Dream Home

With your pre-approval in hand, it's time to start looking for a home. Keep in mind that the property must meet certain standards set by the FHA. This is where the FHA appraisal comes into play, but we'll cover that in more detail later. For now, focus on finding a home that fits your budget and needs.

Step 3: Make an Offer and Sign a Contract

Once you've found the perfect home, you'll need to make an offer. If the seller accepts, you'll sign a purchase agreement. This contract will include details like the sale price, closing date, and any contingencies, such as the home passing the FHA appraisal.

Step 4: Apply for Your FHA Loan

Now that you have a signed contract, it's time to formally apply for your FHA loan. You'll work with your lender to complete the application, which will require more detailed financial information. Be prepared to provide:

- Proof of income (pay stubs, W-2s)

- Tax returns

- Bank statements

- Employment verification

- Identification documents

Step 5: The FHA Appraisal Process

One of the unique aspects of an FHA loan is the appraisal process. The FHA requires an appraisal to ensure the property meets certain safety, security, and structural standards. Here's what you need to know:

- Hiring an Appraiser: Your lender will arrange for an FHA-approved appraiser to evaluate the property.

- Appraisal Checklist: The appraiser will check for things like the condition of the roof, plumbing, electrical systems, and overall safety.

- Valuation: The appraiser will also determine the home's market value to ensure it aligns with the loan amount.

FHA Appraisal Checklist for Homebuyers

To give you a better idea, here's a simplified version of what the appraiser looks for:

| Area | What the Appraiser Checks |

|---|---|

| Roof | No leaks, adequate remaining life |

| Foundation | No major cracks or structural issues |

| Plumbing | Functional, no leaks |

| Electrical | Safe and up to code |

| Heating/Cooling | Functional systems |

| Safety | Handrails on stairs, no peeling paint (for homes built before 1978), etc. |

Step 6: Underwriting and Loan Approval

After the appraisal, your loan application goes to underwriting. The underwriter reviews all your financial information and the appraisal report to decide whether to approve the loan. This step can take a few days to a few weeks, depending on the complexity of your application.

Step 7: Closing on Your Home

Once your loan is approved, you're ready to close. At closing, you'll sign the final paperwork, pay any closing costs, and receive the keys to your new home. Be sure to review all documents carefully and ask questions if anything is unclear.

Tips for a Smooth FHA Loan Process

- Stay Organized: Keep all your financial documents in one place for easy access.

- Communicate with Your Lender: Respond promptly to any requests for additional information.

- Be Patient: The process can take time, especially during the appraisal and underwriting stages.

- Understand the Costs: FHA loans require mortgage insurance premiums (MIP), so factor that into your budget.

Conclusion

Navigating the FHA loan process might seem daunting at first, but by breaking it down into manageable steps, you can approach it with confidence. From getting pre-approved to closing on your home, each stage is designed to help you achieve your dream of homeownership. Remember, the key is to stay informed, organized, and proactive throughout the process. With this guide, you're well on your way to securing an FHA mortgage and moving into your new home.