Buying a home is a big deal—it’s exciting, a little scary, and one of the biggest financial steps you’ll take. This guide breaks down The Homebuying Process: A Step-by-Step Guide to make it simple and clear. We’ll cover everything from setting your budget to getting the keys, plus tips on mortgages like FHA loans. Ready? Let’s dive in!

Step 1: Determine Your Budget

First things first: figure out what you can afford. Look at your income, savings, and credit score. A handy tip? Aim for a home that costs 2.5 to 3 times your yearly income. So, if you make $60,000 a year, think $150,000 to $180,000.

You’ll need cash for a down payment—usually 3-5% of the home price—and closing costs, another 2-5%. Your credit score matters too. A score above 620 gets you better mortgage rates. If it’s lower, work on paying off debt or fixing errors on your report.

Here’s a quick look:

| Annual Income | Home Price (2.5x) | Home Price (3x) |

|---|---|---|

| $40,000 | $100,000 | $120,000 |

| $60,000 | $150,000 | $180,000 |

| $80,000 | $200,000 | $240,000 |

Step 2: Get Pre-Approved for a Mortgage

Next, get pre-approved by a lender. This shows how much you can borrow and proves to sellers you’re serious. You’ll need pay stubs, tax returns, bank statements, and ID. The lender checks your credit too.

Pre-approval isn’t the same as pre-qualification. Pre-qualification is a quick estimate; pre-approval is the real deal after a full financial review. It’s a game-changer when you’re ready to shop.

Step 3: Find a Real Estate Agent

A good real estate agent makes the process smoother. They know the market, find homes that fit your needs, and handle negotiations. Pick someone local with a solid reputation.

How? Ask friends for recommendations, read reviews, and interview a few agents. I once found a great agent through a neighbor’s tip—she knew every street in town and saved me weeks of searching!

Step 4: Start House Hunting

Time to hunt for your dream home! List what you need—like bedrooms or a garage—and what you’d love, like a big backyard. Check out open houses and book private tours.

Think about location too: schools, work, and safety. Take notes and photos. One time, I fell for a house but realized the commute was brutal—location matters as much as the house itself.

Step 5: Make an Offer

Found the one? Make an offer! Your agent will suggest a price based on similar homes sold nearby. Include details like:

- Contingencies (inspection, financing)

- Closing date

- Earnest money (1-3% of the price)

Sellers might counter, so be ready to negotiate. My first offer got rejected, but we tweaked it and won the second time—patience pays off.

Step 6: Get a Home Inspection

Once your offer’s accepted, hire an inspector. They’ll check the roof, plumbing, electrical systems—everything. You’ll get a report on what’s good or needs fixing.

If there’s a big issue, ask the seller to repair it or lower the price. I skipped this once and regretted it when the AC broke a month later. Don’t skip the inspection!

Step 7: Secure Financing

Now, lock in your mortgage. Pick your interest rate, finish the loan application, and send any extra papers the lender needs. Review the loan estimate—it shows your costs—and the closing disclosure later.

Ask questions if something’s unclear. I caught a fee error once by double-checking, saving me a few hundred bucks.

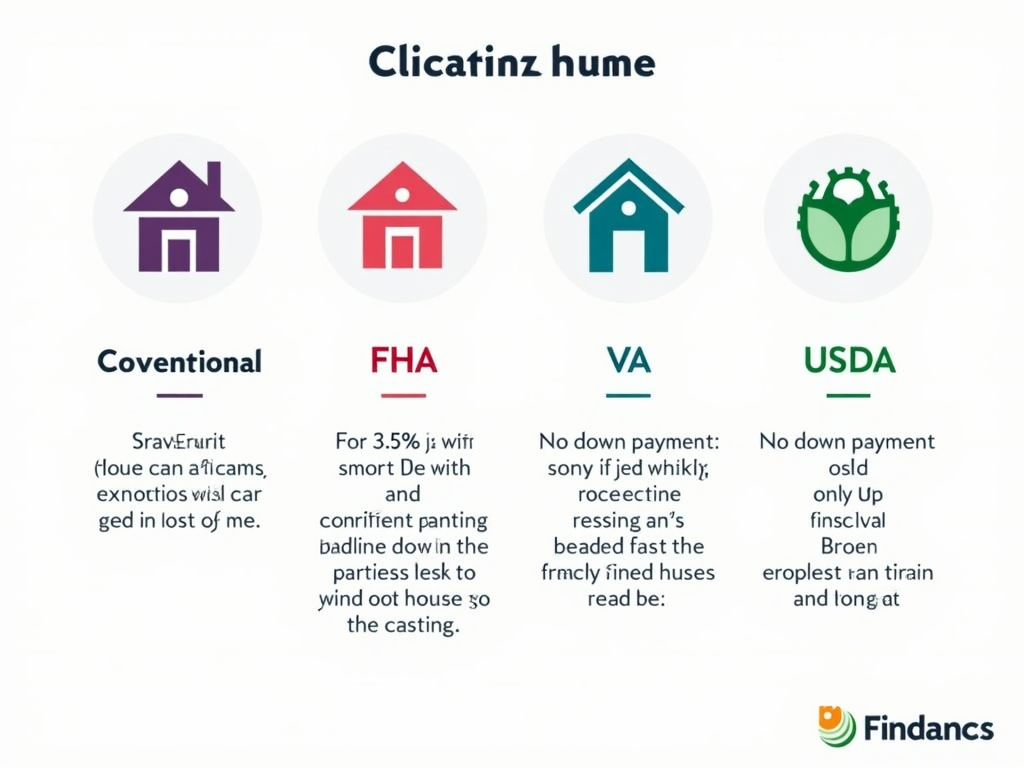

Understanding Mortgage Types and Options

Mortgages come in different flavors. Here’s the rundown:

- Conventional Loans: No government backing, need a 620+ credit score, 5-20% down.

- FHA Loans: Great for first-timers, backed by the FHA, need 500-580 credit and 3.5-10% down.

- VA Loans: For veterans, no down payment, super rates.

- USDA Loans: For rural areas, no down payment.

FHA loans are forgiving on credit and down payments—perfect if you’re starting out. Compare lenders for the best deal. Check out the Consumer Financial Protection Bureau for more.

| Type | Credit Score | Down Payment | Backed? |

|---|---|---|---|

| Conventional | 620+ | 5-20% | No |

| FHA | 500-580 | 3.5-10% | Yes |

| VA | Varies | 0% | Yes |

| USDA | 640+ | 0% | Yes |

How to Apply for an FHA Mortgage

Interested in an FHA mortgage? Here’s the scoop:

- Check FHA Loan Requirements: You need a 500 credit score (10% down) or 580 (3.5% down), a debt-to-income ratio under 43%, steady work, and the home must be your main residence.

- Find a Lender: Use an FHA-approved one—check online.

- Gather Papers: Pay stubs, tax returns, bank statements, ID.

- Apply: Your lender helps you submit.

- Wait: Approval takes a few weeks.

It’s straightforward if you’re prepared. Visit FHA.com for details.

Step 8: Close the Deal

Finally, closing day! Sign the mortgage papers, pay closing costs (fees, insurance, taxes), and do a last walkthrough. Then, grab your keys!

Read everything—my friend found a typo that almost cost her extra. It’s a big moment, so enjoy it. You’re a homeowner now!

Summary

The homebuying process takes effort, but it’s worth it. Set your budget, get pre-approved, team up with an agent, hunt for a home, make an offer, inspect it, secure your loan, and close the deal. Explore mortgage options like FHA loans to fit your needs. Stay curious and lean on pros—you’ve got this!