Buying a home is exciting, but figuring out home loan interest rates can feel overwhelming. This Guide to Home Loan Interest Rates Explained simplifies it all. We’ll cover what interest rates are, what affects them, and how FHA loans fit in. By the end, you’ll know how to save money and choose the right loan.

What Are Home Loan Interest Rates?

Interest rates are what you pay to borrow money for your home, shown as a percentage of the loan. Think of it as the lender’s fee for giving you the cash. For example, on a $200,000 loan with a 4% rate, you’d pay $8,000 in interest yearly—at first.

These rates shape your monthly payments and the total cost over time. A lower rate means smaller payments and less spent overall. A higher rate bumps up both. It’s a big deal when you’re committing to years of payments.

Factors That Affect Your Interest Rate

Your interest rate isn’t random—several things decide it. Here’s what matters most:

- Credit Score: This shows lenders how reliable you are with money. Scores above 700 often get the best rates. Below 620? Rates might climb.

- Down Payment: Putting more money upfront lowers the lender’s risk. A 20% down payment can snag you a better deal.

- Loan Term: Shorter loans (like 15 years) usually have lower rates but bigger monthly payments. Longer ones (like 30 years) cost more in interest.

- Fixed or Variable: Fixed rates stay steady—great for planning. Variable rates might start low but can rise later.

- Economy: Things like inflation or federal rates shift the market. When the economy heats up, rates often follow.

Want to dig deeper into credit scores? Check out this guide from myFICO.

What’s an FHA Loan?

An FHA loan is a mortgage backed by the government through the Federal Housing Administration. It’s built for people who might struggle with regular loans—like first-timers or those with lower credit. I’ve seen friends use FHA loans to buy their first homes when banks turned them down.

Why Choose an FHA Mortgage?

- Low Down Payment: You can start with just 3.5% down.

- Easier Credit Rules: Qualifying is possible even with a credit score as low as 500.

- Good Rates: Lenders offer competitive rates because the FHA covers their risk.

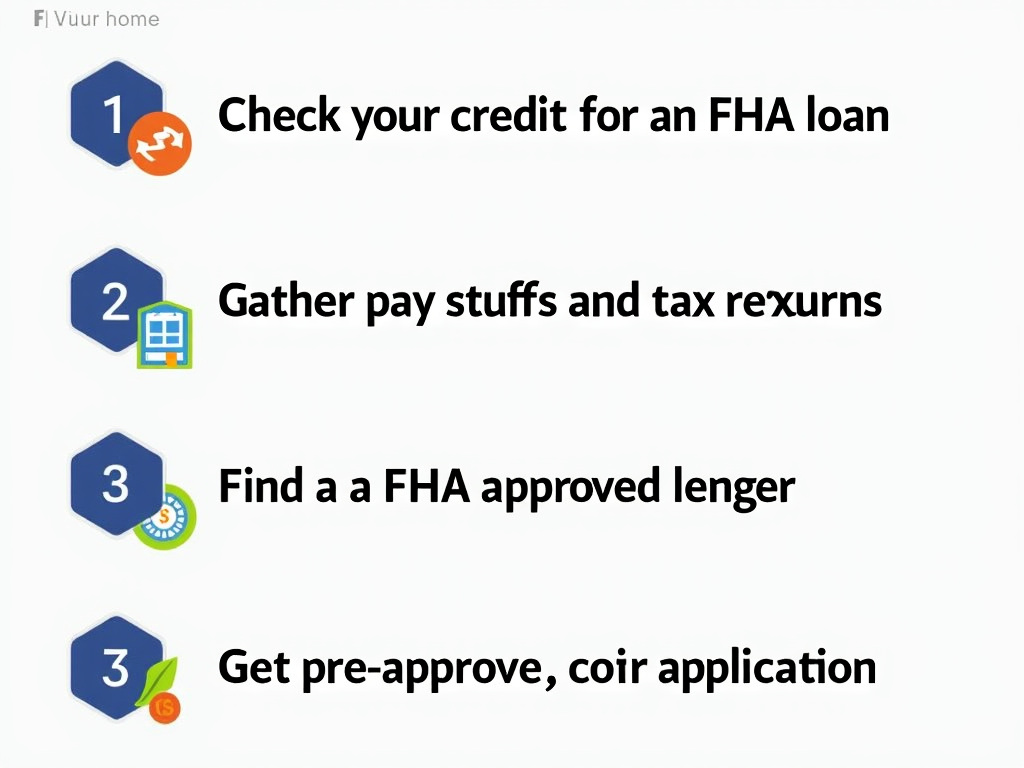

FHA Loan Requirements

To get an FHA loan, you need to meet some basics:

- Credit Score: At least 500 with 10% down, or 580 with 3.5% down.

- Debt-to-Income: Your debts shouldn’t eat up more than 43% of your income.

- Income Proof: Show steady work and pay for two years.

- Primary Home: You have to live in the house—no rentals allowed.

These FHA loan requirements make it doable for lots of people. My cousin got one with a 590 score and couldn’t believe how straightforward it was.

FHA Mortgage Eligibility Criteria

Beyond the requirements, there’s eligibility to nail down:

- Social Security Number: You need a valid one.

- U.S. Residency: Legal residents only—no exceptions.

- No Recent Big Setbacks: Wait two years after bankruptcy, three after foreclosure.

These FHA mortgage eligibility criteria keep things fair. For the full scoop, visit the FHA’s official site. It’s a goldmine of info.

How FHA Loan Rates Work

FHA loan rates often beat conventional ones, especially if your credit’s shaky. The government backing means lenders take less risk, so they cut you a break. Still, your rate depends on your credit, down payment, and the market.

Compared to regular loans, FHA rates can save you money upfront. But there’s a catch: you’ll pay mortgage insurance premiums (MIP) every month. For a $200,000 loan, that might add $100 or more to your payment. Weigh the rate against the total cost—sometimes conventional wins out.

Curious about MIP? The Consumer Financial Protection Bureau explains it clearly.

Tips to Score the Best Interest Rate

Getting a great rate takes some work, but it’s worth it. Here’s how:

- Boost Your Credit: Pay bills on time and cut debt. Even a 50-point jump can help.

- Save More Upfront: Aim for 20% down if you can—it’s a game-changer.

- Pick the Right Term: A 15-year loan might stretch you but saves big on interest.

- Shop Around: Check at least three lenders. I once saved 0.5% just by comparing.

- Explore FHA: If your credit’s low, an FHA mortgage might be your best shot.

A tiny rate drop—like 4.5% to 4% on a $250,000 loan—can save you $30,000 over 30 years. Small moves, big wins.

Wrapping It Up

Home loan interest rates don’t have to be a mystery. This Guide to Home Loan Interest Rates Explained showed you how they work, what moves them, and why FHA loans are a solid option. With lower down payments and flexible FHA mortgage eligibility criteria, they’ve opened doors for tons of buyers.

Take charge: improve your credit, save up, and compare lenders. A little effort now can mean a cheaper, stress-free mortgage later. Your dream home is closer than you think—start exploring your options today.